- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 31-08-2011

The Nasdaq recently slipped into negative territory. Although AOL (AOL 15.70, +0.39) has been a source of support, Yahoo! (YHOO 13.65, -0.19) has been a source of weakness.

EUR/JPY follows the euro decline and currently trades below Y110.00 for lows around Y109.90. Bids at Y110.00 filled on the slide lower with

further demand interest nearby at Y109.80/70.

GBP/USD continues to recover from session lows at $1.6250 and currently holds at $1.6271. Stops below $1.6250. Offers at $1.6300.

Positive sentiment among participants continues to prop up stocks.

Broad-based strength took all three of the major equity averages up more than 1% before the move was challenged.

Financials have been a source of support after lagging in the prior session. Yesterday financials fell 0.7%, but today they have swung to a gain of almost 2%.

The franc rose as the Swiss National Bank refrained from announcing new steps to curb its gains, after intervening or referring to the currency’s strength on the first three Wednesdays of August.

The dollar erased earlier losses against the euro as better-than-forecast economic data damped bets the Federal Reserve may take further steps to stimulate growth.

The euro fell as US Commerce Department data showed orders placed with U.S. factories rose in July by the most in four months, increasing 2.4%.

The Institute for Supply Management-Chicago Inc.’s business barometer fell less than projected this month, declining to 56.5.

Data from ADP Employer Services earlier showed companies in the U.S. added 91,000 workers to payrolls in August, less than the 100,000 forecast. A government report on Sept. 2 is projected to show U.S. nonfarm payroll growth slowed to 70,000 this month from 117,000 in July.

The euro weakened today as data showed unemployment in the region held at 10% in July from the previous month.

AUD/USD rose to session highs on $1.0716, a bit lower offers on $1.0720 and retreated to the figure. Stops above $1.0720 which if triggered open the way to $1.0785/90.

USD/CAD recovered from lows after the pair skidded to lows near C$0.9720 as stops were flushed sub C$0.9740. Pair trades at C$0.9771 with offers likely C$0.9780/90.

EUR/JPY recovers after it earlier fell to Y110.01. Cross currently holds at Y110.20. Offers remain at Y110.90/00 (Y110.99 o/n Asian high), a break here opens a move towards Y111.40/50. Bids now mention at Y109.80/70 ahead of Y109.10/00 (Y109.02 - 19 Aug low).

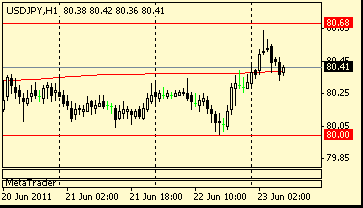

USD/JPY continues to trade higher at Y76.78 currently, just off the session high Y76.83. Small bids at Y76.65/60, behind here very large bids at Y76.50, further bids at Y76.45/40 with stops set below. Further demand is meantioned at Y76.35 ahead of Y76.20/10. Offers noted at Y76.95/00 and Y77.35/40 ahead of large offers at Y77.70.

EUR/USD .$1.4475, $1.4500

USD/JPY Y76.80

GBP/USD $1.6315

AUD/USD $1.0700, $1.0600

AUD/JPY Y81.35

06:00 Germany Retail sales (July) real adjusted 0.0%

06:00 Germany Retail sales (July) real unadjusted Y/Y -1.6%

07:55 Germany Unemployment (August) seasonally adjusted -8.0K

07:55 Germany Unemployment (August) seasonally adjusted, mln 2.951

07:55 Germany Unemployment rate (August) seasonally adjusted 7.0%

07:55 Germany Unemployment (August) seasonally unadjusted, mln 2.945

07:55 Germany Unemployment rate (August) seasonally unadjusted 7.0%

09:00 EU(17) Harmonized CPI (August) Y/Y preliminary 2.5%

09:00 EU(17) Unemployment (July) 10.0%

1230GMT release of the latest ISM-NY Business Index. At 1345GMT, the Chicago PMI

is expected to fall to a reading of 53.0 in August after falling in July. Other regional data already released have suggested significant contraction. This is followed at 1400GMT by Factory Orders and also the latest Help-wanted Online index. Factory new orders are forecast to rise 2.0% in July. Durables orders were already reported up 4.0% in the month on a spike in aircraft orders.

Weekly EIA Crude Oil Stocks data is due at 1430GMT. Then, at 1530GMT, Atlanta Fed President Dennis Lockhart is due to deliver a speech on the economy to the Greater Lafayette Chamber of Commerce. Late US data includes the 1900GMT release of Agriculture Prices for August.

EUR/USD:

Dip buying seen this morning as traders note the next target of $1.0780 for Aussie to gain momentum and push through $1.0900. Initial resistance reported at $1.0700/10 ahead of stops set through $1.0720. Downside bids noted at $1.0650/40 (100DMA $1.0646) ahead of $1.0625/20 (55DMA).

Data released:

05:00 Japan Housing starts (July) Y/Y 21.2% 4.9% 5.8%

05:00 Japan Construction orders (July) Y/Y 5.7% - 6.0%

06:00 Germany Retail sales (July) real adjusted 0.0% -1.5% 4.5 (6.3)%

06:00 Germany Retail sales (July) real unadjusted Y/Y -1.6% - -2.1 (-1.0)%

07:55 Germany Unemployment (August) seasonally adjusted -8.0K -9.7K -11K

07:55 Germany Unemployment (August) seasonally adjusted, mln 2.951 - 2.957

07:55 Germany Unemployment rate (August) seasonally adjusted 7.0% 7.0% 7.0%

07:55 Germany Unemployment (August) seasonally unadjusted, mln 2.945 - 2.939

07:55 Germany Unemployment rate (August) seasonally unadjusted 7.0% - 7.0%

Сoncern the global economic recovery is faltering maintained demand for assets perceived as the safest.

The euro weakened versus most of its 16 major peers as economists forecast unemployment in the 17-nation euro-region remained unchanged at 9.9 percent last month, a level it hasn’t fallen below since 2009. The yen headed for a third monthly gain versus the dollar before a report forecast to show the U.S. employers added fewer jobs this month. New Zealand’s dollar headed for its biggest monthly decline in a year versus the yen as the country’s business confidence worsened.

“Investors that think the world is falling apart and are worried about capital preservation still view the yen and the franc as safe havens,” said Elsa Lignos, a currency strategist in London at RBC Capital Markets in London. “We like the yen -- it just seems a little less overstretched than the Swissie.”

EUR/USD printed session highs on $1.4470, but failed to set above the figure and retreated to current $1.4430.

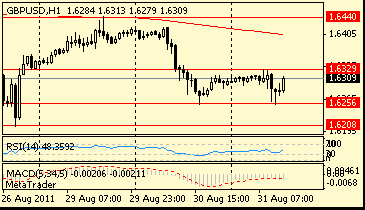

GBP/USD also retreats after it earlier tested $1.6330 and currently holds at $1.6270.

USD/JPY traded within Y76.52/75 range.

European data continues at 0900GMT with the EMU unemployment rate, which is expected to remain at 9.9% and also flash HICP data for August, which is expected to come in at 2.5% y/y. Also in Europe today, from 0730GMT, the German government meets to approve measures decided at a eurozone summit in July with the following press conference due to take place in Berlin at 1130GMT US data starts at 1100GMT with the weekly MBA Mortgage Application Index, which is followed at 1130GMT by Challenger Layoffs and at 1215GMT by the ADP National Employment Report before the 1230GMT release of the latest ISM-NY Business Index. At 1345GMT, the Chicago PMI

is expected to fall to a reading of 53.0 in August after falling in July. Other regional data already released have suggested significant contraction. This is followed at 1400GMT by Factory Orders and also the latest Help-wanted Online index. Factory new orders are forecast to rise 2.0% in July. Durables orders were already reported up 4.0% in the month on a spike in aircraft orders.

Weekly EIA Crude Oil Stocks data is due at 1430GMT. Then, at 1530GMT, Atlanta Fed President Dennis Lockhart is due to deliver a speech on the economy to the Greater Lafayette Chamber of Commerce. Late US data includes the 1900GMT release of Agriculture Prices for August.

EUR/USD

Offers: $1.4455, $1.4470

Bids: $1.4380

GBP/USD

Offers: $1.6330, $1.6350, $1.6380/85

Bids: $1.6290, $1.6250

USD/JPY

Offers: Y77.00/10, Y77.30

Bids: Y76.50, Y76.00

Majors close:

Nikkei 225 +102.55 +1.16% 8,953.90

FTSE 100 +138.74 +2.70% 5,268.66

CAC 40 +5.54 +0.18% 3,159.74

DAX -26.15 -0.46% 5,643.92

Dow +67.17 +0.58% 11,606.42

Nasdaq +23.16 +0.90% 2,585.27

S&P 500 +6.86 +0.57% 1,216.94

10 Year Yield 2.18% -0.09 --

Oil $88.76 +1.49 +1.71%

Gold $1,835.40 +5.60 +0.31%

Japanese stocks rose for a fourth day, the longest winning streak since July, with carmakers advancing as U.S. consumer spending rose more than forecast. Japan’s parliament today confirmed Finance Minister Yoshihiko Noda as the next prime minister.

Honda Motor Co., which gets 40 percent of its revenue from North America, climbed 1 percent after U.S. auto sales increased and Federal Reserve Chairman Ben S. Bernanke last week indicated the U.S. economy may not need more stimulus. Sony Corp. (6758) gained 3.5 percent after the Yomiuri newspaper reported it will form a venture to produce liquid-crystal displays with Toshiba Corp. (6502) and Hitachi Ltd. (6501)

For the month through yesterday, the Nikkei fell 8.9 percent, set for the biggest monthly loss since May 2010, while the Topix was down 8.8 percent.

European stocks rose for a second day as a rally in mining companies and U.K. banks outweighed a bigger-than-forecast decline in U.S. consumer confidence.

Rio Tinto Group pushed a gauge of basic-resources producers to the biggest increase in almost three weeks.

Rio Tinto, the world’s second-largest mining company, rallied 4.3 percent to 3,673.5 pence. BHP Billiton Ltd. (BHP), the biggest mining company, increased 4.3 percent to 2,042.5 pence while Xstrata Plc (XTA) added 4.7 percent to 1,025.5 pence.

Royal Bank of Scotland Group Plc (RBS) and Barclays Plc (BARC) climbed more than 6 percent. Ipsen SA (IPN), the French maker of a Botox rival, and Bunzl Plc (BNZL), the world’s biggest distributor of disposable tableware and food packaging, each surged 7.9 percent as earnings gained.

The Stoxx Europe 600 Index rose 1 percent to 230.64 at the 4:30 p.m. close in London, the highest in almost two weeks. The gauge has still tumbled 13 percent this month, the biggest drop since October 2008, as European and U.S. economic reports trailed forecasts, adding to concern that the economic recovery is at risk. The decline has left the measure trading at about 9.6 times estimated earnings, near the cheapest since March 2009

Gains in the Stoxx 600 were led by U.K. equities that missed out on yesterday’s rally because of a holiday. The Euro Stoxx 50 Index of the biggest companies in the euro area, which excludes British shares, slipped less than 0.1 percent, while the U.K.’s FTSE 100 Index (UKX) rallied 2.7 percent.

Equities in Europe pared their gains as a report showed confidence among U.S. consumers plunged in August to the lowest in more than two years.

U.S. stocks rose, amid a 152-point swing in the Dow Jones Industrial Average, after the Federal Reserve said some policy makers wanted to take more action to stimulate the economy during their meeting this month.

Caterpillar Inc. (CAT) and Boeing Co. (BA) rose more than 2.1 percent, pacing gains among companies most-tied to the economy. Monster Worldwide Inc. (MWW), the provider of help-wanted ads, advanced 18 percent, building on its 13 percent rally during the past two days. Bank of America Corp. (BAC) fell 2.4 percent as the Federal Deposit Insurance Corp. objected to the lender’s proposed $8.5 billion mortgage-bond settlement with investors.

The S&P 500 added 0.3 percent to 1,213.72 at 2:58 p.m. in New York, recovering from a 1.2 percent drop driven by consumer confidence sinking to a 28-month low. The Dow rose 37.35 points, or 0.3 percent, to 11,576.60.

“You still have the Fed in your corner,” Mark Foster, who helps manage $500 million at Kirr Marbach & Co. in Columbus, Indiana, said in a telephone interview. “That gives you confidence in a market like this especially after the volatility we’ve seen in the last few weeks, which was so unsettling.”

The S&P 500 rose to the highest level since Aug. 3 yesterday after surging 7.7 percent in six days. Equities gained 8.1 percent between Aug. 8 and yesterday after the loss of the U.S. government’s AAA credit rating left the S&P 500 trading for 12.2 times earnings, the lowest level since 2009.

The euro weakened against most major counterparts on speculation the European Central Bank has finished raising interest rates as the region’s sovereign-debt crisis curbs economic growth.

The yen rose versus 12 of its 16 major peers as U.S. consumer confidence dropped to the lowest since April 2009 and home prices fell, adding to demand for safer assets. The euro snapped a two-day gain versus the dollar after ECB President Jean-Claude Trichet said yesterday the bank is reviewing its assessment of inflation risks, and data today showed confidence in the region’s economy plunged. The ECB meets next week.

“There’s signs that the ongoing financial-market troubles are starting to have a more noticeable impact not only on confidence but on actual economic activity,” said Nick Bennenbroek, head of currency strategy at Wells Fargo & Co. in New York. “The challenges for the euro are accumulating, and this is a reason the euro is down today.”

U.S. stocks fell as the Conference Board’s index slumped to 44.5 this month, from a revised 59.2 reading in July, figures from the New York-based private research group showed. It was the biggest point drop since October 2008. Economists predicted the August gauge would fall to 52. The Standard & Poor’s 500 Index dropped 0.6 percent.

The S&P/Case-Shiller index of property values in 20 cities fell 4.5 percent in June from a year earlier, after dropping 4.6 percent in the 12 months ended in May, the group said today in New York. The median forecast was for a 4.6 percent drop.

“We’re going to see a lot of the risk-off trades come back into the picture during the rest of the week,” said Robert Sinche, global head of currency strategy at Royal Bank of Scotland Plc in Stamford, Connecticut. “We continue to see euro- dollar move with equity prices and risk in general.”

A Credit Suisse AG index shows traders are betting the ECB will cut its key rate by 20 basis points, or 0.2 percentage point, in the next 12 months. A month ago, they wagered it would raise rates by 22 basis points.

The euro extended losses after the European Commission in Brussels said an index of executive and consumer sentiment in the single-currency region fell to 98.3 in August from a revised 103 in July. That’s the lowest since May 2010 and below the 100.2 reading predicted.

Aug 9 FOMC minutes:

"Uncertainty surrounding the outlook" rose appreciably and recognized "increase in the downside risks" to growth. FOMC discussed "range of policy tools available to promote a stronger econ recovery" incl forward guidance, more asset buys, increase avg mat'y of holdings, reduce IOER. Some said no tools would likely do much and would risk boosting inflation. Agreed on 2 days for Sept FOMC to discuss. Most thought mon-pol "could contribute importantly to better outcomes"; some saw add'l accommodation needed because unemployment rate is high. Forward guidance seen as "measured response" but a few wanted a more substantial move and accepted the stronger guidance as step in that direction. "Three members dissented because they preferred to retain the forward guidance language employed in the June statement." Rejected conditioning FF rate on explicit numerical values for unemployment or inflation, with arguments on both sides. Most said conditional FF expectation thru mid-2013 provided useful guidance; some noted this did not remove flexibility to adjust later.

European data for Wednesday starts at 0600GMT with German retail sales and also the ILO measure of unemployment. This is followed at 0755GMT by the main German unemployment data, which is expected to show a -9k change and rate at 7.0%. European data continues at 0900GMT with the EMU unemployment rate, which is expected to remain at 9.9% and also flash HICP data for August, which is expected to come in at 2.5% y/y. Also in Europe today, from 0730GMT, the German government meets to approve measures decided at a eurozone summit in July with the following press conference due to take place in Berlin at 1130GMT US data starts at 1100GMT with the weekly MBA Mortgage Application Index, which is followed at 1130GMT by Challenger Layoffs and at 1215GMT by the ADP National Employment Report before the 1230GMT release of the latest ISM-NY Business Index. At 1345GMT, the Chicago PMI

is expected to fall to a reading of 53.0 in August after falling in July. Other regional data already released have suggested significant contraction. This is followed at 1400GMT by Factory Orders and also the latest Help-wanted Online index. Factory new orders are forecast to rise 2.0% in July. Durables orders were already reported up 4.0% in the month on a spike in aircraft orders.

Weekly EIA Crude Oil Stocks data is due at 1430GMT. Then, at 1530GMT, Atlanta Fed President Dennis Lockhart is due to deliver a speech on the economy to the Greater Lafayette Chamber of Commerce. Late US data includes the 1900GMT release of Agriculture Prices for August.

Resistance 3: Y78.00/10

Resistance 2: Y77.70

Resistance 1: Y77.10

Current price: Y76.59

Support 1:Y76.50

Support 2:Y75.90

Support 3:Y75.50

Resistance 3: Chf0.8520

Resistance 2: Chf0.8400

Resistance 1: Chf0.8260

Current price: Chf0.8163

Support 1: Chf0.8010

Support 2: Chf0.7880

Support 3: Chf0.7810

Comments: Rate holds below yesterday's highs and strong resistance at Chf0.8260 (channel line from the mid-Feb). Further rise may extend to Chf0.8400 and Chf0.8520 (Jul 01 high). Support is near Chf0.8000/10 (earlier resistance). Friday's lows come at Chf0.7880/85 with a break under targets Chf0.7810 (Aug 19 lows).

Resistance 3:$1.6620

Resistance 2:$1.6570

Resistance 1: $1.6460

Current price: $1.6308

Support 1: $1.6250

Support 2: $1.6200

Support 3: $1.6160

Comments: Rate consolidates after yesterday's fall. Strong resistance is around $1.6460 (61.8% Fibo of decline from Aug 19 high). Back above will target $1.6570 (Aug 12 high). Stronger resistance comes at $1.6620 (Aug 19 high). Minor support is near $1.6250 (Aug 30 base), stronger - at $1.6200/10 (Aug 26 lows). Below losses may widen to $1.6160 (Aug 12 lows).

Resistance 3: $1.4650

Resistance 2: $1.4580

Resistance 1: $1.4550

Current price: $1.4497

Support 1: $1.4390

Support 2: $1.4330

Support 3: $1.4260

Comments: Rate remains under pressure. Support is around yesterday's lows on $1.4390, stronger - at $1.4330 (Friday's low). Break under opens the way to Aug 19 low on $1.4260. Break above $1.4550 opens the way to $1.4580 (Jul 04 high).

Nikkei 225 +102.55 +1.16% 8,953.90

FTSE 100 +138.74 +2.70% 5,268.66

CAC 40 +5.54 +0.18% 3,159.74

DAX -26.15 -0.46% 5,643.92

Dow +67.17 +0.58% 11,606.42

Nasdaq +23.16 +0.90% 2,585.27

S&P 500 +6.86 +0.57% 1,216.94

10 Year Yield 2.18% -0.09 --

Oil $88.76 +1.49 +1.71%

Gold $1,835.40 +5.60 +0.31%

05:00 Japan Housing starts (July) Y/Y 4.9% 5.8%

05:00 Japan Construction orders (July) Y/Y - 6.0%

06:00 Germany Retail sales (July) real adjusted -1.5% 6.3%

06:00 Germany Retail sales (July) real unadjusted Y/Y - -1.0%

07:55 Germany Unemployment (August) seasonally adjusted -9.7K -11K

07:55 Germany Unemployment (August) seasonally adjusted, mln - 2.957

07:55 Germany Unemployment rate (August) seasonally adjusted 7.0% 7.0%

07:55 Germany Unemployment (August) seasonally unadjusted, mln - 2.939

07:55 Germany Unemployment rate (August) seasonally unadjusted - 7.0%

09:00 Italy CPI (August) preliminary 0.2% 0.3%

09:00 Italy CPI (August) preliminary Y/Y 2.6% 2.7%

09:00 Italy HICP (August) preliminary Y/Y - 2.1%

09:00 Italy PPI (August) - 0.1%

09:00 Italy PPI (August) Y/Y - 4.7%

09:00 EU(17) Harmonized CPI (August) Y/Y preliminary 2.5% 2.5%

09:00 EU(17) Unemployment (July) 9.9% 9.9%

12:15 USA ADP employment (August) +101K +114K

13:45 USA Chicago PMI (August) 52.0 58.8

14:00 USA Factory orders (July) 1.9% -0.8%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers