- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 27-05-2011

The major market averages continue to trade in the middle of today's range with the Nasdaq (+0.5%) slightly outpacing gains in the Dow (+0.4%) and S&P (+0.4%).

Financials have been among the best performers all session long, piggybacking gains from their European counterparts after the Financial Times reported European banks may be able to sidestep some of the Basel III capital requirements. Shares of Bank of America (BAC 11.73, +0.27) and Wells Fargo (WFC 28.37, +0.67) are among the best performing stocks in the sector on reports that U.S. banks and state attorneys were close to an agreement on the foreclosure front.

Barclays says private payrolls remain the key metric in the employ report and they "anticipate a slowing to just 207K here (from a 3-month trend of around 250K). This estimate takes into account a sizeable positive impact from the hiring spree McDonalds implemented in late April (which reportedly netted about 60K jobs)."

The major equity averages have spent the past couple of hours trading sideways near their session highs. Financials have managed to click higher, however; they are now up 0.9%, which makes them second to only the 1.3% advance of the materials sector.

Part of the financial sector's strength is owed to favor for bank stocks following positive analyst commentary on many of the banks of Europe and a proposal in Basel III for more favorable requirements for banks. Strength in the space has the KBW Bank Index up 1.2%.

The dollar dropped as U.S. consumer spending rose less than forecast, adding to speculation the Federal Reserve will lag behind other central banks in raising interest rates.

U.S. consumer purchases rose 0.4% in April after a revised 0.5% gain in March that was smaller than previously estimated, Commerce Department data showed.

The dollar extended its loss versus the yen as National Association of Realtors data showed pending home resales in the U.S. plunged almost 12% in April. Economists had a forecast of 1% drop.

“In the past few days we’ve gotten a lot of weak data out of the U.S., so that’s fueling speculation of longer-term accommodation by the Fed, and that’s obviously going to weigh on the U.S. dollar,” said Eric Viloria, senior currency strategist at Gain Capital Group LLC.

“The overall tone is dollar weakness,” said Mark McCormick, a currency strategist at Brown Brothers Harriman & Co. “The Fed is going to remain on hold, the data we’re getting, risk appetite and the story in the equity markets - this is weak for the dollar.”

The Swiss franc rallied to a record against the euro and greenback as Europe’s sovereign-debt crisis encouraged demand for a refuge and Switzerland’s leading economic indicator held at the highest level in almost five years. The KOF Swiss Economic Institute said its leading economic indicator was at 2.30, unchanged from April, which was the highest since August 2006. Economists forecast a drop to 2.22.

The franc has gained 4.6% this year.

The euro has weakened 2.5% over the past month.

“Concerns about sovereign debt are spreading in the region, weighing on the euro,” said Masahide Tanaka, a senior strategist at Mizuho Trust & Banking Co..

The yen dropped against the franc and the euro after Fitch lowered Japan’s outlook to negative from stable.

EUR/USD breaks above overnight highs ($1.4287) to test $1.4298 but stalls ahead of $1.4300. Stops seen over $1.4310. Offers then at $1.4320 (55-day moving average) and again $1.4335/45. Larger stops over $1.4350 (May 20 peak at $1.4345).

Stocks have held steady near the top end of today's trading range for about an hour. Meanwhile, Treasuries have trimmed their losses. In turn, the benchmark 10-year Note is now at the neutral line. The U.S. Treasury market will close earlier today, due to observation of Memorial Day on Monday.

- ECB flexible;

- ECB monetary stance remains accommodative;

- EMU inflation risks are on the upside;

- Higher headline HICP largely reflects commodity prices;

- See EMU HICP back below 2% next year.

- ECB flexible;

- ECB monetary stance remains accommodative;

- EMU inflation risks are on the upside;

- Higher headline HICP largely reflects commodity prices;

- See EMU HICP back below 2% next year.

- Downplays talk Greece may not get next tranche of EMU-IMF loans;

- Robust privatization can give Greece market trust;

- Will take time for Greece to regain credibility;

- Would welcome foreign expertise in privatization;

- Rejects any form of restructuring;

- Restructuring would damage Greece and Eurozone;

- Talk of Eurozone exit is "entirely ridiculous";

- Confident Greek banks can raise capital.

- Downplays talk Greece may not get next tranche of EMU-IMF loans;

- Robust privatization can give Greece market trust;

- Will take time for Greece to regain credibility;

- Would welcome foreign expertise in privatization;

- Rejects any form of restructuring;

- Restructuring would damage Greece and Eurozone;

- Talk of Eurozone exit is "entirely ridiculous";

- Confident Greek banks can raise capital.

Gold breaks above $1532.50 (61.8% Fibonacci retrace of the life-time peaks of $1575.79 seen May 2 and the $1462.50 low seen May 5) to post a high of $1535.10 before retreat. A close above $1532.50 will be needed for upward momentum to mount.

USD/JPY Y80.00, Y80.10, Y80.75, Y81.00, Y81.60-65, Y81.70-75, Y81.90, Y82.00

EUR/JPY Y113.80, Y114.00, Y115.10, Y116.00, Y117.00

AUD/USD $1.0600, $1.0675, $1.0700, $1.0705, $1.0720, $1.0760

U.S. stocks were headed for slight gains early Friday, after a report on personal income and spending came in as expected.

Trading could be tight Friday, as investors are often reluctant to place big bets ahead of a long weekend. The stock market will be closed Monday for the Memorial Day holiday.

Economy: Personal incomes rose 0.4% in April, after rising at the same rate in March, the government said.

Spending by individuals in the month also rose 0.4%, down slightly from 0.5% the month before. Economists had forecast a 0.5% rise.

Shortly after the opening bell, the University of Michigan will put out its final reading on consumer sentiment in May. Economists expect the figure to remain unchanged at 72.4.

The National Association of Realtors is expected to report a 1.4% decline in pending home sales for the month of March.

Companies: Toyota (TM), Nissan (NSANY) and Honda (HON, Fortune 500) all reported sharp declines in sales and production during April, as the fallout from the March 11 earthquake and tsunami continue to take a toll on Japan's auto industry.

PayPal and its parent company eBay (EBAY, Fortune 500) are suing Google (GOOG, Fortune 500) for allegedly stealing trade secrets related to mobile payment technology.

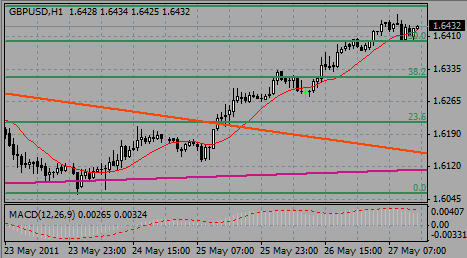

GBP/USD extended session highs to $1.6465, above earlier higs on $1.6461. But resistance in the $1.6465/85 area capped the rise. A break above opens a move toward $1.6500 and then - to a stronger offers at $1.6520 ($1.6518 May 11 high) and $1.6540/50 ($1.6544 May 5 high).

GBP/USD heads for earlier highs on $1.6461, with a break above targets the key resistance area between $1.6465/85. A break here to open potential for $1.6585, while if area contains there is a risk of deeper correction, with supports to be worked out for the retracement of the move up from $1.6055.

Data released:

06:00 UK Nationwide house price index (May) 0.3% 0.1% -0.2%

06:00 UK Nationwide house price index (May) Y/Y -1.2% -1.7% -1.3%

08:00 EU(17) M3 money supply (April) adjusted Y/Y 2.0% 2.3% 2.3%

08:00 EU(17) M3 money supply (3 months to April) adjusted Y/Y 2.1% 2.3% 2.0%

09:00 EU(17) Economic sentiment index (May) 105.5 105.8 106.2

09:00 EU(17) Business climate indicator (May) 0.99 1.20 1.28

The dollar weakened for a second day against the euro and the yen before reports that economists said will show U.S. consumer spending slowed in April and pending home sales declined.

The yen declined against the European common currency as Japan had its credit outlook revised down by Fitch Ratings.

“The market is more concerned about the U.S. than it is about Europe,” said Sonja Marten, a currency strategist at DZ Bank AG. “We have weak growth in the U.S. When you look at the debt situation in the euro zone as a whole, it’s much better than in the U.S. More importantly, they’re doing something about it.”

The euro headed for a weekly loss versus the franc and the yen. A European Commission report today showed an index of executive and consumer sentiment in the region slid to 105.5 this month from 106.2 in April. The median estimate of economists was 105.7.

Luxembourg Prime Minister Jean-Claude Juncker said yesterday the International Monetary Fund may not release its share of a 12 billion-euro aid package to Greece next month.

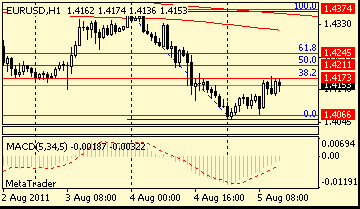

EUR/USD rose to $1.4280 before rate corrected to $1.4230. Next attenpt to gain ground failed to break the session higha and euro weakened to $1.4185. Later rate recovered to $1.4244.

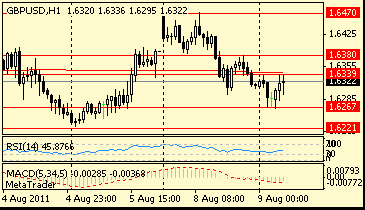

GBP/USD printed session high on $1.6460 before set stable around $1.6400/40.

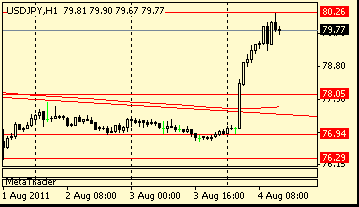

USD/JPY broke channel support line from May 05 at Y81.20 and showed lows near Y80.80.

US data starts at 1230GMT with the personal income report that is expected to rise 0.4% in April. Growth in U.S. consumer spending slowed to 0.5 percent in April, the smallest gain in three months, according to a survey.

At 1355GMT, the Michigan Sentiment Index is expected to be unrevised at a reading of 72.4 in May.

At 1400GMT release of NAR Pending Home Sales is scheduled.

Pending home sales fell 1% in April, economists predict the National Association of Realtors will say today.

“All things considered, the weak fundamental data should provide a ‘sell dollars’ environment,” Sacha Tihanyi, a senior currency strategist at Scotia Capital.

The Bank of Japan said it posted a record low net profit of Y52.1 billion in fiscal 2010, because the yen's rise eroded the value of its investment in foreign securities. The sharp decline from its previous years' net profit of Y367.1 billion was mainly due to lower profits and higher losses incurred by foreign exchange transactions amid the appreciation of the yen. The losses from forex fluctuations totaled Y481.0 billion in fiscal 2010, more than double the Y218.5 billion seen in fiscal 2009.

Gold again holds within the range range as the daily Bollinger band narrows, indicating reduced volatility. Daily studies are mostly bullish. Initial resistance seen at $1530.90/1532.10 (highs from the previous two sessions). Support seen between $1512.10/1514.60 (21-DMA, the 23.6% Fib of $1309/1576 and a 2-week support line).

The dollar tumbled broadly on Friday after weak U.S. economic data dragged the 10-year Treasury yield down to a six-month low overnight, with the greenback's drop gaining steam on a flurry of stop-loss selling.

The dollar fell across the board, hitting a record low against the Swiss franc and a three-year low versus the New Zealand dollar.

The dollar hit a record low against the Swiss franc of Chf0.8534.

The New Zealand dollar marked a three-year high of $0.8200.

"The dollar has been strong since the start of May but it looks like that outperformance may be coming to a close," said Junya Tanase, foreign exchange strategist at JPMorgan Chase in Tokyo. "Even if Greece's problems continue to weigh on the euro, if the dollar does not strengthen much, then the euro's downside against the dollar may gradually become limited," he said.

The euro has turned higher after its drop this week stalled right near its 100-day moving average and also the bottom of the cloud on daily Ichimoku charts.

The dollar retreated after data on Thursday showed fresh signs of a slowdown in the U.S. labour market and the second estimate of first quarter U.S. growth came in below forecasts, spurring a decline in the 10-year Treasury yield to a six-month low.

"All eyes are on U.S. employment data out next Friday," said Teppei Ino, currency analyst at Bank of Tokyo-Mitsubishi UFJ. "If those figures also come in below the market's expectations, the market may get excited about the possibility of QE3 or some other form of monetary easing, putting more pressure on the dollar," Ino said.

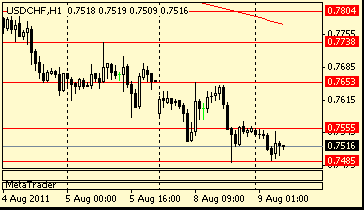

EUR/CHF extends life lows below Asian lows at Chf1.2168. Currently the cross trading down to Chf1.2166. If rate can clear lower expected to meet next support at Chf1.2105/1.2095.

USD/JPY Y80.00, Y80.10, Y80.75, Y81.00, Y81.60-65, Y81.70-75, Y81.90, Y82.00

EUR/JPY Y113.80, Y114.00, Y115.10, Y116.00, Y117.00

AUD/USD $1.0600, $1.0675, $1.0700, $1.0705, $1.0720, $1.0760

Hang Seng +0.95% 23,118

Shanghai Composite -0.97% 2,709.95

Nikkei -0.42 9521.94

The dollar dropped against the yen as the economy grew less than forecast and jobless-benefit claims unexpectedly rose, adding to speculation the U.S. will lag behind other nations in raising interest rates.

Initial claims for unemployment benefits rose by 10,000 to 424,000 in the week ended May 21, Labor Department figures showed today. The median estimate of economists called for a drop to 404,000.

The euro fell to a record low against the Swiss franc after Luxembourg’s Jean-Claude Juncker, who heads euro-area finance ministers, said the International Monetary Fund may not release its share of aid to Greece next month.

The IMF said in a report today that Switzerland’s central bank should start raising borrowing costs to fight emerging price pressures as the economy strengthens.

The euro earlier rose versus the dollar after European Central Bank President Jean-Claude Trichet said policy makers are “carefully” monitoring inflation, fueling bets the region’s economy is strong enough for higher borrowing costs.

The ECB raised its main refinancing rate to 1.25% last month after keeping it at a record low of 1% for almost two years. The Fed has held its target rate at zero to 0.25% since December 2008. It’s forecast to keep the benchmark unchanged until the first quarter of 2012.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers