- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 26-08-2011

USD/CHF holds at Chf0.8056, a bit lower earlier set session highs on Chf0.8160. Support at Chf0.8000/10 (earlier broken support). Strong support comes at overnight lows on Chf0.7880/85.

The stock market continues to drift along its session high. Despite the stocks gains, Treasuries have performed well all session. In fact, buying interest has kept the yield on the benchmark 10-year Note near or below 2.20%.

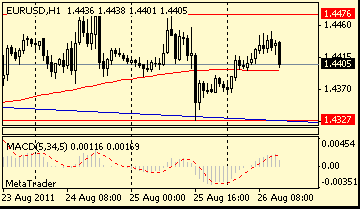

EUR/USD holds higher, a bit lower session high on $1.4483. Rate earlier printed session high on $1.4500 with stops above. Further oggers at $1.4520.

The dollar gained after Federal Reserve Chairman Ben S. Bernanke failed to signal new measures to shore up the economy that would risk debasing the greenback.

Bernanke said the central bank still has tools to stimulate the economy without signaling when or whether policy makers might deploy them.

“The key point from the speech was that he didn’t signal any new Federal Reserve easing,” said Nick Bennenbroek, head of currency strategy at Wells Fargo & Co..

Last year at the conference, Bernanke said the Fed would “do all that it can” to ensure a continuation of the economic recovery and that buying more debt might be warranted if growth slowed. Two months later, policy makers announced a $600 billion second round of asset purchases that ended in June.

The euro pared earlier gains after Commerce Department data showed U.S. gross domestic product grew at a 1% annual rate from April through June, down from a 1.3% prior estimate. The median forecast of economists called for a 1.1% increase.

The global economy has a 50% chance of slipping into recession as the economies of Europe and the U.S. struggle to grow, the Nobel laureate and New York University professor Michael Spence said yesterday.

The dollar has declined 1.4% in the past three months. The euro has appreciated 0.3% and the yen has gained 4.8%.

The yen advanced for the first time in three days versus the dollar as Japan’s Prime Minister Naoto Kan said he was stepping down.

“I feel I’ve done everything I could under these difficult conditions,” Kan told Democratic Party of Japan lawmakers at a nationally televised meeting today.

The Swiss franc weakened against most major counterparts after an index of leading indicators dropped more than economists forecast, adding to signs the currency’s recent strength may be damaging the nation’s growth.

Stocks have recovered back from their morning slide.

Tech stocks have emerged as leaders today. Despite their recent dip, tech stocks continue to collectively sport a 1.0% gain. Shares of Apple (AAPL 378.94, +5.22) have been integral in the sector's move. Thanks to its climb today, the stock has now fully offset the prior session's loss, which came in response to news that the company's heralded CEO, Steve Jobs, plans to resign from the company.

EUR/USD $1.4275, $1.4395, $1.4400, $1.4500

USD/JPY Y76.00, Y77.00

EUR/JPY Y110.50

GBP/USD $1.6375, $1.6500

USD/CHF Chf0.8000

AUD/USD $1.0400, $1.0290

AUD/JPY Y81.00

US data: 12.30 GMT Q2 GDP revisions. Est +1% real growth. At 13.55 GMT Aug U-Mich final consumer sentiment is dua. Est 55.5.

14:.00 GMT Fed Jackson Hole- Bernanke on near-term prospects.

GBP/USD

Offers $1.6480, $1.6450/55, $1.6430/35, $1.6380/400, $1.6350

Bids $1.6280/75, $1.6260/50, $1.6235/30, $1.6200, $1.6168

Offers $1.4580, $1.4535/50, $1.4520, $1.4485/500, $1.4475

A lack of direction is evident on the daily oil chart, while daily studies remain mixed to neutral. The break of long-term support will remain in focus as there is little other impetus to be seen. Initial support seen at $81.59, the former 23.6% Fibo level of $100.62/75.71. Next support seen at $80.28, the 23 Nov 2010 reversal low. Strong resistance seen at $86.51, the 21-DMA.

deficit cut plan has made UK a safe haven

global instability bolsters case for deficit cutting

must tackle vested interests blocking growth

Data released:

08:00 EU(17) M3 money supply (July) adjusted Y/Y 2.0% 2.3% 2.1%

08:00 EU(17) M3 money supply (3 months to July) adjusted Y/Y 2.1% 2.3% 2.2%

08:30 UK GDP (Q2) revised 0.2% 0.2% 0.2%

08:30 UK GDP (Q2) revised Y/Y 0.7% 0.7% 0.7%

The dollar weakened against most of its major counterparts as traders awaited a speech by Federal Reserve Chairman Ben S. Bernanke and a report forecast to show the world’s biggest economy is slowing.

The U.S. currency headed for a second weekly loss versus the euro and fell the most today against the Norwegian krone and New Zealand dollar. Bernanke will speak today at the Kansas City Fed’s annual economic conference in Jackson Hole, Wyoming, and may announce further measures to expand monetary easing. The yen rose against 15 of its 16 major peers after Japan’s Prime Minister Naoto Kan said he’s resigning 14 months into the job.

“There probably won’t be immediate further stimulus but we think Bernanke will acknowledge that the Fed is absolutely ready to act if the data shows any further deterioration in the economy,” said Neil Mellor, a currency strategist at Bank of New York Mellon Corp. in London. “If he conveys that there is absolutely no way the Fed will allow the U.S. economy to deteriorate, and that they will use all policy tools at their disposal, then it will be risk-on and the dollar will weaken.”

EUR/USD reached $1.4450 in recovering from overnight lows on $1.4370.

GBP/USD reached resistance seen into $1.6350 ahead of reported corporate sell interest placed between $1.6380/00, with topside stops noted between $1.6405/10. Support seen into $1.6280/75, stronger between $1.6260/50 with stops below.

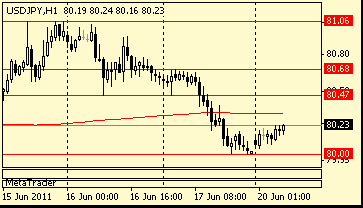

USD/JPY eased under Y77.00.

All week, markets have been waiting for Fed Chairman Ben Bernanke's speech at the annual Jackson Hole forum. The wait is over at 1400GMT. Ahead of then, at 0600GMT, Germany releases import prices for July, which are expected to come in unchanged m/m, 6.4% y/y. Also at 0600GMT, the France manufacturing investment survey is due, followed at 0800GMT by M3 data from the ECB, which is expected to come in at 2.2% with M3 lending at 2.5%. UK data sees the second estimate of Q2 GDP along with the June Index of Services data at 0830GMT. The risks are of a small downward revision to Q2 GDP, with final industrial production coming in weaker than expected, although the median forecast is for growth to remain at 0.2% q/q, 0.7% y/y.

Resistance seen into $1.6350 ahead of reported corporate sell interest placed between $1.6380/00, with topside stops noted between $1.6405/10. Support seen into $1.6280/75, stronger between $1.6260/50 with stops below. A break here to allow for a move toward the 55-DMA at $1.6225 ahead of $1.6200 and $1.6180/70.

Majors close

Nikkei +132.75 (+1.5%) 8,772.36

Topix +9.58 (+1.3%) 751.82

DAX -96.94 (-1.71%) 5,584

CAC -20.55 (-0.65%) 3,119

FTSE-100 -74.75 (-1.44%) 5,131

Dow -170.81 (-1.51%) 11,149.90

Nasdaq -48.06 (-1.95%) 2,420

S&P500 -18.33 (-1.56%) 1,159

Oil -0.32 (-0.38%) $84.98

10-Years 2.22% -0.04

Japanese stocks rose, pushing up the Nikkei 225 (NKY) Stock Average the most in almost two months, after better-than-estimated U.S. economic data improved the earnings outlook for exporters.

The Topix has lost about 11 percent this month amid concern U.S. growth is sputtering and Europe’s debt crisis will damage the banking system, damping demand in two of Japan’s biggest export markets.

Toyota Motor Corp. (7203), which gets 28 percent of its sales in the U.S. and Canada, rose 1.7 percent after demand for cars boosted orders for U.S. durable goods the most in four months.

Sony Corp. (6758), Panasonic Corp. (6752) and other Japanese technology companies gained as shares of Apple Inc. dropped in after-hours trading following Steve Jobs’ resignation as the firm’s chief executive officer.

Panasonic, an electronics maker which yesterday dropped to its lowest level since 1980, climbed 3.8 percent to 792 yen.

Nippon Electric Glass Co. rose 6.1 percent to 751 yen. Goldman Sachs Group Inc. boosted its investment rating on the glassmaker to “buy” from “neutral,” citing an increase in its market share and improved profit performance.

Hitachi Chemical Co. climbed 4.4 percent to 1,287 yen after the maker of chemical products said it will establish a subsidiary in India.

EU stocks tumbled, pushing the DAX Index (DAX) down as 4 percent during one 15-minute stretch, as traders rushed to sell futures to hedge equities amid speculation bans on short selling would be extended.

German shares have declined more than gauges in France, Spain and Italy.

The DAX has dropped for the past four weeks as concern escalated that the global economy is slowing and the euro-area debt crisis spread to Italy and Spain, bringing the decline from this year’s high on May 2 to 26 percent.

After the close of trading today, French, Italian and Spanish regulators extended temporary bans on short selling introduced this month. Spain and Italy lengthened their restrictions through Sept. 30 and France said its prohibitions could last as long as Nov. 11.

The three countries, along with Belgium, imposed bans on short-selling of some financial stocks in an effort to stabilize markets after European banks including Societe Generale SA hit their lowest levels since the credit crisis of 2008.

Utilities and chemical companies led the selloff in Frankfurt. EON AG, the nation’s biggest power company, dropped 3.1 percent to 14.68 euros while RWE AG retreated 3.9 percent to 25.37 euros.

BASF SE (BAS), the world’s largest chemical company, retreated 3.3 percent to 48.25 euros and K&S AG, Europe’s biggest potash producer, lost 2.9 percent to 43.32 euros.

U.S. stocks were lower Thursday afternoon, as investors hit the brakes following a 3-day advance, and as nervousness about Europe's debt crisis returned to the spotlight.

Investors also grew anxious about Europe, amid rumors that ratings agencies may downgrade the credit rating in Germany -- Europe's largest economy.

Standard and Poor's, Fitch Ratings and Moody's Investors Services said Thursday that they did not have any updates to their AAA-rating on Germany.

This week's three-day stock advance in the U.S. has been attributed to investor hopes that Fed chief Ben Bernanke will announce steps on Friday to spur the faltering economy at the Kansas City Fed's annual retreat in Jackson Hole, Wyo.

At last year's meeting, Bernanke prepared the market for QE2 -- a bond-buying program that is widely credited for supporting stocks earlier this year.

Companies: Financial stocks were the biggest winners Thursday, as investors reacted to Warren Buffett's $5 billion bet on battered shares of Bank of America (BAC, Fortune 500). The news was a welcome surprise, since Bank of America shares have been hammered recently and are down roughly 40% over the past month

Shares of the Charlotte, N.C.-based bank rallied 9%, making it the biggest gainer on the Dow and the S&P 500 indexes.

Other bank stocks were right behind BofA with healthy gains. Morgan Stanley (MS, Fortune 500) and Citigroup (C, Fortune 500) were up between 3% and 4%, while US Bancorp (USB, Fortune 500) and Wells Fargo (WFC, Fortune 500) also edged higher.

Meanwhile, shares of Apple (AAPL, Fortune 500) dipped almost 1% after co-founder and two-time CEO Steve Jobs resigned late Wednesday.

Former Chief Operating Officer Tim Cook will replace Jobs, who will remain chairman of the second-most valuable company in the world.

Economy: First-time claims for unemployment benefits rose more than expected, as a dispute between Verizon Communications (VZ, Fortune 500) and its union employees caused thousands of workers to seek jobless benefits

Ongoing claims, which include people filing for the second week of benefits or more, dropped to the lowest level since September 2008.

Data released:

10:00 UK CBI retail sales volume balance (August) -14% -10% -5%

12:30 USA Jobless claims (week to 20.08) 417K 416K 412 (408)K

20:30 USA M2 money supply (15.08), bln +5.1 - +43.1

23:30 Japan Nationwide CPI (July) 0.0% - -0.1%

23:30 Japan Nationwide CPI (July) Y/Y 0.2% - 0.2%

23:30 Japan Nationwide CPI ex fresh food (July) Y/Y 0.1% 0.0% 0.4%

23:30 Japan Tokyo-area CPI (August) 0.1% - 0.0%

23:30 Japan Tokyo-area CPI (August) Y/Y -0.2% - 0.5%

23:30 Japan Tokyo-area CPI ex fresh food (August) Y/Y -0.2% -0.2% 0.4%

The euro weakened against the dollar and pared gains versus the yen on concern regulators will need to extend a ban on short-selling in European equity markets to prevent the region’s sovereign-debt crisis from worsening.

Better-than expected durable-goods orders and home-price data from the U.S. curbed speculation Fed Chairman Ben S. Bernanke will announce a third round of bond purchases that boost the supply of dollars, known as quantitative easing, when he speaks tomorrow at a symposium at Jackson Hole, Wyoming.

“Expectations for QE3 have been pared down because the recent economic data isn’t conclusive” enough to warrant urgent action, said Sim Moh Siong, a foreign-exchange strategist at Bank of Singapore Ltd. The dollar’s strength “is consistent” with those expectations, he said.

U.S. house prices rose 0.9% in June from the month before, the biggest increase since September 2005, a report showed yesterday. Durable-goods orders jumped 4% in July from a year earlier, following a revised 1.3% contraction the previous month.

The pound fell to the lowest level in more than two weeks against the euro as a report showed U.K. consumer confidence dropped in July, fueling concern the economic recovery will falter.

Sterling reached its lowest against the dollar since Aug. 17. Nationwide Building Society said its index of sentiment declined 2 points to 49 from June, the lowest reading since April. A gauge of consumers’ expectations for the economy in the next six months slipped 3 points to 67, the customer-owned lender said in an e-mailed report today. The pound declined as stock-market gains across Europe sapped demand for the nation’s bonds as a haven from the euro area’s debt crisis.

All week, markets have been waiting for Fed Chairman Ben Bernanke's speech at the annual Jackson Hole forum. The wait is over at 1400GMT. Ahead of then, at 0600GMT, Germany releases import prices for July, which are expected to come in unchanged m/m, 6.4% y/y. Also at 0600GMT, the France manufacturing investment survey is due, followed at 0800GMT by M3 data from the ECB, which is expected to come in at 2.2% with M3 lending at 2.5%. UK data sees the second estimate of Q2 GDP along with the June Index of Services data at 0830GMT. The risks are of a small downward revision to Q2 GDP, with final industrial production coming in weaker than expected, although the median forecast is for growth to remain at 0.2% q/q, 0.7% y/y.

EUR/USD $1.4275, $1.4395, $1.4400, $1.4500

USD/JPY Y76.00, Y77.00

EUR/JPY Y110.50

GBP/USD $1.6375, $1.6500

USD/CHF Chf0.8000

AUD/USD $1.0400, $1.0290

AUD/JPY Y81.00

Resistance 3: Y80.20

Resistance 2: Y78.20

Resistance 1: Y77.80

Current price: Y76.98

Support 1:Y76.80

Support 2:Y76.40

Support 3:Y75.90

Comments: closest support at yesterday's session lows Y76.80, ahead of Wednesday base Y76.40/45 and Y75.90. Resistance spotted at Y77.80 (38.2% Y80.20-Y75.90), ahead of Y78.20.

Resistance 3: Chf0.8140

Resistance 2: Chf0.8010/15

Resistance 1: Chf0.7945

Current price: Chf0.7900

Support 1: Chf0.7790

Support 2: Chf0.7660

Support 3: Chf0.7540

Comments: Resistance is around session's highs on Chf0.7945, stronger - at Chf0.8010/15 (Aug 17 highs). Further rise may extend Chf0.8140 (channel line from the mid-Feb). Strong support comes at Chf0.7790 (23.6% Fibo of Chf0.7070 - Chf0.8020). Below losses may widen to Chf0.7660 (38.6%) and Chf0.7540 (Aug 12 lows).

Resistance 3:$1.6620

Resistance 2:$1.6530

Resistance 1: $1.6390

Current price: $1.6332

Support 1: $1.6250

Support 2: $1.6160

Support 3: $1.6100

Comments: cable tries to rebound. Minor resistance $1.6390. Further resistance is near Monday's highs on $1.6530, stronger - at $1.6620 (Friday's high). Further rise may extend to $1.6660. Support is near $1.6250 (50% of the rise from Aug 11). Below losses may widen to $1.6160.

Resistance 3: $1.4580

Resistance 2: $1.4520

Resistance 1: $1.4500

Current price: $1.4431

Support 1: $1.4340

Support 2: $1.4260

Support 3: $1.4150

Comments: Support remains at $1.4340 (overnight lows). Below there is a chance for a test of stronger level - at $1.4260 (Friday's low). Further resistance comes at $1.4520 (Aug 17 high). Further rise may extend to $1.4580 (Jul 04 high).

Spreadbetters Cantor Index are calling the FTSE down 1, the DAX down 34, the CAC down 12 and the Eurostoxx 50 down 9.

Nikkei +132.75 (+1.5%) 8,772.36

Topix +9.58 (+1.3%) 751.82

DAX -96.94 (-1.71%) 5,584

CAC -20.55 (-0.65%) 3,119

FTSE-100 -74.75 (-1.44%) 5,131

Dow -170.81 (-1.51%) 11,149.90

Nasdaq -48.06 (-1.95%) 2,420

S&P500 -18.33 (-1.56%) 1,159

Oil -0.32 (-0.38%) $84.98

10-Years 2.22% -0.04

06:00 Germany Import prices (July) 0.3% -0.6%

06:00 Germany Import prices (July) Y/Y 7.0% 6.5%

06:00 Germany Import prices excluding oil (July) Y/Y - 4.0%

08:00 EU(17) M3 money supply (July) adjusted Y/Y 2.3% 2.1%

08:00 EU(17) M3 money supply (3 months to July) adjusted Y/Y 2.3% 2.2%

08:30 UK GDP (Q2) revised Y/Y 0.2% 0.2%

08:30 UK GDP (Q2) revised Y/Y 0.7% 0.7%

12:30 USA GDP (Q2) revised Y/Y 1.1% 1.3%

12:30 USA PCE price index (Q2) revised - 3.1%

12:30 USA PCE price index ex food, energy (Q2) revised - 2.1%

13:55 USA Michigan sentiment index (August) final 56.0 54.9

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers