- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 22-03-2018

| Pare | Closed | % change |

| EUR/USD | $1,2305 | -0,27% |

| GBP/USD | $1,4099 | -0,27% |

| USD/CHF | Chf0,9487 | -0,01% |

| USD/JPY | Y105,31 | -0,71% |

| EUR/JPY | Y129,59 | -0,98% |

| GBP/JPY | Y148,461 | -0,99% |

| AUD/USD | $0,7695 | -0,88% |

| NZD/USD | $0,7207 | -0,25% |

| USD/CAD | C$1,29297 | +0,21% |

| Time | Region | Event | Period | Previous | Forecast |

| 01:30 | Japan | National CPI Ex-Fresh Food, y/y | Февраль | 0.9% | 1% |

| 01:30 | Japan | National Consumer Price Index, y/y | Февраль | 1.4% | 1.7% |

| 14:00 | United Kingdom | BOE Quarterly Bulletin | | | |

| 14:10 | USA | FOMC Member Bostic Speaks | | | |

| 14:30 | Canada | Retail Sales YoY | | 5.8% | |

| 14:30 | Canada | Retail Sales, m/m | | -0.8% | 0.1% |

| 14:30 | Canada | Retail Sales ex Autos, m/m | January | -1.8% | 0% |

| 14:30 | Canada | Consumer Price Index m / m | January | 0.7% | 0.3% |

| 14:30 | Canada | Bank of Canada Consumer Price Index Core, y/y | January | 1.2% | 1.4% |

| 14:30 | Canada | Consumer price index, y/y | February | 1.7% | 1.6% |

| 14:30 | USA | Durable goods orders ex defense | February | -2.7% | |

| 14:30 | USA | Durable Goods Orders ex Transportation | February | -0.3% | -0.4% |

| 14:30 | USA | Durable Goods Orders | February | -3.7% | -0.1% |

| 16:00 | USA | New Home Sales | February | 0.593 | 0.611 |

| 16:30 | USA | FOMC Member Kashkari Speaks | February | | |

| 17:30 | USA | FOMC Member Kaplan Speak | February | | |

| 19:00 | USA | Baker Hughes Oil Rig Count | March | 800 | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | |

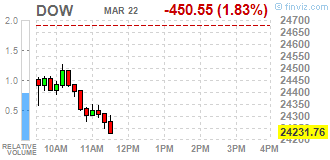

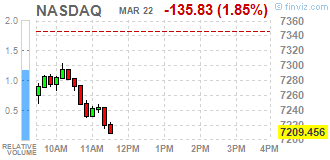

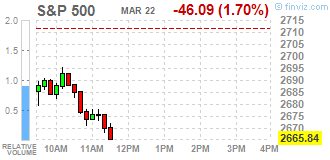

Major U.S. stock-indexes tumbled on Thursday, dragged down by a heavily-weighted financial sector, which fell as the U.S. Treasury yields dropped sharply, while the broad market sentiment was dented by growing threat of a global trade war as the Trump administration plans to impose import tariffs on China.

Most of Dow stocks in negative area (28 of 30). Top loser - Caterpillar Inc. (CAT, -3.81%). Top gainer - The Coca-Cola Co (KO, +0.37%).

Most of S&P sectors in negative area. Top loser - Basic Materials (-0.6%). Sole gainer - Utilities (+1.0%).

At the moment:

| Index/commodity | Last | Today's Change, points | Today's Change, % |

| Dow | 24260.00 | -467.00 | -1.89% |

| S&P 500 | 2671.50 | -46.75 | -1.72% |

| Nasdaq 100 | 6743.50 | -140.50 | -2.04% |

| Crude Oil | 64.38 | -0.79 | -1.21% |

| Gold | 1329.00 | +7.50 | +0.57% |

| U.S. 10yr | 2.80% | -0.10 | -3.58% |

March data revealed another strong increase in private sector output, together with a further solid payroll gain and elevated price pressures. At 54.3 in March, down from 55.8 in the previous month, the seasonally adjusted IHS Markit Flash U.S. Composite PMI Output Index has remained above the 50.0 no-change threshold for just over two years.

The latest upturn in business activity was faster than the average over this period, driven by solid rises in both manufacturing production and service sector output.

U.S. house prices rose in January, up 0.8 percent from the previous month, according to the Federal Housing Finance Agency (FHFA) seasonally adjusted monthly House Price Index (HPI). The previously reported 0.3 percent increase in December was revised upward to 0.4 percent.

The FHFA monthly HPI is calculated using home sales price information from mortgages sold to, or guaranteed by, Fannie Mae and Freddie Mac. From January 2017 to January 2018, house prices were up 7.3 percent.

For the nine census divisions, seasonally adjusted monthly price changes from December 2017 to January 2018 ranged from -0.7 percent in the West South Central division to +1.2 percent in the New England and Pacific divisions. The 12-month changes were all positive, ranging from +5.1 percent in the West South Central division to +10.0 percent in the Mountain division.

U.S. stock-index futures tumbled on Wednesday, as technology stocks led the way lower on fears of increased regulations in the wake of Facebook's (FB) data privacy issues, while investors assessed the outcomes of the latest meeting of the U.S. Federal Reserve and awaited Trump's announcement of tariffs on Chinese imports.

Global Stocks:

| Index/commodity | Last | Today's Change, points | Today's Change, % |

| Nikkei | 21,591.99 | +211.02 | +0.99% |

| Hang Seng | 31,071.05 | -343.47 | -1.09% |

| Shanghai | 3,263.83 | -17.12 | -0.52% |

| S&P/ASX | 5,937.20 | -13.10 | -0.22% |

| FTSE | ,958.87 | -80.10 | -1.14% |

| CAC | 5,170.35 | -69.39 | -1.32% |

| DAX | 12,162.86 | -146.29 | -1.19% |

| Crude | 64.63 | | -0.83% |

| Gold | 1,332.00 | | +0.79% |

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 47.9 | -0.05(-0.10%) | 1680 |

| ALTRIA GROUP INC. | MO | 59.81 | -0.19(-0.32%) | 3918 |

| Amazon.com Inc., NASDAQ | AMZN | 1,566.50 | -15.36(-0.97%) | 39752 |

| AMERICAN INTERNATIONAL GROUP | AIG | 55.91 | 0.07(0.13%) | 675 |

| Apple Inc. | AAPL | 169.85 | -1.42(-0.83%) | 250285 |

| AT&T Inc | T | 35.93 | -0.07(-0.19%) | 14304 |

| Barrick Gold Corporation, NYSE | ABX | 12.25 | -0.10(-0.81%) | 21725 |

| Boeing Co | BA | 334 | -3.10(-0.92%) | 12294 |

| Caterpillar Inc | CAT | 153.75 | -2.05(-1.32%) | 3750 |

| Chevron Corp | CVX | 116.19 | -0.85(-0.73%) | 440 |

| Cisco Systems Inc | CSCO | 43.8 | -0.51(-1.15%) | 24823 |

| Citigroup Inc., NYSE | C | 72.5 | -0.82(-1.12%) | 127148 |

| Deere & Company, NYSE | DE | 156.35 | -1.70(-1.08%) | 2105 |

| Exxon Mobil Corp | XOM | 74.7 | -0.34(-0.45%) | 11243 |

| Facebook, Inc. | FB | 165.51 | -3.88(-2.29%) | 680614 |

| FedEx Corporation, NYSE | FDX | 247.01 | -2.01(-0.81%) | 5945 |

| Ford Motor Co. | F | 11.04 | -0.06(-0.54%) | 11299 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 18.98 | -0.20(-1.04%) | 8198 |

| General Electric Co | GE | 13.82 | -0.06(-0.43%) | 32914 |

| General Motors Company, NYSE | GM | 37.57 | -0.01(-0.03%) | 809 |

| Goldman Sachs | GS | 259.5 | -2.35(-0.90%) | 7349 |

| Google Inc. | GOOG | 1,081.25 | -9.63(-0.88%) | 4844 |

| Hewlett-Packard Co. | HPQ | 23.15 | -0.13(-0.56%) | 21300 |

| Home Depot Inc | HD | 177.91 | -0.11(-0.06%) | 10535 |

| HONEYWELL INTERNATIONAL INC. | HON | 149.87 | -1.49(-0.98%) | 497 |

| Intel Corp | INTC | 51.08 | -0.48(-0.93%) | 55069 |

| International Business Machines Co... | IBM | 155.33 | -1.36(-0.87%) | 2902 |

| Johnson & Johnson | JNJ | 129.99 | -1.20(-0.91%) | 538 |

| JPMorgan Chase and Co | JPM | 113.11 | -1.63(-1.42%) | 24743 |

| McDonald's Corp | MCD | 158.2 | -0.46(-0.29%) | 1119 |

| Microsoft Corp | MSFT | 91.38 | -1.10(-1.19%) | 52627 |

| Nike | NKE | 66 | -0.35(-0.53%) | 2388 |

| Pfizer Inc | PFE | 36.15 | -0.12(-0.33%) | 3257 |

| Procter & Gamble Co | PG | 76.85 | -0.19(-0.25%) | 3158 |

| Tesla Motors, Inc., NASDAQ | TSLA | 313.3 | -3.23(-1.02%) | 22862 |

| The Coca-Cola Co | KO | 42.81 | -0.19(-0.44%) | 547 |

| Twitter, Inc., NYSE | TWTR | 32.1 | -0.63(-1.92%) | 116389 |

| United Technologies Corp | UTX | 126.85 | -0.15(-0.12%) | 210 |

| Verizon Communications Inc | VZ | 47.11 | -0.17(-0.36%) | 13764 |

| Visa | V | 122.85 | -0.37(-0.30%) | 8472 |

| Wal-Mart Stores Inc | WMT | 87.83 | -0.35(-0.40%) | 13626 |

| Walt Disney Co | DIS | 101.36 | -0.46(-0.45%) | 1425 |

| Yandex N.V., NASDAQ | YNDX | 43.03 | -0.18(-0.42%) | 2162 |

Facebook (FB) target lowered to $168 from $195 at Stifel

In the week ending March 17, the advance figure for seasonally adjusted initial claims was 229,000, an increase of 3,000 from the previous week's unrevised level of 226,000. The 4-week moving average was 223,750, an increase of 2,250 from the previous week's unrevised average of 221,500.

-

Firming short-term wage data provides "Increasing confidence" that wage and labour cost growth will pick up

-

Direct impact of U.S. tariff announcements likely limited but big increase in global protectionism would have "significant negative impact"

-

Any future increases in bank rate likely to be gradual and limited

-

Hourly productivity likely to fall in q1 2018, growth in output per head likely to remain weak at start of 2018

"The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 21 March 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion".

-

Indicators point to strong growth momentum; expansion may be better in near term than previously expected

-

Euro area labour markets continue to exhibit strong dynamics, further improvement expected

-

Sticks to current 2018 GDP growth forecast

-

Despite cold weather construction sector remains buoyant

-

Export expectations have fallen to lowest level in more than a year

In February 2018, the quantity bought in retail sales increased by 0.8% when compared with the previous month, with increases seen across all main sectors except non-food stores.

The monthly increase to the quantity bought follows two monthly declines in December and January, resulting in an overall decrease of 0.4% in the three months to February.

The year-on-year growth rate increased by 1.5% following a general slowdown when compared with an increase of 3.3% in February 2017; however, this stabilised in recent months as we see little movement in the year-on-year growth since November 2017.

While we continue to see price increases across all sectors, there is a slowdown to growth in the last two months, falling from 3.1% in December to 2.5% in February.

Eurozone business activity grew at its slowest rate for over a year in March, according to the flash IHS Markit Eurozone PMI. At 55.3, down from 57.1 in February, the headline output index was the lowest since January of last year and signalled a second successive monthly easing in the rate of expansion. January's PMI had been the highest since June 2006.

Output growth moderated in both manufacturing and services, the latter seeing business activity grow at the slowest rate for five months while factory output increased at the weakest pace since January 2017.

The IHS Markit Flash Germany Composite Output Index, which is based on around 85% of usual monthly responses, registered a reading of 55.4 in March, down from 57.6 in February. Although remaining solid overall, growth has now softened in each of the past two months after having reached a near seven-year high in January.

Services business activity rose at the slowest pace since last August, while manufacturing output showed the weakest increase in 14 months. This slower expansion in factor output was reflected in a further correction in the IHS Markit Flash Germany Manufacturing PMI, which dipped from 60.6 in February to 58.4 in March, down for the third straight month and its lowest reading since July last year.

Private sector growth softened in March according to latest data. Nevertheless, at 56.2, down from 57.3 last month, the IHS Markit Flash France Composite Output Index continued to highlight an elevated rate of expansion and one that was markedly higher than the long-run series average.

Rates of expansion remained strong, but softened in both the manufacturing and service sectors, hitting 12- and seven-month lows respectively. Service providers maintained a sharper rate of growth than their goods producing counterparts.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2474 (4050)

$1.2439 (2184)

$1.2419 (905)

Price at time of writing this review: $1.2378

Support levels (open interest**, contracts):

$1.2307 (3416)

$1.2272 (5416)

$1.2232 (3876)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date April, 6 is 104140 contracts (according to data from March, 21) with the maximum number of contracts with strike price $1,2000 (6036);

GBP/USD

Resistance levels (open interest**, contracts)

$1.4285 (2795)

$1.4241 (2150)

$1.4213 (2515)

Price at time of writing this review: $1.4171

Support levels (open interest**, contracts):

$1.4073 (283)

$1.4043 (778)

$1.4009 (893)

Comments:

- Overall open interest on the CALL options with the expiration date April, 6 is 31158 contracts, with the maximum number of contracts with strike price $1,4200 (2795);

- Overall open interest on the PUT options with the expiration date April, 6 is 30057 contracts, with the maximum number of contracts with strike price $1,3800 (3596);

- The ratio of PUT/CALL was 0.96 versus 0.97 from the previous trading day according to data from March, 21

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Says renewed upward pressure on the swiss franc cannot be ruled out

-

Interventions occurred mainly during periods of uncertainty when the swiss franc was particularly sought after

Trend estimates (monthly change):

-

Employment increased 19,300 to 12,480,500.

-

Unemployment increased 4,300 to 729,500.

-

Unemployment rate remained steady at 5.5%.

-

Participation rate increased by 0.1 pts to 65.7%.

-

Monthly hours worked in all jobs decreased 1.4 million hours (0.1%) to 1,730.3 million hours.

Seasonally adjusted estimates (monthly change):

-

Employment increased 17,500 to 12,480,500. Full-time employment increased 64,900 to 8,533,600 and part-time employment decreased 47,400 to 3,946,900.

-

Unemployment increased 8,900 to 734,100. The number of unemployed persons looking for full-time work increased 13,600 to 512,900 and the number of unemployed persons only looking for part-time work decreased 4,700 to 221,200.

-

Unemployment rate increased by 0.1 pts to 5.6%

-

Participation rate increased by less than 0.1 pts to 65.7%.

-

Monthly hours worked in all jobs increased 21.2 million hours (1.2%) to 1,734.1 million hours.

-

Flash Japan Manufacturing PMI declines in March to 53.2, from 54.1 in February.

-

New orders increase, albeit to weakest extent in five months.

-

Job creation eases amid joint-softest pace of output growth since July 2017.

Commenting on the Japanese Manufacturing PMI survey data, Joe Hayes, Economist at IHS Markit, which compiles the survey, said: "The headline PMI declined in March, signalling a weaker improvement in overall business conditions in the manufacturing sector. Output, new order and employment growth rates all slowed, while longer lead times continued to impact supply capacities. "That said, with new business increasing for an eighteenth straight month, firms raised output prices to a quicker extent, signalling confidence in the demand climate and purchasing power of their clients. Despite two months of weaker headline PMI readings, the 2018 Q1 average still signals a robust operating environment."

-

Says only gradual upward pressure on inflation despite fall in unemployment

-

Balance sheet reduction program is proceeding smoothly, does not intend to alter

-

Today's decision to raise rates another step in gradual process

-

The shortfall of inflation reflects some unusual price declines from last year

-

Inflation may be above or below 2 percent at times

-

FOMC expects that the job market will remain strong

-

Raises view of estimated neutral Fed funds rate following years in which it lowered estimates

-

Job gains have been strong; growth rates of household spending and fixed investment have moderated

-

Economic activity has been rising at 'moderate rate;' previously described rate as 'solid'

-

Inflation on 12-month basis is expected to move up in coming months

-

Median projection sees Fed funds rate at 2.875 pct at end-2019 compared with 2.688 pct in dec forecast

European stocks ended modestly lower Wednesday, as investors prepared to hear that the Federal Reserve likely has decided to continue raising interest rates.

U.S. stock-market indexes ended a turbulent session slightly lower on Wednesday after the Federal Reserve delivered its sixth interest-rate increase since the end of 2015 and signaled it still expects to deliver two more before the end of the year. The central bank also upped its forecast for the number of rate increases it expects to deliver in 2019.

Asian stock markets outside mainland China strengthened Thursday, after the Federal Reserve raised interest rates but stopped short of signaling a faster pace of increases for this year.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers