- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 15-07-2011

The euro fluctuated against the dollar before as eight banks failed the European Union stress tests after regulators said they had a combined capital shortfall of 2.5 billion euros ($3.5 billion).

“They haven’t resolved the broader issues that have emerged and there will be question marks over the stress tests and the pressure on the euro in the near term is likely to downward more than up,” said Steven Englander, head of Group of 10 currency strategy at Citigroup Inc. in New York. “Investors are a lot more skeptical with these tests and there is going to be a lot of work to analysis the financials of the banks in the context that the market has moved way beyond what they were assuming in the stress test.”

The European banks were found to have insufficient reserves to maintain a core tier 1 capital ratio of 5 percent in the event of an economic slowdown, the European Banking Authority said.

The assessments are the first by the European Banking Authority since it was set up earlier this year. Last year’s tests by its predecessor were criticized for not being tough enough because banks were shown to need only 3.5 billion euros more capital, a 10th of the lowest analyst estimate. Banks that fail the stress test must present a plan to raise more capital within three months.

The U.S. currency strengthened earlier after a report showed U.S. consumer prices excluding food and energy increased for a second month, cutting chances of additional stimulus from the Federal Reserve. The Dollar Index had slumped earlier after Standard & Poor’s said there’s a 50 percent chance the U.S. will lose its top credit rating even if Congress reaches agreement on raising the debt ceiling to stave off a default.

The core measure of the cost of living in the U.S., which excludes more volatile food and energy costs, increased 0.3 percent for a second month. Economists projected the core gauge would rise 0.2 percent.

Federal Reserve Chairman Ben S. Bernanke told Congress yesterday that inflation has moved higher, boosting speculation the central bank won’t take further steps to support the U.S. economy.

“Having a slightly high reading of core inflation is something that grabbed the attention of the market today, which is our reason why the dollar should be benefiting after Bernanke’s speech that raised the idea that we could have more easing or the beginning of an exit,” said David Mann, regional head of research for the Americas at Standard Chartered Plc in New York.

The major market averages pushed higher following the results of the European stress tests. Currently, the Nasdaq is seeing a gain of 0.7% with the S&P and Dow trailing with respective gains of 0.3% and 0.1%.

European bank stocks are on the move following the results of the second round of European ‘stress tests.’ The tests showed 82 of 90 banks passed with a total of 20 banks seeing their Core Tier 1 Requirements below the 5% threshold for the two-year time horizon. Sixteen of the 90 banks will need to improve their capital buffers as their core Tier 1 Requirements are between 5% and 6%. The count shows five Spanish banks, two Greek banks, and one Austrian bank failing the test. Deutsche Bank (DB $52.57, -0.29) saw a spike immediately following the results, but has since pared those gains. Barclays (BCS $14.68, +0.12) is seeing a similar trading pattern play out in its shares.

While the broader market is flat, there are several individual stocks making big moves. Google (GOOG) is +12.0% after reporting strong earnings. Specifically, Google reported Q2 EPS of $8.74 per share, excluding non-recurring items, $0.91 better than the Capital IQ Consensus Estimate of $7.83; net revenues (subtracting traffic acquisition costs -- TAC) rose 36% YoY to $6.92 billion versus the $6.55 billion consensus.

Citigroup (C) is +0.9% after reporting EPS of $1.09 per share, vs. the Capital IQ Consensus Estimate of $0.96; revenues rose 4.5% year/year to $20.62 billion vs the $19.76 billion consensus; the call starts at 11:00 ET.

Petrohawk Energy (HK), is +62.7% on reports indicating that BHP Billiton (BHP) will acquire the company for $38.75/share, representing a 65% premium to yesterday's closing price. Petrohawk Energy is an oil and gas E&P name with exposure to the Haynesville Shale, the Eagle Ford Shale, and the Midland and Delaware Basins. These reports have caused related names to move sharply higher in early trade as market participants readjust valuations based on this potential takeout.

Clorox (CLX) is +6.8% after confirming that it has received an unsolicited conditional proposal from Icahn Enterprises to acquire the co for $76.50 per share, subject to due diligence, financing and other conditions. Clorox's board of directors, in consultation with its financial and legal advisers, will review the proposal in due course.

Stocks have erased the majority of their gains after a rather disappointing Consumer Sentiment Survey for July from the University of Michigan. The Sentiment Survey came in at 63.8, which is far worse than the reading of 71.4 that had been broadly expected. The July reading is also less than the 71.5 that had been posted for the prior month.

current conditions 76.3 vs 82.0 and expectations 55.8 vs 64.8. 1y inflation expected 3.4% and 5y at 2.8%.

S&P futures vs fair value: +4.30. Nasdaq futures vs fair value: +21.00. Equity futures edged higher to their best levels of the morning following the top and bottom line beats by Citigroup (C) before slipping on the data release. The banking giant posted earnings per share of $1.09 (Capital IQ Consensus Estimate of $0.96) and saw revenues climb to $20.62 billion (Capital IQ Consensus Estimate of $19.76 billion).

At 13:15 GMT US Industrial production will be released.

At 13:55 preliminary Michigan sentiment index is due to come.

EUR/USD

EUR/USD

Offers: $1.4200

Bids: $1.4095/90, $1.4080

GBP/USD

Offers: $1.6170/80, $1.6195/00

Bids: $1.6110/00

USD/JPY

Offers: Y79.25/30, Y79.35/40

Bids: Y78.90/80, Y78.75, Y78.50/40

AUD/USD

Offers: $1.0680/00

Bids: $1.0615/20

EUR/GBP

Bids: stg0.8745, stg0.8725/20, stg0.8695/90.

The dollar headed for its biggest weekly drop against the yen in three months after Standard & Poor’s became the second ratings company this week to say it may cut the U.S.’s top credit grade.

The euro strengthened as Italian lawmakers prepared for a confidence vote on an austerity package and before the release of stress tests on European banks.

The European Banking Authority will release the results of the stress tests for 91 banks as part of an effort to reassure investors the region’s banks have sufficient capital.

The greenback headed for a second weekly loss against the Swiss franc as S&P said there’s at least a 50% chance it will cut the AAA rating within 90 days if it concludes Congress and President Barack Obama’s administration haven’t achieved a credible solution to the rising government debt burden.

Moody’s Investors Service put the U.S. Aaa credit rating on review for a downgrade on July 13, citing concern officials won’t raise the nation’s $14.3 trillion debt limit in time to prevent a missed payment.

“Uncertainty about the credit rating and debt-ceiling talk will continue weighing on the dollar,” said Toshiya Yamauchi, a senior currency analyst at Ueda Harlow Ltd.. “The market has a negative view for the dollar.”

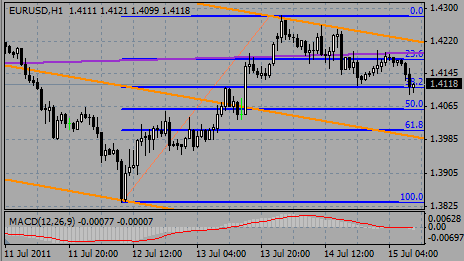

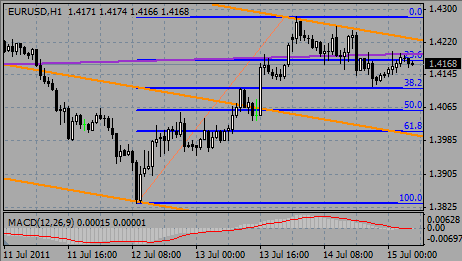

EUR/USD printed highs on $1.4190 before retreated to $1.4110.

GBP/USD retreated from $1.6170 to $1.6120.

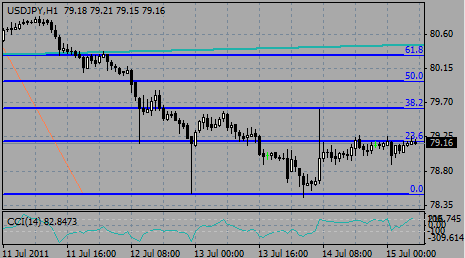

USD/JPY rose from Y78.90 to Y79.20.

Today's focus in Europe will be on EU Trade balance.

In US investors will digest US CPI for June at 12:30 GMT. The same time NY Fed Empire State manufacturing index comes.

At 13:15 GMT US Industrial production will be released.

At 13:55 preliminary Michigan sentiment index is due to come.

USD/JPY rises after printing daily high on Y79.28. Offers extending to Y79.40 with stops above Y79.60 ahead of offers Y79.80/00. rate currently holds around Y79.16.

AUD/USD falls after it broke the 55 day MA at $1.0657 and triggered bids at $1.0650 (the 50 day MA). Some technical support seen towards $1.0615/20 lows of Wednesday. Below support comes at 100 day moving average currently around $1.0516. Aussie trades around $1.0633.

Majors close

Nikkei -27.02 (-0.27%) 9936

Topix -3.65 (-0.42%) 856.88

DAX -53.13 (-0.73%) 7215

CAC -42.04 (-1.11%) 3751

FTSE-100 -59.48 (-1.01%) 5847

Dow -54.49 (-0.44%) 12437.12

Nasdaq -34.25 (-1.22%) 2763

S&P500 -8.85 (-0.67%) 1308.87

Oil +0.15 (+0.16%) $95.85

10-Years +0.05 2.94%

Japanese stocks fell for the third time this week as on Wednesday Moody's and Chinese ratings agency Dagong both put the US AAA credit rating on negative watch. This news plunged the dollar down against the yen and hurt an outlook for Asian exporters.

Japanese stocks also slipped today after Bernanke’s comments about a risk of a U.S. default and the impact of dollar weakness on exporters.

Toyota, the world’s largest automaker, lost 0.7 percent.

Nippon Yusen K.K., Japan’s biggest shipping line by sales, sang 1.7 percent after cargo rates dropped.

Dainippon Screen, a maker of equipment used to clean semiconductor wafers, slumped 4.2 percent to 645 yen, the lowest since Jan. 13.

As for gainers, among stocks that rose, smelter Toho Titanium Co. jumped by 1.7 percent to 2,336 yen after Mitsubishi UFJ Morgan Stanley Securities Co. upgraded stocks to “outperform” due to a “sharp recovery” in titanium demand.

China’s Shanghai Composite index gained 0.53 per cent to 2,994.

The Shanghai index was up 0.53% per cent at 2,944.

Japan’s Nikkei 225 Stock Average fell 0.27 per cent 9,936.

European stocks fell for the fourth day in five after Italy auctioned bonds and US AAA credit rating was put on negative watch. According to JPMorgan Chase & Co, even a temporary default will probably have “large systemic effects” on the economy and Treasury finances.

Italy sold five-year bonds at the highest yield in three years. The Treasury priced 1.25 billion euros ($1.8 billion) of 2016 bonds today at an average yield of 4.93 percent, up from a yield of 3.9 percent at a previous auction on June 14.

Prime Minister Silvio Berlusconi won a confidence vote in the Italian Senate on its four-year austerity plan, which aims to balance the budget by 2014. The Chamber of Deputies will pass the plan tomorrow.

Germany’s Landesbank Hessen-Thueringen snubbed the European Union’s bank stress tests, refusing to give the European Banking Authority permission to publish all of its data. The stress test results will be announced on Friday after the European stocks markets’ close.

Wednesday Greece's credit rating was cut three levels by Fitch Ratings from B+ to CCC, the lowest grade for any country in the world, saying about “real possibility” of default.

Petrofac Ltd. (PFC), the U.K.-based oilfield services and engineering provider, decreased 3.8 percent as it was downgraded to “underweight” from “equal weight” at Barclays.

Software AG sang 16 percent, its largest decline in more than two years, after posting a decline in sales.

SAP AG, the world’s biggest business-software maker, lost 2.8 percent.

Accor SA (AC) and Intercontinental Hotels Group Plc (IHG) fell 2.2 percent to 29.64 euros and 3.2 percent to 1,241 pence, respectively, after rival Marriott’s third-quarter earnings outlook was forecasted below forecasts.

Daily Mail & General Trust Plc (DMGO) shed 4.1 percent to 421.3 pence as its data in advertising sales declined 7 percent in the 13 weeks through July 3.

U.S. stocks fell Thursday, giving up early gains after Federal Reserve chairman Ben Bernanke said that the central bank may not be as willing to move on further stimulus as previously indicated.

Shares of Alcoa (AA, Fortune 500), DuPont (DD, Fortune 500) and Boeing (BA, Fortune 500) were the biggest drags on the blue chip index.

Meanwhile, JPMorgan (JPM, Fortune 500) was the best performer on the Dow, rising roughly 2%, after reporting quarterly income and revenue that topped estimates. But the bank also said that it sees additional costs for resolving mortgage issues.

Economy: The Labor Department said jobless claims fell 22,000 to 405,000 in the latest week. Economists were expecting weekly claims to decrease to 410,000.

The producer price index -- a reading of wholesale inflation -- fell 0.4% in June, after rising 0.2% the prior month. Economists were expecting the measure to have fallen 0.2%.

June retail sales rose 0.1%, according to the Commerce Department. Sales were expected to have fallen 0.2% last month.

Companies: ConocoPhillips (COP, Fortune 500) said it plans to split its operations into two distinct publicly traded corporations, sending its stock up 1.5%. In a tax-free spin to shareholders, ConocoPhillips will separate its oil refining and marketing business from its exploration and production operations.

The merger between NYSE Euronext (NYX, Fortune 500) and Deutsche Boerse moved one step closer to completion on Thursday after Deutsche shareholders gave preliminary approval of the merger. Shares of NYSE Euronext edged lower.

News Corp (NWSA, Fortune 500) shares dropped 3% following several reports that the FBI is opening up an investigation into whether its media properties may have hacked into 9/11 victims' voicemails.

European music-streaming service Spotify launched in the U.S. today, bringing shares of competitor Pandora (P) down 1%.

Marriott (MAR, Fortune 500) shares plunged more than 6.5%, after the company cut its full-year outlook.

EUR/USD: $1.4000, $1.4160, $1.4275, $1.4285

USD/JPY: Y78.25, Y79.00, Y79.50, Y80.00, Y80.50, Y80.80, Y81.00

EUR/JPY: Y115.00

GBP/USD: $1.5975, $1.5970

GBP/JPY: Y128.40

USD/CHF: Chf0.8275

AUD/USD: $1.0625, $1.0800

Thursday the U.S. dollar significantly dropped as late Wednesday Moody's and Chinese ratings agency Dagong both put the US AAA credit rating on negative watch.

“The fear of the U.S. downgrade has led to a swift move to the safe haven currency,” said Sebastien Galy, a foreign-exchange analyst at Societe Generale in London.

Euro strengthened versus US dollar amid the weakeness of the latter. Despite Greece's credit rating was cut three levels by Fitch Ratings from B+ to CCC, any downgrade in the eurozone has increasingly less impact than debt problems in the US.

It should be noted that yesterday Federal Reserve chairman Ben Bernanke, raised the possibility of a third bout of quantitative easing – or “QE3”, that the central bank is ready to provide additional economic stimulus if needed.

The Swiss franc reached to record highs against the dollar, euro and the pound amid concerns about credit ratings of U.S and Greece. Today Fitch Ratings has affirmed Switzerland's ratings at 'AAA'. Its outlook remains stable.

New Zealand’s dollar strengthened to a record after a government report showed the economy grew faster than expected. The New Zealand economy has released today its house price index for the month of June which increased 1.3%, compared with a previous drop by 1.8% in May. This fact signaled the nation is recovering from a deadly earthquake in February.

EUR/USD printed highs on $1.4280 before retreated to $1.4150. After some consolidation rate set stable around $1.4110.

GBP/USD rose from $1.6185 before held within the $1.6090/$1.6150 range.

USD/JPY rose from Y78.45 to Y79.60. But rate failed to set above and retreated to Y78.90/00.

Today's focus in Europe will be on EU Trade balance.

In US investors will digest US CPI for June at 12:30 GMT. The same time NY Fed Empire State manufacturing index comes.

At 13:15 GMT US Industrial production will be released.

At 13:55 preliminary Michigan sentiment index is due to come.

Nikkei -27.02 (-0.27%) 9936

Topix -3.65 (-0.42%) 856.88

DAX -53.13 (-0.73%) 7215

CAC -42.04 (-1.11%) 3751

FTSE-100 -59.48 (-1.01%) 5847

Dow -54.49 (-0.44%) 12437.12

Nasdaq -34.25 (-1.22%) 2763

S&P500 -8.85 (-0.67%) 1308.87

Oil +0.15 (+0.16%) $95.85

10-Years +0.05 2.94%

Resistance 3: Y80.20

Resistance 1: Y79.60

Current price: Y79.16

Support 1:Y78.50

Support 3:Y77.10

Current price: Chf0.8164

Support 1: Chf0.8085

Support 2: Chf0.8050

Support 3: Chf0.8000

Comments: Dollar holds within the narrow range with support comes at Chf0.8085 (session low). Below losses may widen to Chf0.8050. Resistance is around Chf0.8250 (38.2% Fibo of Chf.0.8520 - Chf0.8080). Above resistance comes at Chf0.8330 (Jul 13 high).

Comments: Techs hasn't changed much with strong support comes at $1.6100/90 (23.6% Fibo of $1.5778 - $1.6190). Break under widens correction to $1.6000/90 (50%). Below support is near $1.5910 (local lows of Jul 12-13). Resistance is around $1.6190 (overnight high). Above there is a room for a rise up to $1.6240 (channel line from May 02).

Resistance 2:$1.4370

Resistance 1:$1.4230

Support 3: $1.3950

Comments: Rate continues to retreat, heading for support at $1.4110 (38.2% Fibo of $1.3840-$1.4280). Stronger level at $1.4060 (50%), with further losses may widen to $1.3950 (Jul 13 lows). Resistance is around channel line from Jul 05 at $1.4230. Above the recover may extend to $1.4370 (Jul 07-08 high).

09:00 EU(17) Trade balance (May) unadjusted, bln - -4.1

09:00 EU(17) Trade balance (May) adjusted, bln -3.1 -2.9

12:30 USA CPI (June) -0.1% 0.2%

12:30 USA CPI (June) Y/Y - 3.6%

12:30 USA CPI excluding food and energy (June) 0.2% 0.3%

12:30 USA CPI excluding food and energy (June) Y/Y - 1.5%

12:30 USA NY Fed Empire State manufacturing index (July) 0.6 -7.8

13:15 USA Industrial production (June) 0.2% 0.1%

13:15 USA Capacity utilisation (June) 76.9 76.7

13:55 USA Michigan sentiment index (July) preliminary 71.0 71.5

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers