- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 11-08-2011

Carl Weinberg of High Frequency Economics notes that France's Q2 GDP reading will be out ahead of overall EMU GDP data (August 16/Assumption Day holiday Aug 15).

HFE looks for the report to show a 0.3% decline in Q2, compared to most estimates looking for +0.3% instead (vs +0.9% q/q in Q1 and +1.4% y/y in 2011).

A -0.3% reading would bring GDP growth "down to a 1.4% y/y pace, compared to 2.2% in Q1, and leave economic activity 1.1% lower than its pre-downturn peak in the first quarter of 2008," he said.

The market may be "vulnerable to unexpected bad news about France," Weinberg says.

Despite ongoing concern about the solvency of French bank Societe Generale, France's second-largest bank, the markets continue rising amid positive news about corporate earnings of such large companies as Cisco Systems (CSCO) and decline in jobless claims by 7K to 395K in the week ended on Aug 6.

Fri's July retail sales data "could be the last month of strength before the restriction from tightening financial conditions bites domestic demand. The story could be the same for jobless claims - decent readings now, but possibly very weak readings later".

The euro falls against the dollar amid resumed concern that Europe will fail to contain its sovereign-debt crisis.Earlier the euro soared in the wake of news that Italy and France will announce a naked short-selling ban after the close Thursday.

The Swiss franc continue falling after Swiss National Bank Deputy President Thomas Jordan was reported today to have said in an interview with Tages-Anzeiger that a temporary tie between the franc and the euro to curb the Swiss currency’s gains would be legal under the central bank’s mandate.

The pound strengthened against the dollar after U.K. Chancellor of the Exchequer George Osborne rebuffed opposition demands to review spending cuts as the euro- region’s debt woes roil stock markets around the world.

The yen sheds as higher Treasury yields make the dollar more attractive to Japanese investors.

The Australian dollar bounces back versus the dollar amid weakness of the latter. Earlier the Australian currency fell versus its New Zealand counterpart after a report showed the jobless rate unexpectedly rose.

Золото стремительно снижается после того, как биржевой оператор CME Group Inc, который владеет основными американскими биржами металлов, зерна и энергии, включая Nymex, поднял маржинальные требовании на торговлю золотом, побуждая инвесторов к продажам. CME Group поднял маржу на фьючерсы на золото на 22%.

Также спрос на фьючерсы снижает рост на фондовых рынках США.

После 3-дневного ралли фьючерсы показали самое крупное падение за последние 7 недель.

На данный момент декабрьские фьючерсы на золото котируются по $1,743 за тройскую унцию (-2.31%).

The gold prices plummets down as CME Group Inc., which owns the main U.S. exchanges for metals, grains and energy including the Nymex, raised margin requirements for trading in gold, prompting investors unwilling or unable to put up more money to sell. The exchange operator raised margins on gold contracts by 22 percent.

Gold futures fell the most in seven weeks after their three-day rally to a record topping $1,800 an ounce.

Rebound in US stock markets also put pressure on gold demand.

Currently December gold futures are at $1,743 per troy ounce (-2.31%).

Jens Nordvig of Nomura pointed to the latest available weekly Fed data, which shows that the USD cash position of foreign banks was $837bn as per July 27 (vs $900bn as per July 13), compared to an average $394bn in 2010 and a mere $54bn in 2007.

"Since European banks dominate the foreign banks operating in the US, the bulk of this cash is sitting on eurozone bank balance sheets," he says. This would suggest that eurozone banks "have a significant buffer in place and that difficulty in obtaining new USD funding is not translating into immediate stress," Nordvig says.

Also, this explains why FX swap line are not yet being tapped and why the euro has been less correlated with the FX basis swap market, as was the case in 2008, he says.FX swap line are not yet being tapped and why the euro has been less correlated with the FX basis swap market, as was the case in 2008, he says.

The markets continue soaring. Dow index have already added more than 360 points.

The markets continue rising amid positive news about corporate earnings of such large companies as Cisco Systems (CSCO) and decline in jobless claims by 7K to 395K in the week ended on Aug 6.

EIA estimates OPEC revenues collectively will break above $1 trillion this year and in 2012, even as oil prices currently decline to $80/bbl.

Stocks have begun to pull back from a strong upward push that came with the open, but the broad market continues to boast a gain of more than 1%.

To little surprise, financials are leading the action. The sector has been a driving force behind broad market action all week. Today, the sector is up 1.8%, which makes it the top performing sector.

Tech stocks aren't far behind, however. The sector's 1.6% gain has been helped along by a positive response to the latest quarterly report from Dow component Cisco (CSCO 15.64, +1.91)

Stocks were poised for a higher start earlier, as investors pinned their hopes on an upbeat forecast from Cisco Systems. But as the clock ticked closer to the opening bell, futures turned lower, following a downturn in European stocks.

The swing to the red came, as European stocks drifted into negative territory and fell to session lows, amid ongoing jitters about the region's debt crisis.

Ever since Standard & Poor's stripped the United States of its AAA credit rating last week, fears have been building that rating agencies may also downgrade AAA-rated nations in Europe, since they are also struggling with massive debt problems.

Concerns about the solvency of French bank Societe Generale, or SocGen, are also weighing on markets, despite the bank's denial of the allegations.

Earlier, investors were showing optimism about Cisco's better-than-expected guidance for the current quarter. Shares of Cisco (CSCO, Fortune 500) jumped nearly 12% in premarket trading.

Jobless claims were also better than forecast, falling below the key 400,000 level for the first time in four months.

World markets:

Economy: A report from the Labor Department showed that weekly jobless claims fell to 395,00 last week, down 7,000 from the prior week.

That reading was better than the 409,000 claims economists were expecting.

The U.S. trade deficit grew to $53.1 billion in June, from $50.8 billion in May. The trade deficit was also wider than the $48 billion expected.

Companies: Companies reporting on Thursday include chip maker Nvidia (NVDA), and retailers Kohl's (KSS, Fortune 500) and Nordstrom (JWN, Fortune 500).

Gold futures for December delivery rose $5.30 to $1,789.60 an ounce, after setting an intraday record high of $1,817.60 an ounce.

Oil for September delivery slipped 24 cents to $82.65 a barrel.

Bonds: The price on the benchmark 10-year U.S. Treasury fell, pushing the yield up to 2.20% from 2.14% late Wednesday.

The cross pulled lower by ongoing general euro slippage, with cable currently buoyed above $1.6130. The cross extends its pullback off European morning highs of stg0.8825 to stg0.8740. Support seen at stg0.8725/15 (76.4% stg0.8678/0.8849) ahead of stg0.8700.

oil prices and a decline in exports. US data continues at 2030GMT with M2 Money Supply.

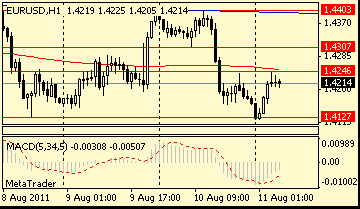

EUR/USD

Offers: $1.4225/30, $1.4245/50, $1.4280, $1.4295/300, $1.4310/15

Bids: $1.4155/50, $1.4105/00, $1.4080/70, $1.4055/50, $1.4015/00

Intesa Sanpaolo, Unicredit and Mediobanca shares are suspended from trading due to excessive volatility. Traders also note story doing the rounds that BNP Paribas faces another E713mln write-downs related to its Greek debt exposure.

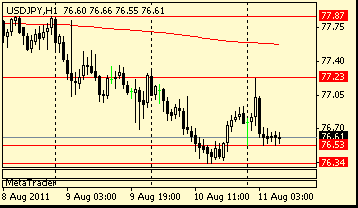

Cross trades in a tight Y108.30-Y109.25 range, looking at euro-dollar for the next move. Reported bids seen at Y108.65/60 and Y108.30/25 (10 Aug low). Topside offers noted at Y109.70/80 ahead of the 5-DMA at Y110.14 and offers at Y110.30/40.

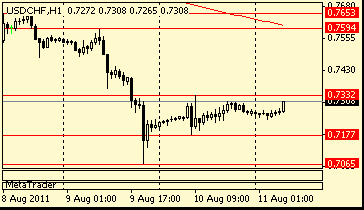

Under pressure in recent trade, tracking euro-dollar slippage to hit a fresh session low $1.0210. Inital support seen at $1.0210/00 ahead of $1.0120/10. Offers on approach to $1.0290.

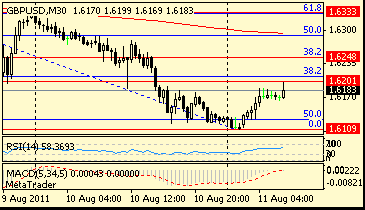

Drops back to $1.6120 from around $1.6185 as stops get triggered on break below $1.6150. Cable support remains at $1.6110, overnight low as well as Jul 11 low, with bids seen from here and extending to $1.6100. Break lower will target $1.6070. Offers remain on approach to $1.6185/00.

European stocks surged early on Thursday in a tentative rally, as reassuring comments from Societe Generale's CEO and France's renewed effort to trim its deficit eased fears over the euro zone debt crisis for now.

EUR/USD $1.4200, $1.4250, $1.4300

USD/JPY Y76.00( large), Y77.00, Y77.10, Y77.60, Y77.75

EUR/JPY Y109.00, Y111.20, Y114.00

GBP/USD $1.6325, $1.6335, $1.6450

AUD/USD $1.0000, $1.0300, $1.0335, $1.0435, $1.0520

NZD/USD $0.8200, $0.8085

oil prices and a decline in exports. US data continues at 2030GMT with M2 Money Supply.

oil prices and a decline in exports. US data continues at 2030GMT with M2 Money Supply.

Shanghai Composite 2,582 +32.33 +1.27%

2011 EMU HICP seen +2.6% vs 2.5% previous

2012 EMU HICP seen +2.0% vs 1.9% prev

2011 EMU GDP seen +1.9% vs 1.7% previous

2012 EMU GDP seen +1.6% vs 1.7% previous

2011 EMU unemployment seen 9.8% vs 9.8% prev

2012 EMU unemployment seen 9.5% vs 9.5% prev

Resistance 3: Y78.45 (Aug 8 high)

Resistance 3: Chf0.7650 (Aug 8 high)

Resistance 3: $ 1.6330 (Aug 10 high, 61.8 % FIBO $1.6470-$ 1.6110)

Resistance 3 : $1.4400 (Aug 8-9 high)

Topix +6.34 (+0.82%) 776.73

Hang Seng +452.97 (+2.34%) 19,783.70

DAX -303.66 (-5.13%) 5,613.42

CAC -173.20 (-5.45%) 3,002.99

FTSE-100 -157.76 (-3.05%) 5,007.16

Dow -519.83 (-4.62%) 10,719.90

Nasdaq -101.47 (-4.09%) 2,381.05

S&P500 -51.77 (-4.42%) 1,120.76

10-Years 2.11% -0.14

Oil +2.70 (+3.41%) 82.03

Gold +53 (+3.04%) 1,796

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers