- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 10-08-2011

Most S&P industry groups are in the red.

As en exception to the fall, Basic Materials gained in the wake of rising oil prices as U.S. Energy Department reported that the crude oil inventories fell by 5.23M barrels to 349.8M in the week ended Aug. 5, while analysts expected a rise by 1.35M barrels.

Financial sector (-2.2%) and Conglomerates (-2.7) were hit the hardest. Finacial group tumbled as investors worried that problems in the European banking sector could spillover into the U.S. banks.

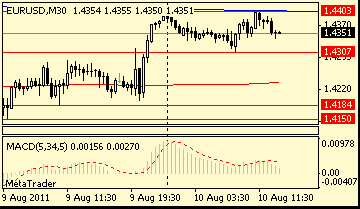

The euro rebounded to $1.4240 amid strong data on US Federal budget -$129.4b (slightly better than expected -140.3b. June figure was a fall by 40.0B), but currently retreats to $1.4210. Initial support is at $1.4250. Minor resistance is aroung $1.4150/60 area.

The markets are supported by strong data on US Federal budget -$129.4b (slightly better than expected -140.3b).

Earlier the stocks erased some losses after BofA chief Moynihan said that conditions at the bank and and in the country are much better than they were four years ago, when the financial crisis hit, during a call hosted by investor Bruce Berkowitz of Fairholme Capital Management.

But investors are still worried about the Europe's ongoing sovereign debt crisis.

The dollar gains against most major peers. Results of FOMC Fed meeting failed to convince investors global growth will be sustained.

Yesterday the FOMC redefined "extended period" as "at least through mid-2013" left its rates unchanged (0% -0.25%). The Fed also noted that inflation is moderated and will settle lower, but "downside risks to the economic outlook have increased." Fed expects slower pace ahead than in June.

The euro tumbles versus the dollar in the wake of concern that Europe will fail to contain its sovereign-debt crisis. The pair declined amid speculation that France Europe's second largest economy after Germany may be first to face a rating cut even though the major rating agencies have reiterated France's AAA rating.

The yen drops against the dollar. Earlier the currency gained, approaching a post- World War II high versus the dollar, as the Federal Open Market Committee’s pledge to keep interest rates at a record low until mid-2013 failed to convince investors growth will be buoyed. Central Bank of Japan is also ready to intervene to prevent the growth of currency as the latter hurts its export- aimed economy.

The Swiss franc weakens versus the greenback after the Swiss National Bank said it will “significantly increase” the supply of liquidity to the money market and expand banks’ sight deposits to fight the currency’s “massive overvaluation.”

The Canadian dollar sheds on concern that U.S., Canada’s biggest trade partner, growth is flat-lining. Declining oil prices also put pressure on the currency. Oil didn’t soared despite the U.S. Energy Department reported the oil inventories fell by 5.23 million barrels to 349.8 million in the week ended Aug. 5, while analysts expected a rise by 1.35M barrels.

Crude oil rebounded, but didn't reached its session highs despite U.S. Energy Department' data.

According to the report, the crude oil fell by 5.23M barrels to 349.8M in the week ended Aug. 5, while analysts expected a rise by 1.35M barrels.

Oil prices are still under pressure of concern that Europe will fail to contain its sovereign-debt crisis and that the global economic recovery is faltering.

Currently Crude for September delivery at $81.17 per barrel (+2.24%).

The euro is still under pressure of concern that Europe will fail to contain its sovereign-debt crisis and currently is at $1.4180.

The pair declines amid speculation that France Europe's second largest economy after Germany may be first to face a rating cut even though the major rating agencies have reiterated France's AAA rating.

Minor support is at $1. 4150/60, initial resistance is at $1.4250.

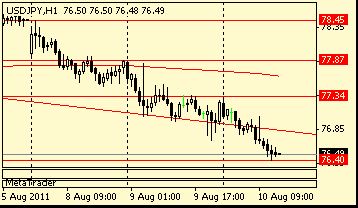

Currently the pair is at Y76.40. Bids seen at life lows at Y76.25, more at Y76.00 where a barrier is cited, with stops noted below there.

The markets are still on a dark mood on concerns over slowdown in economic recovery of US and EU debt crisis.

Spot gold posts new record highs of $1796.86/oz, slips quickly to current levels of $1785.75. Eye on $1800 market target.

Financial stocks led the sell-off in U.S markets, as investors worried that problems in the European banking sector could spillover into the U.S. banks.

European stock markets declines amid speculation that France, Europe's second largest economy after Germany, may be first to face a rating cut.

Even though the major rating agencies have reiterated France's AAA rating, "there's growing concern that France could get downgraded," said Tom Schrader, managing director at Stifel Nicolaus. "There's fear that S&P might do something stupid."

Despite yesterday's positive reaction of the markets, the statement of the Fed didn’t calm nervous markets as investors speculated the rebound was unjustified amid concerns that the economy is slowing.

EUR/USD $1.4200, $1.4225, $1.4350, $1.4365

USD/JPY Y76.00, Y77.75, Y78.00, Y78.25

EUR/JPY Y110.00

GBP/JPY Y125.00

EUR/CHF Chf1.0650

AUD/USD $1.0100, $1.0300

NZD/USD $0.8155

The yen strengthened as the Federal Reserve’s pledge to keep interest rates at a record low for two more years failed to convince investors global growth will be sustained, boosting demand for haven currencies.

The Swiss franc weakened after the nation’s central bank said it expanded measures to counter the currency’s strength.

US data starts at at 1400GMT with Wholesale Inventories and then at 1430GMT with the weekly EIA Crude Oil Stocks data. Later on, at 1800GMT, the US Treasury is expected to post a $135.0 billion budget gap in July, smaller than the $165.0 billion gap in July 2010.

Oil rebounded from a 10-month low as investors bet fuel demand will increase amid shrinking stockpiles and comments by the Federal Reserve that it is prepared to use a range of methods to bolster the economy.Currently crude oil for September delivery at $82.56 a barrel (+4.21%).

- have to face up to fact crisis is one of solvency;

- see no reason for MPC to commit on rate outlook;

- not particularly sensible to lock in low rates;

- monetary policy must have flexibility to move if needed;

- current UK plan has a lot of flexibility;

- inflation should fall quite sharply during next year;

- growth of money and credit at extraordinary low level;

- rates will need to rise at some point;

- growth profile weaker than in May;

- MPC judges growth risks are on the downside;

- near term UK growth prospects somewhat weaker.

The euro gained against the US dollar as investors bet the Federal Open Market Committee will repeat its pledge to maintain stimulus measures to revive confidence in the U.S. economy. Another catalyst to rise was the fact that the European Central Bank today purchased Italian and Spanish debt in an attempt to curb the nation’s surging borrowing costs and prevent the crisis spreading further.

The pound slumped versus the greenback amid the worst civil unrest in 30 years spread in the country and weaken-than-expected U.K. manufacturing unexpectedly. According the UK National Statistics, the UK industrial production didn't advanced in June, while analysts forecasted gaining by 0.4% after its previous rise by 0.9%.

The Swiss franc appreciated to fresh historical high against the dollar as investors favored the safest assets amid concern global growth is faltering. Earlier the franc slightly dropped amid weaken-than-expected July consumer confidence.

The yen also gained versus the dollar as “save haven” currency. The Japanese currency has almost erased its decline since the nation’s unilateral intervention on The Bank of Japan added 10 trillion yen ($129 billion) of monetary stimulus on Aug. 4.

The Canadian dollar rose for the first time in eight days against its US rival as an advance in North American stocks reduced demand for a refuge in the greenback. Rising oil prices also supported the loonie.

European events start at 0600GMT with the final reading of German HICP, which is followed by France data at 0645GMT, which includes the June readings for balance of payments and industrial output data. The IEA monthly oil market report then follows, at 0800GMT.

UK data starts at 0930GMT with the Bank of England's Quarterly Inflation Report. The August Inflation Report is set to show inflation, at least in the near term, higher and growth lower than predicted back in May, while BOE Governor Mervyn King will leave all policy options open at the press conference. The BOE's central forecasts are based on market rate expectations. The fact the market has stopped pricing in rate hikes this year or next will inevitably push up on the market rate inflation forecast.

US data starts at at 1400GMT with Wholesale Inventories and then at 1430GMT with the weekly EIA Crude Oil Stocks data. Later on, at 1800GMT, the US Treasury is expected to post a $135.0 billion budget gap in July, smaller than the $165.0 billion gap in July 2010.

06:00 Germany CPI (July) final 0.4% 0.4% 0.1%

06:00 Germany CPI (July) final Y/Y 2.4% 2.4% 2.3%

06:00 Germany HICP (July) final Y/Y 2.6% 2.6% 2.4%

06:45 France Industrial production (June) -1.6% 0.5% 1.9 (2.0)%

The dollar rose against the majority of its major counterparts as the Federal Reserve’s pledge for record low interest rates failed to convince investors global growth will be sustained, boosting demand for haven currencies.

The Swiss franc weakened after the nation’s central bank said it expanded measures to counter the currency’s strength.

Japan’s Finance Minister Yoshihiko Noda said in parliament today that one-sided moves in the yen can hurt growth.

Japan is “very serious about preventing yen strength,” said Kurt Magnus, executive director of currency sales at Nomura Holdings Inc. in Sydney.

The euro slipped as a French report showed industrial production fell more than economists estimated in June.

UK data starts at 0930GMT with the Bank of England's Quarterly Inflation Report. The August Inflation Report is set to show inflation, at least in the near term, higher and growth lower than predicted back in May, while BOE Governor Mervyn King will leave all policy options open at the press conference. The BOE's central forecasts are based on market rate expectations. The fact the market has stopped pricing in rate hikes this year or next will inevitably push up on the market rate inflation forecast.

US data starts at at 1400GMT with Wholesale Inventories and then at 1430GMT with the weekly EIA Crude Oil Stocks data. Later on, at 1800GMT, the US Treasury is expected to post a $135.0 billion budget gap in July, smaller than the $165.0 billion gap in July 2010.

EUR/USD $1.4200, $1.4225, $1.4350, $1.4365

USD/JPY Y76.00, Y77.75, Y78.00, Y78.25

EUR/JPY Y110.00

GBP/JPY Y125.00

EUR/CHF Chf1.0650

AUD/USD $1.0100, $1.0300

NZD/USD $0.8155

Nikkei -153.08 (-1.68%) 8,944.48

Topix -12.47 (-1.59%) 770.39

Hang Seng -1,159.87 (-5.66%) 19,330.70

DAX -6.19 (-0.10%) -5,917.08

CAC 51.00 (1.63%) 3,176.19

FTSE-100 +95.97 (1.89%) 5,164.92

Dow +429.92 (3.98%) 11,239.80

Nasdaq +124.83 (5.29%) 2,482.52

S&P500 +53.07 (4.74%) 1,172.53

10-Years 2.28% -0.04

Oil 0.430 (0.53%) 81.740

Gold 27.20 (1.59%) 1,740.40

Asian markets closed Tuesday mostly lower

Japan’s Nikkei Stock Average closed down 1.7% at 8,944.48, South Korea’s Kospi ended at 1,801.35, taking a hit of 3.6%, and Taiwan’s Taiex slid 0.8% to 7,493.12.

All three benchmarks ended well off their lows — Seoul shares had in particular dropped as much as 10% earlier in the day, before sharply narrowing losses. The Kospi has now lost between 2% and 4% for six straight sessions.

Australia’s S&P/ASX 200 index staged a major turnaround from a more than 5% drop to end the day up 1.2% higher at 4,034.8.

China’s July CPI reached a higher-than-expected 6.5%, accelerating from a 6.4% year-on-year rise in June.

The Shanghai Composite ended fractionally lower at 2526.07. The index came off lows even as the country's consumer price index rose to a higher-than-expected 6.5% in July from a year earlier and above the 6.4% rate in June. But market participants said they don't expect Beijing to launch further tightening measures given the tumultuous global markets.

Japan’s Inpex Corp. fell 5.5% in Tokyo. In Hong Kong, Cnooc Ltd. lost 8.2% of its value, while stock in Angang Steel Co. plunged 12.7%.

Korean exporters were among those hit hard by heavy foreign selling, with LG Electronics losing 8.1% and Hyundai Motor shrinking 2.8%.

In Hong Kong, HSBC Holdings Ltd. fell 7.3%, Standard Chartered PLC dropped 5.6% and Bank of China Ltd. lost 7.2%.

In Tokyo, Nomura Holdings Inc. skidded 3.8% and Mitsubishi UFJ Financial Group Inc. traded down 2.4%.

European markets ended the day in green zone

The markets started trading on a dark mood on concerns over slowdown in economic recovery of US and Europe for all this week.

The main catalyst to rise was the fact that the European Central Bank today purchased Italian and Spanish debt in an attempt to curb the nation’s surging borrowing costs and prevent the crisis spreading further.

Then the markets gained as investors bet the Federal Open Market Committee will repeat its pledge to maintain stimulus measures to revive confidence in the U.S. economy.

Among big decliners in London, Royal Bank of Scotland Group PLC fell 3.9%. Silver miner Fresnillo PLC slumped 7.3%, tracking a drop in silver prices.

Shares of RWE AG sank 6.3% after the utility firm said first-half net profit fell 22% and slashed its earnings forecast, citing pressure from Germany’s decision to close its nuclear reactors. In the same sector, E.On AG fell 5.9%, intensifying pressure on the DAX.

Also in Germany, Deutsche Telecom AG fell 3.5% and Deutsche Bank AG dropped 2.9%.

Notable gainers included car maker BMW AG, up 6.3%, and telecom-equipment firm Alcatel-Lucent, up 9.2%.

US stocks bounded back between 4% and 5%

The Dow Jones industrial average soared by 430 points. This is the first bulls since US credit downgrade by agency S&P.

The stocks popped higher on the defined "extended period" language. FOMC redefined "extended period" as "at least through mid-2013" left its rates unchanged (0% -0.25%). The Fed also noted that inflation is moderated and will settle lower, but "downside risks to the economic outlook have increased."

Economy: Fed interest rates were remained unchanged (0% -0.25%)

Corporate news: Financial and Technology sectors significantly rebounded after Monday’s decline.

The Bank of America's (BAC) stock recouped some of those losses Tuesday, with shares up 17%. Financial stocks such as JPMorgan Chase (JPM) andAmerican Express (AXP) rebounded 7%, and Citigroup (C) soared more than 14%.

Boeing (BA), Alcoa (AA) and Pfizer (PFE) were among the biggest gainers on Tuesday and all rose more than 2%. Losers included Cisco (CSCO) and General Electric (GE), which both fell more than 2%.

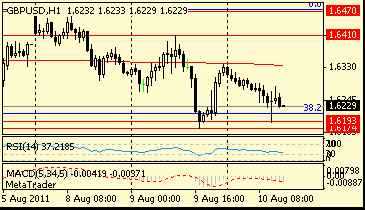

Support 2 : $1.6130 (50.0 % FIBO $1.5780-$ 1.6470)

Comments: the pair eased under $1.6300. The immediate resistance - $1.6340. Above growth is possible to $1.6380. The immediate support - $1.6220. Below decrease is possible to $1.6175.

Comments: the pair eaded from yesterday's high. The immediate support - $1.4200. Below losses are possible to $1.4150. The immediate resistance - $1.4400. Above growth is possible to $1.4450.

Nikkei -153.08 (-1.68%) 8,944.48

Topix -12.47 (-1.59%) 770.39

Hang Seng -1,159.87 (-5.66%) 19,330.70

DAX -6.19 (-0.10%) -5,917.08

CAC 51.00 (1.63%) 3,176.19

FTSE-100 +95.97 (1.89%) 5,164.92

Dow +429.92 (3.98%) 11,239.80

Nasdaq +124.83 (5.29%) 2,482.52

S&P500 +53.07 (4.74%) 1,172.53

10-Years 2.28% -0.04

Oil 0.430 (0.53%) 81.740

Gold 27.20 (1.59%) 1,740.40

06:00 Germany CPI (July) final 0.4% 0.1%

06:00 Germany CPI (July) final Y/Y 2.4% 2.3%

06:00 Germany HICP (July) final Y/Y 2.6% 2.4%

06:45 France Industrial production (June) 0.5% 2.0%

06:45 France Industrial production (June) Y/Y 5.4% 2.9%

09:30 UK BoE quarterly inflation report

14:00 USA Wholesale inventories (June) 1.0% 1.8%

19:00 USA Federal budget (July), bln -140.0 -43.1

23:50 Japan Machinery orders core (June) adjusted 1.8% 3.0%

23:50 Japan Machinery orders core (June) unadjusted Y/Y 11.3% 10.5%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers