- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 09-08-2011

Stocks pop higher on the defined "extended period" language. FOMC redefined "extended period" as "at least through mid-2013" left its rates unchanged (0% -0.25%).

- FOMC redefined "extended period" as "at least through mid-2013".

- Fed interest rates were remained unchanged (0% -0.25%).

- "Is prepared to employ tools (to promote a stronger recovery) as appropriate."

- Fed expects slower pace ahead than in June.

- Infl moderated, will settle lower.

- "Downside risks to the econ outlook have increased."

The euro gained against the US dollar as investors bet the Federal Open Market Committee will repeat its pledge to maintain stimulus measures to revive confidence in the U.S. economy. Another catalyst to rise was the fact that the European Central Bank today purchased Italian and Spanish debt in an attempt to curb the nation’s surging borrowing costs and prevent the crisis spreading further.

The pound slumped versus the greenback amid the worst civil unrest in 30 years spread in the country and weaken-than-expected U.K. manufacturing unexpectedly. According the UK National Statistics, the UK industrial production didn't advanced in June, while analysts forecasted gaining by 0.4% after its previous rise by 0.9%.

The Swiss franc appreciated to fresh historical high against the dollar as investors favored the safest assets amid concern global growth is faltering. Earlier the franc slightly dropped amid weaken-than-expected July consumer confidence.

The yen also gained versus the dollar as “save haven” currency. The Japanese currency has almost erased its decline since the nation’s unilateral intervention on The Bank of Japan added 10 trillion yen ($129 billion) of monetary stimulus on Aug. 4.

The Canadian dollar rose for the first time in eight days against its US rival as an advance in North American stocks reduced demand for a refuge in the greenback. Rising oil prices also supported the loonie.

The major US equities are around session highs. The Nasdaq Composite currently boasts the biggest move by percent (+3.56%).

The Nasdaq's surge as large-cap tech plays like Apple (AAPL +4.4%) and Google (GOOG +3.8%) surge after enduring a sharp drop in the prior session. Technolody sector added 1.2%.

Semiconductor-related plays are up, but lagging on a relative basis, however. In turn, the Semiconductor HOLDRs ETF (SMH) is up less than 2%.

The markets hold in the green zone ahead of today's meeting of the Federal Open Market Committee.

September WTI crude oil renewed its fall and currently at $81.85 per barrel (+0.66%), after trading in a $75.71 to $83.05 range. Earlier the bulls were supported on waiting of Federal Reserve’ statement on monetary policy that may hint a further easing. At the low seen overnight, WTI was down $24.91 from the $100.62 peak seen only two weeks ago.

Stocks opened today's trade with impressive gains, but the move was quickly challenged by traders looking to sell the bounce. Pressure actually pushed the Dow to a fractional loss in negative territory before it was able to rebound alongside its counterparts.

Financials, which plummeted 10% in the prior session, have actually provided some support to the broad market this morning. The sector's 2.0% bounce comes as bargain hunters offer a bid for banks and diversified financial services plays after their beat down yesterday.

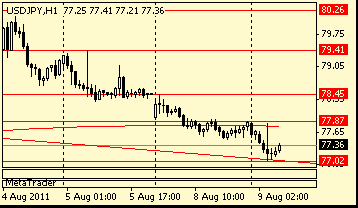

Rate trades in mid-range around Y77.20 ahead of the Y77.00 and Y77.50 option expiries. Bids at Y77.10/05 and Y77.00/95, offers seen at Y77.50/60.60.

U.S. stocks appeared set for a choppy session Tuesday, following the market's worst day since the 2008 financial crisis, as investors awaited the Federal Reserve's latest statement on monetary policy.

U.S. stocks have fallen 15% during the past two weeks, and Monday's beating was the most brutal thus far. Stocks posted their worst losses since the 2008 financial crisis -- amounting to a paper loss of about $1 trillion, in the aftermath of S&P's downgrade of the U.S. credit rating.

All three major indexes sank between 5% and 7%, pushing the Dow below 11,000 for the first time since last November. The sell-off was worse than the 512-point drop stocks experienced only three trading sessions before.

Bank stocks were among the hardest hit during Monday's slide -- with Bank of America shares tumbling 20%, after AIG (AIG, Fortune 500) said it is suing the bank for billions of dollars over mortgage security fraud.

But Bank of America's (BAC, Fortune 500) stock was poised to recoup some of those losses, with shares up more than 6% in premarket trading Tuesday.

All eyes will be on the Federal Reserve when it releases its monetary policy statement at 1815 GMT on Tuesday. Investors will likely pour over the central bank's announcement for hints that the Fed will take steps to stabilize markets, and revitalize the slowing economic recovery to avoid a double-dip recession.

Companies: After the closing bell, Dow component Walt Disney (DIS, Fortune 500) will head to the earnings stage. The media giant is expected to report a profit of 73 cents a share.

World markets:

Oil for September delivery rose 80 cents to $82.11 a barrel.

Gold futures for December delivery gained $37 to $1,750.20 an ounce. Earlier, gold prices hit a record intraday high of $1,782.50 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury fell, pushing the yield up to 2.39% from 2.34% late Monday.

The yen and the Swiss franc strengthened as concern over a U.S. economic slowdown, tumbling stock markets and the euro region’s debt crisis spurred demand for the currencies as a refuge.

The dollar fell against the euro and the yen on speculation the Federal Open Market Committee will repeat its pledge to maintain stimulus measures to revive the economy. The franc reached records versus the euro and the dollar. The benchmark Stoxx Europe 600 Index rose, after falling earlier for the eighth consecutive day.

“Investor sentiment is very fragile, boosting demand for the safest currencies, such as the yen and franc,” said Lee Hardman, a strategist at Bank of Tokyo-Mitsubishi UFJ Ltd. in London. “There’s a strong focus on today’s FOMC meeting. The market is looking for another shot in the arm from more quantitative easing. Investors are hesitant to buy the dollar given the risk of more quantitative easing.”

The Japanese currency has almost erased its decline since the nation’s unilateral intervention in the foreign-exchange market pushed it to as weak as 80.24 per dollar on Aug. 4. That same day, The Bank of Japan added 10 trillion yen of stimulus. BOJ Governor Masaaki Shirakawa today said volatile exchange rates could have a “negative impact” on the economy.

The Federal Reserve meets today on monetary policy and may prolong a pledge to maintain record stimulus, economists at JPMorgan Chase & Co., BNP Paribas SA and Goldman Sachs Group Inc. said. The Fed could commit to hold its $2.87 trillion balance sheet steady for an “extended period,” they said.

Fed policy makers are likely to embark on a third round of large-scale asset purchases, moving “more decisively” to secure the U.S. recovery, Harvard University economist Kenneth Rogoff said.

Federal Reserve policymakers face enormous challenges and pressures ahead of the 1815GMT announcement today.

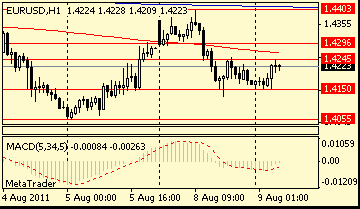

EUR/USD

Offers: $1.4300/05, $1.4320/30, $1.4350/60, $1.4400

Bids: $1.4250/45, $1.4225/20, $1.4205/00, $1.4185/80, $1.4160/50, $1.4130, $1.4100

EUR/USD $1.4100, $1.4150, $1.4200, $1.4250, $1.4285, $1.4385

USD/JPY Y77.00, Y77.50, Y78.00, Y78.50

EUR/JPY Y113.00

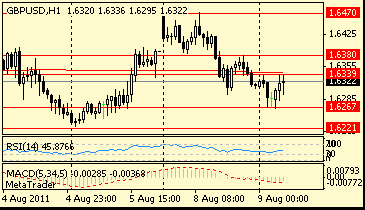

GBP/USD $1.6330, $1.6285, $1.6100

EUR/GBP stg0.8750

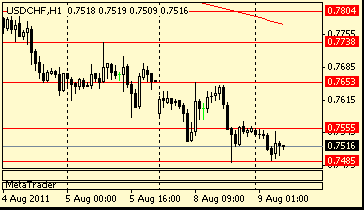

USD/CHF Chf0.7500, Chf0.7800

AUD/USD $1.0300, $1.0400

Aussie trades higher approaching $1.0200 mark, tracking euro-dollar gains. Resistance seen at $1.0210 ahead of offers at $1.0250/60. Aussie bids remain at $1.0085.

EUR/USD $1.4100, $1.4150, $1.4200, $1.4250, $1.4285, $1.4385

USD/JPY Y77.00, Y77.50, Y78.00, Y78.50

EUR/JPY Y113.00

GBP/USD $1.6330, $1.6285, $1.6100

EUR/GBP stg0.8750

USD/CHF Chf0.7800

Nikkei 8,944 -153.08 -1.68%

Hang Seng 19,576 -914.44 -4.46%

S&P/ASX 4,035 +48.72 +1.22%

Shanghai Composite 2,526 -0.75 -0.03%

Data:01:30 Australia National Australia Bank's Business Confidence (Jul) 2

01:30 Australia Home Loans (Jun) 0.0%

02:00 China Producer Price Index (YoY) (Jul) 7.5%

02:00 China Consumer Price Index (YoY) (Jul) 6.5%

05:00 Japan Consumer Confidence Index (Jul) 37.0

forecasts for these look for the visible trade balance to come in at -8.2 billion with total trade at -3.8 billion. IP is expected to rise

by 0.4% m/m, 0.2% y/y with manufacturing output up 0.2% m/m, 2.9% y/y. Also, at 1400GMT UK NIESR GDP growth data is due.

Federal Reserve policymakers face enormous challenges and pressures ahead of the 1815GMT announcement today.

The dollar rose to a four-month high against Australia’s currency and gained versus the euro as investors sought the refuge of U.S. government debt even after the rating cut as stocks fell. Treasury two-year note yields reached a record low. Canada’s dollar reached a four-month low versus the greenback as crude oil, the nation’s biggest export, plunged.

U.S. two-year note yields decreased as much as six basis points, or 0.06 percentage point, to an all-time low of 0.23 percent. Yields on 10-year notes tumbled 19 basis points to 2.37 percent. The Standard & Poor’s 500 Index dropped 3.6 percent following the biggest weekly fall since 2008.

Moody’s Investors Service reiterated that it affirmed the U.S.’s top Aaa ranking because the dollar’s status as the main reserve currency allows it to support higher debt levels than other countries, Moody’s analyst Steven Hess wrote in a report.

UK data includes the Trade Balance and Index of Production for June at 0830GMT as well as BOE Quoted Rates data at the same time. The median

forecasts for these look for the visible trade balance to come in at -8.2 billion with total trade at -3.8 billion. IP is expected to rise

by 0.4% m/m, 0.2% y/y with manufacturing output up 0.2% m/m, 2.9% y/y. Also, at 1400GMT UK NIESR GDP growth data is due.

Federal Reserve policymakers face enormous challenges and pressures ahead of the 1815GMT announcement today.

Resistance 3: Y79.40 (Aug 5 high)

Resistance 2: Chf0.7740 (Aug 5 high)

Resistance 3: $ 1.6470 (Jun 7 high, Jul 29 high, Aug 1 and 8 high)

FTSE 100 -142.18 -2.71% 5,104.81

CAC 40 -153.37 -4.68% 3,125.19

DAX -312.89 -5.02% 5,923.27

Dow -633.78 -5.54% 10,810.83

Nasdaq -174.72 -6.90% 2,357.69

S&P 500 -79.85 -6.66% 1,119.53

10 Year Yield 2.34% -0.22 --

Oil $81.01 -0.30 -0.37%

Gold $1,717.00 +3.80 +0.22%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers