- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 07-07-2011

DB alters June payroll forecast due to the ADP results being much better than expected (+157k pvt in June). DB says "With the public sector shedding on average -25k jobs per month, headline nonfarm payrolls should come in at +175k. Previously, we were forecasting +100k. Our forecast of a one tenth decline in the unemployment rate (to 9.0%) remains intact."

The tech sector, which is the largest by market weight, is up a strong 1.4% at the moment. It is currently led by the likes of Western Digital (WDC 38.59, +1.20) and Seagate Technology (STX 16.92, +0.60), both of which were recently upgraded by analysts at JPMorgan. Not all tech issues are in favor, though; shares of IBM (IBM 176.55, -1.16) are in the red after they were downgraded by analysts at Wells Fargo.

- No precommitment;

- ECB to analyze,decide anew each month;

- Official interest rates still relatively low;

- Economy in EMU currently developing quite dynamically;

- Dynamic economy can naturally foster price increases;

- Since 3Q11, infl expectations risen slowly but steadily;

- Inflation expectations decisive for monetary policy;

- Mon policy not tailor-made for individual countries;

- Notes ECB fcasts show avg infl under 2% again in 2012;

- High infl of recent months mainly due energy, raw materials;

- Rate hike today to prevent broad-based infl pressures;

- ECB does not orient mon policy by what markets expect

All three major equity averages are at their best levels of the day. Their advance has been steady.

Materials stocks have benefitted from accelerating buying interest, though. The sector is now up 1.6%, which is second only to the financial sector's 1.7% gain. Among basic materials plays, metals and mining name Freeport McMoRan (FCX 55.66, +2.14) is a top performer as it boasts a big 4% gain.

The euro stemmed a two-day drop versus the dollar as European Central Bank President Jean-Claude Trichet signaled more interest-rate increases after raising the benchmark to 1.5 percent.

The 17-member currency gained after Trichet said policy makers loosened collateral rules for Portuguese bonds to support local banks.

“We’ve seen a significant turnaround in the euro,” said John McCarthy, managing director of currency trading at ING Groep NV in New York. “In terms of accommodating Portuguese debt, it was seen as a positive and the principal reason we saw the euro rise.”

ECB policy makers increased the target lending rate by a quarter-percentage point.

“Our monetary-policy stance remains accommodative,” Trichet said at a press conference in Frankfurt. “It is essential recent price developments do not give rise to broad-based inflation pressures over the medium term.”

The ECB waived some of its collateral rules to provide a lifeline to Greek banks a year ago. While banks can currently obtain as much money as they need from the ECB for up to three months against eligible assets, including government bonds, policy makers had said they may no longer accept Greek debt as collateral if the country defaults.

Suspending the collateral rules for Portugal “does show that the ECB is willing to maintain liquidity in the market, yet it does expose the ECB to risks should we see haircuts” on defaulted bonds, said Jeremy Stretch, head of currency strategy at Canadian Imperial Bank of Commerce in London. “They are trying to be ahead of the game if Portugal’s bonds receive a default rating.”

The dollar dropped against most of its major counterparts as U.S. companies added more workers in June than economists forecast, damping demand for haven assets before the government’s payrolls report tomorrow.

Companies added 157,000 workers last month, ADP Employer Services reported today, surpassing the 70,000 forecast by 36 economists in a Bloomberg News survey. Initial jobless claims fell by 14,000 to 418,000 in the week ended July 2, the Labor Department said today.

Nonfarm payrolls increased by 105,000 in June after an advance of 54,000 in the prior month, according to the median estimate of 83 economists in a Bloomberg News survey before tomorrow’s payrolls report from the Labor Department. The unemployment rate probably stayed at 9.1 percent.

The yen and Swiss franc were the biggest losers among major currencies as stocks and commodities rallied on U.S. employment reports, boosting demand for Brazil’s real and the Canadian dollar.

The Nasdaq has stretched its advance so that it now sits at a fresh session high witha gain that is double that of the Dow. The Nasdaq's impressive performance comes amid strong buying interest in large-cap issues like Apple (AAPL 356.76, +5.00), Intel (23.26, +0.51), and Oracle (ORCL 33.78, +0.57).

Pierpont previews Jun jobs (they est +130k), saying the labor mkt "was probably never quite as good as the initial April (jobs) reading nor as soft as the tepid May figure." But jobs cooled in May and the Q is "whether the moderation proves persistent or even worsens." Even if weather and Japan slowed Q2 growth, downside risks persist, they warn.

The dollar index moved into negative territory in recent trade, which has given commodities a boost.

Natural gas has been in positive territory for the past hour and a half, approx., but has slowly pulled back about $0.02/MMBtu during this time. Ahead of inventory data, nat gas was at $4.23, up $0.01. Following the data, which showed versus a build of 95 bcf versus the consensus of ~80 bcf, nat gas fell sharply to new session lows of $4.08; now at $4.09, down 3.3%.

Crude oil rallied sharply about 45 minutes before floor trading began, gaining about $2/barrel and pushing to new session highs of $99.07/barrel.

Silver has been in positive territory all morning, while gold has been chopping around the unchanged line in a tight range of around $1526 to $1530. Silver rose as high as $36.47/oz at around 9:00am EST and is now 1.2% higher at $36.36/oz. Gold is down $1.20/oz. at $1527.90/oz.

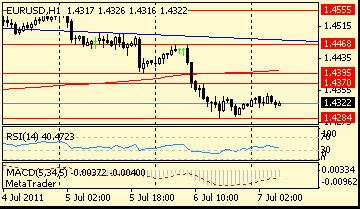

EUR/USD continues rising, currently holding around $1.4352 after it triggered stops. rate broke above overnight high at $1.4345. Euro probes $1.4350 now with stops in place above.

USD/JPY Y80.70, Y80.85, Y81.00, Y81.30

EUR/JPY Y116.55

GBP/USD $1.5975, $1.6165

USD/CHF Chf0.8370, Chf0.8400

AUD/USD $1.0740, $1.0750

EUR/GBP recovers from recent lows around stg0.8902 to current stg0.8940 amid sharp recovery in EUR/USD and GBP/USD below $1.6000. Resistance seen into stg0.8950 (61.8% stg0.89795/0.89045), a break to open a move toward

stg0.8960 ahead of stg0.8980.

- upward price pressure from energy still visible;

- no second-round effects;

- inflation expectations must stay firmly anchored;

- risks to inflation outlook on upside;

- inflation risks in particular due energy prices;

- M3 has continued to edge up over recent months;

- loans to priv sector continue to strengthen slightly;

- banks must continue to expand credit provision;

- shld use better-than-expected econ devels to cut deficits;

- we do always what we judge necessary for price stability;

- last two rate hikes done at right time;

- markets didn't expect rate hikes 2011 until we gave sign.

- further adjustment of interest rates warranted;

- still upside risks to price stability;

- no broad-based inflation pressures in mid term;

- interest rates low;

- policy accommodative;

- some deceleration in econ growth expected in 2Q;

- underlying growth momentum positive, uncertainty high;

- monitoring all developments very closely;

- all nonstandard measures temporary by nature;

- recent data show continued expansion of economic activity;

- but economic activity at slower pace;

- strong 1Q growth due partly to special factors.

U.S. stocks were set to extend gains Thursday as investors reacted to a pair of jobs reports that showed stronger-than-expected results.

Economy: Before the bell the U.S. government's weekly report on initial unemployment claims showed that 418,000 people filed for unemployment in the week ended July 2. Economists had expected a total of 425,000 jobless claims last week.

Separately, a report from payroll services firm ADP showed that employers in the private sector added 157,000 workers in June, far exceeding expectations. The ADP was expected to show that employers in the private sector added 60,000 workers in June.

Economists are expecting the Payrolls report to show 120,000 jobs added to payrolls.

World markets: European stocks rose in midday trading. Britain's FTSE 100 and the DAX in Germany each surged 0.8% and France's CAC 40 gained 0.5%.

Asian markets ended mostly lower. The Shanghai Composite fell by 0.6%, the Hang Seng in Hong Kong ended flat and Japan's Nikkei ticked down by 0.1%.

- upward price pressure from energy still visible;

- no second-round effects;

- inflation expectations must stay firmly anchored;

- risks to inflation outlook on upside;

- inflation risks in particular due energy prices;

- M3 has continued to edge up over recent months;

- loans to priv sector continue to strengthen slightly;

- banks must continue to expand credit provision;

- shld use better-than-expected econ devels to cut deficits;

- we do always what we judge necessary for price stability;

- last two rate hikes done at right time;

- markets didn't expect rate hikes 2011 until we gave sign.

- further adjustment of interest rates warranted;

- still upside risks to price stability;

- no broad-based inflation pressures in mid term;

- interest rates low;

- policy accommodative;

- some deceleration in econ growth expected in 2Q;

- underlying growth momentum positive, uncertainty high;

- monitoring all developments very closely;

- all nonstandard measures temporary by nature;

- recent data show continued expansion of economic activity;

- but economic activity at slower pace;

- strong 1Q growth due partly to special factors.

Data released:

08:30 UK Industrial production (May) 0.9% 1.1% -1.7%

08:30 UK Industrial production (May) Y/Y -0.8% -0.5% -1.2%

08:30 UK Manufacturing output (May) 1.8% 1.0% -1.5%

08:30 UK Manufacturing output (May) Y/Y 2.8% 2.1% 1.3%

10:00 Germany Industrial production (May) seasonally adjusted 1.2% 0.9% -0.8 (-0.6)%

10:00 Germany Industrial production (May) not seasonally adjusted, workday adjusted Y/Y 7.6% - 9.3 (9.6)%

11:00 UK BoE meeting announcement 0.50% 0.50% 0.50%

The euro touched a one-week low as concern that Greece may become the currency region’s first default outweighed prospects for higher interest rates from the European Central Bank.

The euro holds tight as investors considered whether ECB President Jean-Claude Trichet will comment on the central bank’s acceptance of Greek debt as loan collateral in the event of a default. The ECB raised its key rate 25 basis points to 1.5%, as expected.

Today’s conference is “about what the ECB says about rate hikes going forward,” said Paul Robson, a senior foreign-exchange strategist at Royal Bank of Scotland Group Plc. “If they say risks to inflation and growth have moved to the downside, the euro would be quite vulnerable. Euro-dollar has had a very tight correlation with rate spreads over the last year, and that’s set to continue.”

The pound slipped against the greenback as the Bank of England left its key rate at a record-low 0.5%. The U.K. central bank also held its bond-purchase program at 200 billion pounds.

The Swiss franc weakened after a report showed inflation accelerated less than expected in June led by higher costs for energy. Consumer prices increased 0.6% from a year earlier, after rising 0.4% in May. Economists had forecast an inflation rate of 0.7%.

EUR/USD printed session high on $1.4350 before held within the range, limited by $1.4270/$1.4320. Later rate resumed decline to $1.4250.

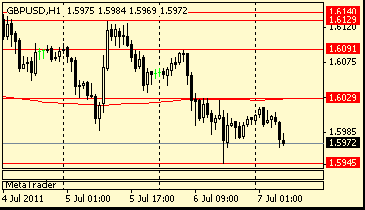

GBP/USD failed to set above $1.6000 and retreated to below the figure - now at $1.5970.

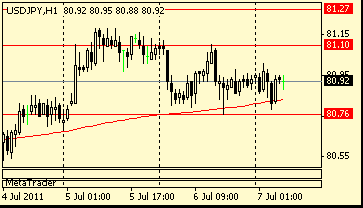

USD/JPY rose to Y80.12 following some consolidation between Y80.90/Y81.00.

The ECB President Jean-Claude Trichet conference is due at 1230GMT.

At 1215GMT, the ADP National Employment Report is due. Last month the unexpectedly soft reading caused some to revise their estimates

lower. The lackluster 54,000 increase in non-farm payrolls justified the revision. At 1230GMT, initial jobless claims are expecting toll to 420,000 in the July 2 week. Claims have been above 420,000 since the April 30 week. In the July 25 week, a labor analyst said there no special factors

contributing to the decline of 1,000 claims.

Focus is on ECB President Jean-Claude Trichet's language at the regular press conference at 1230GMT. Futures point to around 97% chance of a 25bps rate hike today after Trichet last month signalled "strong vigilance". Markets expect Trichet to revert to "monitor closely" in the opening statement, but at the same time say risks to price stability still seen to be on the upside.

GBP/USD holds around $1.5980 followint the interest rate decision from the BOE MPC. Support seen at $1.5965/60, a break to expose the earlier lows at $1.5944, with demand seen in place between $1.5945/35. Resistance remains in place toward $1.6020.

Gold prices managed to close above the 55 and 21-DMAs, now initial support at $1519.5/1520.9, respectively. Daily studies remain mixed. Initial resistance seen at $1530.9/1532.1 (May 25/26 highs) with a break above targets $1552.7/1554/1558 (9-wk resistance line, Daily Boll top, and Jun 22 reversal high). Break under $1519.5/1520.9 opens the way down to $1510.5/1512.7 (5-day MA, 23.6% Fibonacci $1309/1576).

The euro holds near one-week lows versus the dollar on Thursday as worries about Europe's sovereign debt problems outweighed a widely expected interest rate hike by the European Central Bank.

if anything, a softening in ECB President Jean-Claude Trichet's hawkish stance, or even a lack of more hawkish comments, could further weigh on the euro, traders said.

"If Trichet's comments just underline expectations of gradual tightening in the future, the market may be disappointed and sell the euro," said Katsunori Kitakura, chief dealer at Chuo Mitsui Trust Bank.

Concern that Greece's debt crisis would spread to other highly indebted peripheral euro zone countries flared up this week after Moody's slashed its rating for Portugal to junk status.

Moreover, the Moody's Investors Service has today downgraded the government-guaranteed debt of four Portuguese banks - Caixa Geral de Depositos (CGD), Banco Espirito Santo (BES), Banco Comercial Portugues (BCP) and Banco Internacional do Funchal (Banif).

Still, analysts don't expect the euro to fall too sharply in the months ahead, underpinned by higher interest rates.

The dollar benefited from the euro's woes, rising against a basket of major currencies. The dollar index climbed near 75.00, pulling further away from a one-month low of 74.13 set earlier in the week.

The Australian dollar recovered from a dip to one-week lows after data showed Australian employment rose by more than expected in June.

The number of people employed in Australia rose by 23,400. That was higher than the median estimate for a 15,000 increase. The jobless rate held at 4.9%.

EUR/JPY currently holds around Y115.78, above session lows on Y115.54. Support comes now at Y115.20/10. On the topside we have stops mentioned between Y116.30-60. resistance is around 100 day MA at Y116.42, a break here opens Y117.00.

EUR/USD $1.4400, $1.4430, $1.4475, $1.4500

USD/JPY Y80.70, Y80.85, Y81.00, Y81.30

EUR/JPY Y116.55

GBP/USD $1.5975, $1.6165

USD/CHF Chf0.8370, Chf0.8400

AUD/USD $1.0740, $1.0750

01:30 Australia Employment Change s.a. (Jun) 23.4K

The euro traded near the lowest level in a week against the Swiss franc after analysts said Ireland’s credit rating may be cut to junk by Moody’s Investors Service following Portugal’s loss of its investment-grade rating.

The euro snapped yesterday’s loss against the dollar and yen after Moody’s said it differentiates “significantly” among European periphery countries, suggesting it may not imminently cut Ireland’s rating to junk in line with Portugal and Greece.

The European Central Bank will increase its main refinancing rate to 1.50 percent today from 1.25 percent, according to all economists in a survey. The central bank may increase borrowing costs further in the fourth quarter, according to a separate survey.

European data starts at 1000GMT by German in industrial output data. At 1145GMT, the ECB decision is due, which will be followed at 1230GMT

by the usual press conference with ECB President Jean-Claude Trichet.

UK data includes at 0830GMT Industrial Production/Manufacturing Output data is due for release. The data is expected to show a bit of a rebound from the previous month, with industrial production rising 1.3% m/m but remaining lower by a reading of -0.4% y/y. Manufacturing output is seen

up 1.1% m/m, 2.2% y/y. The Bank of England Monetary Policy Committee makes it's announcement at 1100GMT but no change is expected in either

the current 0.50% overnight rate or the 200 billion level of asset purchases.

At 1215GMT, the ADP National Employment Report is due. Last month the unexpectedly soft reading caused some to revise their estimates

lower. The lackluster 54,000 increase in non-farm payrolls justified the revision. At 1230GMT, initial jobless claims are expecting toll to 420,000 in the July 2 week. Claims have been above 420,000 since the April 30 week. In the July 25 week, a labor analyst said there no special factors

contributing to the decline of 1,000 claims.

Nikkei 10,071 -11.34 -0.11%

Hang Seng 22,542 +24.31 +0.11%

S&P/ASX 4,606 +0.46 +0.01%

Shanghai Composite 2,794 -16.21 -0.58%

European data starts at 1000GMT by German in industrial output data. At 1145GMT, the ECB decision is due, which will be followed at 1230GMT

by the usual press conference with ECB President Jean-Claude Trichet.

UK data includes at 0830GMT Industrial Production/Manufacturing Output data is due for release. The data is expected to show a bit of a rebound from the previous month, with industrial production rising 1.3% m/m but remaining lower by a reading of -0.4% y/y. Manufacturing output is seen

up 1.1% m/m, 2.2% y/y. The Bank of England Monetary Policy Committee makes it's announcement at 1100GMT but no change is expected in either

the current 0.50% overnight rate or the 200 billion level of asset purchases.

At 1215GMT, the ADP National Employment Report is due. Last month the unexpectedly soft reading caused some to revise their estimates

lower. The lackluster 54,000 increase in non-farm payrolls justified the revision. At 1230GMT, initial jobless claims are expecting toll to 420,000 in the July 2 week. Claims have been above 420,000 since the April 30 week. In the July 25 week, a labor analyst said there no special factors

contributing to the decline of 1,000 claims.

Moody's Investors Service has today downgraded the government-guaranteed debt of four Portuguese banks - Caixa Geral de Depositos (CGD), Banco Espirito Santo (BES), Banco Comercial Portugues(BCP) and Banco Internacional do Funchal (Banif) - following the downgrade of the Portuguese government to Ba2 (negative outlook).

08:30 UK Industrial production (May) 1.1% -1.7%

08:30 UK Industrial production (May) Y/Y -0.5% -1.2%

08:30 UK Manufacturing output (May) 1.0% -1.5%

08:30 UK Manufacturing output (May) Y/Y 2.1% 1.3%

10:00 Germany Industrial production (May) seasonally adjusted - -0.6%

10:00 Germany Industrial production (May) not seasonally adjusted, workday adjusted Y/Y - 9.6%

11:00 UK BoE meeting announcement 0.50% 0.50%

11:45 EU(17) ECB meeting announcement 1.50% 1.25%

12:30 EU(17) ECB press conference

12:15 USA ADP employment (June) +70K +38K

12:30 USA Jobless claims (week to 02.07) 420K 428K

20:30 USA M2 money supply (27.06), bln - +30.0

23:50 Japan Current account (May) unadjusted, trln - 0.406

23:50 Japan Trade balance (May) unadjusted, trln - -0.418

23:50 Japan (M2+CDs) money supply (June) Y/Y - 2.7%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers