- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-08-2011

- We welcome the agreement to raise the U.S. government's borrowing limit and cut the budget deficit.

- By reducing a major uncertainty in the markets and bolstering U.S. fiscal credibility, this agreement is good for both the U.S. and the global economy.

- Raising the debt ceiling means a severe economic disruption has been avoided, and the accompanying deficit reduction deal is an important step toward fiscal consolidation.

- Given the fragility of recovery, the planned spending cuts are appropriately phased and not overly frontloaded so as not to undermine growth.

- Enactment of legislation to raise the debt ceiling Tuesday averts an economically damaging debt crisis in the very near term, but it leaves plenty for the Federal Reserve to worry about.

- Passage of the $2.4 trillion debt deal means the Fed will not have to engage in various acrobatics to assist the Treasury in paying its bills.

- It faces larger challenges in the months and years ahead as it tries to cope with a struggling economy.

General Motors (GM) reported July U.S. sales added 7.6% to 214,915 vehicles vs. expected +7%.

Ford Motor (F) reported July U.S. sales advanced by 9% to 180,865 vehicles vs. expected +7.6%.

Honda Motor (HMC) said its July sales fell 28.4% to 80,052 vehicles.

Toyota Motor (TM) said its July sales fell 22.7% to 130,802 vehicles.

Nissan Motor (NSANY) said its sales rose just 2.7% to 84,601 vehicles.

(The data were compared to the same month a year earlier).

US dollar renewed its decline amid concern that crafted agreement between Barack Obama and congressional leaders to raise the federal debt ceiling and spending reduction may lead to slowdown in economic recovery. Today Senate approved the debt limit hike bill. According to the plan, the U.S. debt limit will be raised by at least $2.1 trillion and cut federal spending by $2.4 trillion.

European stocks tumbled to the lowest level in 11 months amid concern that a slowdown in the world’s largest economy may derail global growth. Another pressure for the currency is surging bond yields in Italy reawakened concern that the region’s debt crisis will worsen amid slowing global growth. Italy’s 10-year yield jumped to the most since 1997.

The Swiss franc climbed to a new life-time high today. It was supported by “save haven” status and beating statistics on Swiss SVME PMI and retail sales.

The Australian dollar sheds today after the nation’s central bank kept its main interest rate unchanged.

The yen remain under pressure amid speculations Japan will intervene in currency markets. Today Japanese Finance Minister Yoshihiko Noda said the nation’s currency is overvalued and he’s watching markets closely.

- Pres Obama has begun speaking, is lauding the debt bill as an important first step in fiscal reform.

- Says can't close deficit all at once, need a balanced approach.

- Growing the US econ is not just about cutting spending, wants Congress to take other steps so businesses can hire.

- Will urge extending tax cuts to middle class families.

- Pres Obama says will work with Congress to grow the economy.

- "As it expected, agreement was reached on an increase in the United States' debt ceiling commensurate with its 'AAA' rating".

- "The risk of sovereign default remains extremely low. The agreement is an important first step but not the end of the process towards putting in place a credible plan to reduce the budget deficit to a level that would secure the United States' 'AAA' status over the medium-term."

The markets continue declining amid concerns about a possible U.S. government credit downgrade and faltering growth in the world’s largest economy.

JPMorgan said the PI report has not set the US up well for Q3: "We are inclined to revise lower our Q3 GDP estimate from an already-below-consensus 2.5% pending today's July vehicles sales report, which will allow some further refinement of how consumption is tracking this quarter."

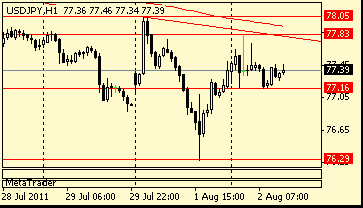

The rate extends losses through support to hit a new session low Y77.07. Traders look to bids at Y77.10/05 and Y76.85/80. The pair is currently Y77.11 in light dealings.

S&P futures vs fair value: -9.60. Nasdaq futures vs fair value: -12.30.

Italy’s 10-year yield jumped to the most since 1997.

European producer-price inflation slowed to 5.9 percent from 6.2 percent in May, the European Union’s statistics office in Luxembourg said today. The result strengthened the case for the European Central Bank to keep interest rates unchanged this week.

Demand for the dollar was limited on concern an agreement between President Barack Obama and Congressional leaders on raising the debt ceiling and spending cuts will weigh on growth in the world’s biggest economy. The House approved legislation to raise the U.S. debt limit by at least $2.1 trillion and cut federal spending by $2.4 trillion or more. The measure goes to the Senate for a final vote planned today.

Offers $1.4250/55, $1.4235, $1.4205/10.41847)

Bids $1.4150, $1.4140, $1.4110/00, $1.4070/50, $1.4015/00

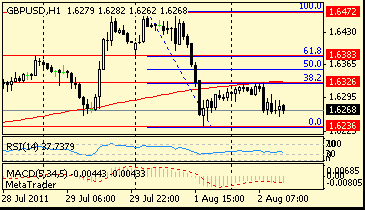

Despite reports of decent demand seen around $1.6270 the rate sinks to $1.6257, but dip attracts frseh demand, allows rate to edge back toward that $1.6270 level. Demand/support seen at $1.6255/50 with stops below.

GBP/USD holds near session lows around $1.6272. Rate tried to recover but still under pressure. Tech resistance mentioned at $1.6314 (76.4% Fibo of $1.6329/1.6264).

Data released:

03:30 Australia RBA meeting announcement 4.75% 4.75% 4.75%

The yen fell amid speculations Japan will intervene in currency markets.

The yen dropped against the euro for the first time in five days after Japanese Finance Minister Yoshihiko Noda said the nation’s currency is overvalued and he’s watching markets closely.

The Nikkei newspaper reported that Japanese officials are concerned that the yen’s strength will hurt domestic companies and undermine the nation’s recovery from the March 11 earthquake and tsunami. Noda declined to comment on possible currency intervention today.

Bank of Japan officials in the past week have voiced more concern about the currency, with board member Hidetoshi Kamezaki saying the central bank would need to act “proactively” should the yen’s gains pose a threat to growth and prices. The BOJ is set to meet on policy this week.

Japan last intervened on March 18, joining Group of Seven counterparts in selling the yen a day after it jumped to a record against the dollar.

“BOJ intervention in the past has only slowed the pace of JPY appreciation,” BNP Paribas SA analysts wrote yesterday. “If the BOJ does intervene the result may be the same.”

Demand for the dollar was limited on concern an agreement between President Barack Obama and Congressional leaders on raising the debt ceiling and spending cuts will weigh on growth in the world’s biggest economy. The House approved legislation to raise the U.S. debt limit by at least $2.1 trillion and cut federal spending by $2.4 trillion or more. The measure goes to the Senate for a final vote planned today.

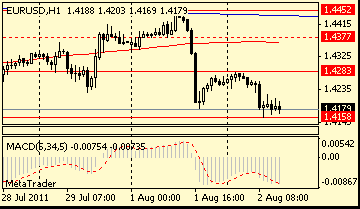

EUR/USD continued to weaken from $1.4280 and printed session lows around $1.4150.

GBP/USD also fell from $1.6330 to $1.6260.

USD/JPY tested Y77.15 before recovered to Y77.36.

US personal income/spending are scheduled to release at 12:30 GMT.

EUR/USD: $1.4195, $1.4200, $1.4295, $1.4400

USD/JPY: Y78.00, Y78.10

USD/CHF: Chf0.8100

AUD/USD: $1.1000, $1.1025

EUR/USD

Bids: $1.4200, $1.4185

GBP/USD

Offers: $1.6325/30, $1.6350/60, $1.6390/00, $1.6420

Bids: $1.6285/80, $1.6260/50, 1.6240

USD/JPY

Offers: Y77.80/85

Bids: Y77.10/15

AUD/USD

Bids: $1.0880, $1.0870, $1.0850

EUR/GBP

Offers: stg0.8750/55

Bids: stg0.8700, stg0.8675/70

Majors close:

Nikkei +131.98 (+1.31%) 9965.01

DAX -204.79 (-2.86%) 6,954

CAC -83.23 (-2.27%) 3,588

FTSE-100 -40.76 (-0.70%) 5,774

Dow -10.75 (-0.09%) 12,132

Nasdaq -10.75 (-0.46%) 2,335.25

S&P500 -5.34 (-0.41%) 1,287

Oil -0.10 (-0.11%) $94.79

10-Years 2.74% 0.00

Asian stock markets ended Monday higher.

Just before the open, the markets received a powerful stimulus to growth from U.S. President Barack Obama’s announcement of a framework agreement to lift the nation’s debt ceiling and avert a sovereign default sparked a relief rally.

This growth was curbed by released data on China’s PMI Manufacturing. Official survey by the China Federation of Logistics and Purchasing earlier showed a drop in the nation’s PMI to 50.7 in July from 50.9 in June, but remained above the threshold of 50, indicating an expansion. Then HSBC reported its July China manufacturing purchasing managers’ index fell to 49.3 from 50.1 in June.

HSBC noted the China’s manufacturing activity signaling deterioration in the operating environment at the nation’s factories as tighter monetary conditions weigh further on the sector.

Statistics by HSBC also showed Taiwan’s PMI eased to 46.1 in July from 49.9 in June, while India’s monthly manufacturing PMI declined to 53.6 from 55.3 in June. The reading for South Korea was 51.3, which HSBC said has been “broadly unchanged” over the last three survey periods.

The Taipei index weighed by sharp losses in Formosa Plastics Group firms after a weekend fire at a refining complex of Formosa Petrochemical Corp.

Today the banking sector was among the main leaders: Westpac Banking Group Ltd. added 1.9% in Sydney, Sumitomo Mitsui Financial Group Inc. increased by 2.9% in Tokyo. HSBC Holdings PLC climbed by 0.5% in Hong Kong, after announcing a deal to sell 195 of its U.S. retail branches to First Niagara Financial Group Inc. for approximately $1 billion in cash.

The U.S. debt agreement news boosted oil prices and, as a result, shares of in the region’s energy producers: Inpex Corp. +0.7% in Tokyo, Woodside Petroleum Ltd. +1.4% in Sydney, Cnooc Ltd. +0.9% and PetroChina Co. +1.6% Hong Kong.

European stock markets closed the first day of the week on dark mood.

On Monday the European markets appeared under pressure from data on EU and UK business activity, which missed analysts’ estimates, reinforcing concerns about countries’ economies in Europe. Moreover the IMF lowered its forecast for UK GDP 2011 to 1.5% from April's forecast of 1.75%.

Market plaers also worried that agreement on the US debt deal might not be sufficient to placate the rating.

The main factor to fall was a report by the Institute for Supply Management (ISM), which showed a slowing manufacturing business activity that missed median estimates.

Banking sector suffered substantial losses: in London shares of Royal Bank of Scotland Group PLC and Lloyds Banking Group PLC showed a decrease of 4.5% and 5%, respectively, in Frankfurt Deutsche Bank AG’ shares fell by 3.9% and Commerzbank AG’ – by 5.2%, in Paris shares of BNP Paribas SA – by 3.9% and Societe Generale SA’ - more than 4%.

As most financials slid, shares of heavily weighted HSBC Holdings PLC managed to hold on to a 2.2% gain after posting a 35% gain in first-half net profit and saying it will cut 30,000 jobs. Its pretax profit rose 3.3%, topping forecasts.

HSBC also announced its plans to sell 195 retail branches in upstate New York to First Niagara Financial Group Inc. for around $1 billion.

Shares of BMW AG lost 3.9% on Monday.

Auto-related stocks also sold off sharply, with tire maker Michelin declining 4.2% despite earlier UBS upgraded the company’s shares from Neutral from Sell.

US equities also closed lower on Monday.

The markets were under pressure amid weak ISM manufacturing and concerns that rating agencies may downgrade US credit rating despite the US debt ceiling agreement.

The decline was curbed by reports that on the weekends the U.S. Republicans and Democrats reached an agreement on hiking debt ceiling and deficit reduction. According to the agreement, the debt limit may be raised by $2.1 trillion and the federal deficit may be cut by $2.5 trillion. over the next 10 years.

Economy: The Institute for Supply Management (ISM) reported the pace of growth in the U.S. manufacturing sector slowed more than expected in July while new orders hit their lowest level since 2009 (50.9 in July vs. est. 53.0 and 55.3 in June).

The US construction spending added 0.2%, up from estimated advance by 0.1% and June rise by 0.3%.

On Monday top losers were defense and healthcare companies amid US governments decision to cut federal spending.

Shares of HSBC Holdings PLC (HBC) added 1.6% after the London-based bank announced it will eliminate 25,000 jobs by 2013. The bank has already trimmed 5,000 jobs. The job cuts are seen as a positive, since they help the bank reduce costs. HSBC also posted a solid profit.

Data released:

07:45 Italy PMI (July) 50.1 48.5 49.9

07:50 France PMI (July) 50.5 50.1 52.5

07:55 Germany PMI (July) seasonally adjusted 52.0 52.1 54.6

08:00 EU(17) PMI (July) 50.4 50.4 52.0

08:30 UK CIPS manufacturing index (July) 49.1 51.1 51.3

09:00 EU(17) Unemployment (June) 9.9% 9.9% 9.9%

Switzerland National Day

Canada Civic Holiday

14:00 USA ISM Mfg PMI (July) 50.9 53.0 55.3

14:00 USA Construction spending (June) 0.2% 0.1% +0.3 (-0.6)%

Obama said from the White House that leaders of both parties in the U.S. House and Senate had approved an agreement to raise the nation’s debt ceiling by $2.1 trillion and cut the federal deficit by as much as $2.5 trillion over a decade.

Shortly before Obama spoke, Senate Majority Leader Harry Reid and Minority Leader Mitch McConnell took to the Senate floor to endorse the accord.

Treasury Secretary Timothy F. Geithner has said the U.S. will run out of options to prevent a default by tomorrow if the debt limit isn’t increased.

Standard & Poor’s said on July 14 that the chance of a downgrade is 50 percent in the next three months and it may cut the rating as soon as this month if there isn’t a “credible” plan to reduce the nation’s deficit.

Manufacturing purchasing managers' indexes across Europe suggested the euro-zone economy got off to a weak start in the third quarter. The data showed that activity at euro-zone factories slowed to a near standstill in July, with even Germany recording slower growth than expected.

The economic situation looked worse in the U.K. The PMI showed that U.K. manufacturing activity unexpectedly contracted last month for the first time in two years. That saw sterling fall more than half a cent against the dollar.

USD/JPY failed to break above Y78.00 and retreated to Y76.30.

Among EU data today the UK Jul PMI Construction comes at 08:30 GMT. EU inflation data will be in focus at 09:00 GMT.

US personal income/spending are scheduled to release at 12:30 GMT.

Resistance 3: Y78.70

Resistance 2: Y78.00

Resistance 1: Y77.80

Current price: Y77.25

Support 1:Y77.20

Support 2:Y76.30

Support 3:Y76.00

Comments: Overnight rate tested resistance at Y77.70/80 (channel lines from Jul 20 and Jul 08 crossing) and retreated. Support comes at Y77.20 (Asian low) with a break under widens losses to Monday's lows on Y76.30. Break above Y77.70/80 to open a way to yesterday's highs on Y78.00.

Oil continued to go lower in Asia today, slipping to $94.50 ahead of the European open. Expectations for this week's Crude inventory report are for a build of around 2 millions barrels which could add further downside pressure. Support is seen towards $94.00 and $93.43 with resistance at $96.27 and $97.38.

Resistance 3: Chf0.8030

Resistance 2: Chf0.7950

Resistance 1: Chf0.7850

Current price: Chf0.7798

Support 1: Chf0.7730

Support 2: Chf0.7700

Support 3: Chf0.7640

Comments: Techs hasn't changed much. Support is around Chf0.7730/20 (record low, Chf0.7720 - channel lines from Feb 16 and Jul 08 crossing), then - at Chf0.7000. Resistance comes at Chf0.7850 (Monday's local low), then - near Chf0.7950 (Monday's high).

Resistance 3:$1.6480

Resistance 1:$1.6325

Current price: $1.6280

Support 1: $1.6230

Support 2: $1.6210

Support 3: $1.6120

Comments: Rate failed to break above the resistance at $1.6325 (38.2% Fibo of yesterday's decline). Above the target is at $1.6380 (61.8% of the same move). Stronger level - at $1.6480 (Monday's high). Support is near $1.6230/40 (yesterday's lows). Below losses may widen to $1.6210 (38.2% Fibo of $1.5780-$1.6480 move) and then - to $1.6120 (50%).

Nikkei +131.98 (+1.31%) 9965.01

DAX -204.79 (-2.86%) 6,954

CAC -83.23 (-2.27%) 3,588

FTSE-100 -40.76 (-0.70%) 5,774

Dow -10.75 (-0.09%) 12,132

Nasdaq -10.75 (-0.46%) 2,335.25

S&P500 -5.34 (-0.41%) 1,287

Oil -0.10 (-0.11%) $94.79

10-Years 2.74% 0.00

Resistance 3:$1.4540

Resistance 2:$1.4500

Resistance 1:$1.4450

Current price: $1.4205

Support 1: $1.4180

Support 2: $1.4140

Support 2: $1.4020

03:30 Australia RBA meeting announcement 4.75% 4.75%

09:00 EU(17) PPI (June) 0.1% -0.2%

09:00 EU(17) PPI (June) Y/Y 5.9% 6.2%

12:30 USA Personal income (June) 0.1% 0.3%

12:30 USA Personal spending (June) 0.0% 0.0%

12:30 USA PCE price index ex food, energy (June) 0.2% 0.3%

12:30 USA PCE price index ex food, energy (June) Y/Y - 1.2%

12:55 USA Redbook (30.07)

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers