- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-05-2018

| raw materials | closing price | % change |

| Oil | 67.74 | +0.73% |

| Gold | 1,306.40 | -0.03% |

| index | closing price | change items | % change |

| Nikkei | -35.25 | 22472.78 | -0.16% |

| TOPIX | -2.66 | 1771.52 | -0.15% |

| Hang Seng | -84.57 | 30723.88 | -0.27% |

| CSI 300 | +6.77 | 3763.65 | +0.18% |

| KOSPI | -9.77 | 2505.61 | -0.39% |

| Euro Stoxx 50 | +17.53 | 3553.79 | +0.50% |

| FTSE 100 | +22.84 | 7543.20 | +0.30% |

| DAX | +190.14 | 12802.25 | +1.51% |

| CAC 40 | +8.72 | 5529.22 | +0.16% |

| DJIA | -174.07 | 23924.98 | -0.72% |

| S&P 500 | -19.13 | 2635.67 | -0.72% |

| NASDAQ | -29.81 | 7100.90 | -0.42% |

| Pare | Closed | % change |

| EUR/USD | $1,1955 | -0,31% |

| GBP/USD | $1,3575 | -0,27% |

| USD/CHF | Chf0,99819 | +0,19% |

| USD/JPY | Y109,83 | 0,00% |

| EUR/JPY | Y131,32 | -0,33% |

| GBP/JPY | Y149,105 | -0,22% |

| AUD/USD | $0,7492 | 0,06% |

| NZD/USD | $0,6995 | -0,15% |

| USD/CAD | C$1,28719 | +0,20% |

The main US stock indexes have moderately decreased, the reason for this was the fall in the shares of the health sector, as well as the results of the May meeting of the Fed.

As a result of a two-day meeting, the US Federal Reserve, as expected, left the key interest rate in the range of 1.5% -1.75%. In the accompanying statement, the Central Bank noted a slowdown in household spending compared to the high rate of the fourth quarter, but pointed to the continued strong growth of companies' investments in fixed assets. Also, the Fed noted a strong increase in the number of jobs. Meanwhile, this time the Fed did not begin to declare that "it closely follows the dynamics of inflation." This change reflects an increase in inflationary pressures in the United States. In addition, the Fed noted that the annual inflation approached the target level of the Central Bank, which is 2%. In general, the Fed's rhetoric allows investors to count on raising rates during the June meeting.

A certain influence on the course of trading also provided statistics on the United States. As shown by data from Automatic Data Processing (ADP), the growth rate of employment in the private sector of the US slowed in March, and almost coincided with the forecasts. According to the report, in April the number of employed increased by 204 thousand people compared with the figure for March at 241 thousand. Analysts had expected that the number of employed will increase by 200 thousand.

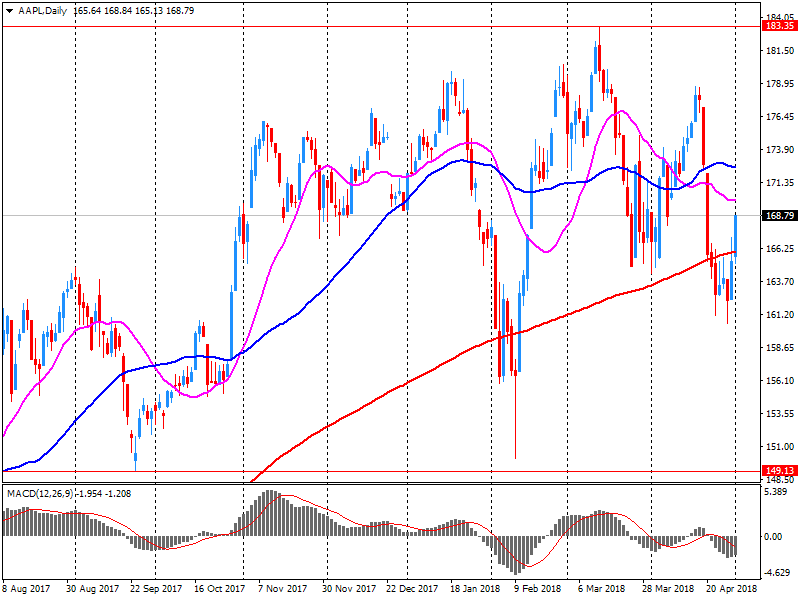

Most DOW components recorded a decline (24 out of 30). Outsider were the shares of Verizon Communications Inc. (VZ, -2.58%). The leader of growth was the shares of Apple Inc. (AAPL, + 4.38%).

Almost all sectors of S & P finished trading in the red. The health sector showed the greatest decline (-1.1%). Only the base materials sector grew (+ 0.1%).

At closing:

Dow 23,924.98 -174.07 -0.72%

S&P 500 2,635.67 -19.13 -0.72%

Nasdaq 100 7,100.90 -29.81 -0.42%

At 436.0 million barrels, U.S. crude oil inventories are in the lower half of the average range for this time of year.

Total motor gasoline inventories increased by 1.2 million barrels last week, and are in the upper half of the average range. Both finished gasoline inventories and blending components inventories increased last week. Distillate fuel inventories decreased by 3.9 million barrels last week and are in the lower half of the average range for this time of year. Propane/propylene inventories increased by 0.7 million barrels last week, and are in the lower half of the average range. Total commercial petroleum inventories increased by 5.4 million barrels last week.

U.S. stock-index futures were flat on Wednesday, as investors were cautious ahead of the announcement of the outcomes of the Federal Open Market Committee's May meeting at 18:00 GMT. Apple's (AAPL) solid quarterly results underpinned Nasdaq futures.

Global Stocks:

| Index/commodity | Last | Today's Change, points | Today's Change, % |

| Nikkei | 22,472.78 | -35.25 | -0.16% |

| Hang Seng | 30,723.88 | -84.57 | -0.27% |

| Shanghai | 30,723.88 | -84.57 | -0.27% |

| S&P/ASX | 6,050.20 | +35.00 | +0.58% |

| FTSE | 7,552.53 | +32.17 | +0.43% |

| CAC | 5,525.53 | +5.03 | +0.09% |

| DAX | 12,766.10 | +153.99 | +1.22% |

| Crude | $67.32 | | +0.10% |

| Gold | $1,309.60 | | +0.21% |

(company / ticker / price / change ($/%) / volume)

| Amazon.com Inc., NASDAQ | AMZN | 1,581.40 | -0.86(-0.05%) | 34282 |

| AMERICAN INTERNATIONAL GROUP | AIG | 56.38 | 0.07(0.12%) | 193 |

| Apple Inc. | AAPL | 175.59 | 6.49(3.84%) | 1999979 |

| AT&T Inc | T | 32.61 | 0.07(0.22%) | 25538 |

| Barrick Gold Corporation, NYSE | ABX | 13.47 | 0.03(0.22%) | 3730 |

| Boeing Co | BA | 329.01 | -0.53(-0.16%) | 4624 |

| Caterpillar Inc | CAT | 144.43 | 0.01(0.01%) | 1853 |

| Chevron Corp | CVX | 124.87 | 0.01(0.01%) | 4206 |

| Cisco Systems Inc | CSCO | 44.76 | -0.07(-0.16%) | 66902 |

| Citigroup Inc., NYSE | C | 68.12 | -0.13(-0.19%) | 5671 |

| Deere & Company, NYSE | DE | 135.6 | 0.23(0.17%) | 318 |

| Facebook, Inc. | FB | 173.8 | -0.06(-0.03%) | 77832 |

| Ford Motor Co. | F | 11.28 | 0.02(0.18%) | 33358 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 15.19 | 0.24(1.61%) | 45733 |

| General Electric Co | GE | 14.13 | 0.08(0.57%) | 102630 |

| General Motors Company, NYSE | GM | 36.57 | 0.15(0.41%) | 10903 |

| Goldman Sachs | GS | 235.87 | -0.80(-0.34%) | 3386 |

| Google Inc. | GOOG | 1,033.55 | -3.76(-0.36%) | 3083 |

| Home Depot Inc | HD | 184.73 | 0.10(0.05%) | 936 |

| Intel Corp | INTC | 53.11 | -0.22(-0.41%) | 76604 |

| International Business Machines Co... | IBM | 144.82 | -0.18(-0.12%) | 3416 |

| Johnson & Johnson | JNJ | 126.25 | 0.24(0.19%) | 2587 |

| JPMorgan Chase and Co | JPM | 108.56 | -0.22(-0.20%) | 6380 |

| McDonald's Corp | MCD | 163.3 | -0.14(-0.09%) | 2006 |

| Merck & Co Inc | MRK | 57.95 | -0.03(-0.05%) | 2422 |

| Microsoft Corp | MSFT | 94.75 | -0.25(-0.26%) | 67941 |

| Nike | NKE | 67.88 | -0.22(-0.32%) | 2917 |

| Pfizer Inc | PFE | 35.35 | -0.05(-0.14%) | 9514 |

| Procter & Gamble Co | PG | 72.05 | 0.09(0.13%) | 9868 |

| Starbucks Corporation, NASDAQ | SBUX | 57.93 | -0.20(-0.34%) | 4003 |

| Tesla Motors, Inc., NASDAQ | TSLA | 299.1 | -0.82(-0.27%) | 32345 |

| The Coca-Cola Co | KO | 42.5 | -0.09(-0.21%) | 3936 |

| Twitter, Inc., NYSE | TWTR | 30.02 | -0.28(-0.92%) | 54433 |

| United Technologies Corp | UTX | 119.19 | 0.23(0.19%) | 3344 |

| Verizon Communications Inc | VZ | 48.59 | -0.23(-0.47%) | 1923 |

| Visa | V | 128.34 | 0.83(0.65%) | 41077 |

| Wal-Mart Stores Inc | WMT | 87.46 | 0.05(0.06%) | 2388 |

| Walt Disney Co | DIS | 100.31 | 0.25(0.25%) | 3818 |

| Yandex N.V., NASDAQ | YNDX | 33.15 | -0.48(-1.43%) | 14989 |

Alcoa (AA) initiated with a Buy at Jefferies; target $65

Apple (AAPL) target lowered to $204 from $210 at Maxim Group

U.S private sector employment increased by 204,000 jobs from March to April according to the April ADP National Employment Report.

"The labor market continues to maintain a steady pace of strong job growth with little sign of a slowdown," said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "However, as the labor pool tightens it will become increasingly difficult for employers to find skilled talent. Job gains in the highskilled professional and business services industry accounted for more than half of all jobs added this month. The construction industry, which also relies on skilled labor, continued its six month trend of steady job gains as well." Mark Zandi, chief economist of Moody's Analytics, said, "Despite rising trade tensions, more volatile financial markets, and poor weather, businesses are adding a robust more than 200,000 jobs per month. At this pace, unemployment will soon be in the threes, which is rarified and risky territory, as the economy threatens to overheat."

MasterCard (MA) reported Q1 FY 2018 earnings of $1.50 per share (versus $1.00 in Q1 FY 2017), beating analysts' consensus estimate of $1.24.

The company's quarterly revenues amounted to $3.580 bln (+30,9% y/y), beating analysts' consensus estimate of $3.255 bln.

MA rose to $187.00 (+3.74%) in pre-market trading.

Apple (AAPL) reported Q2 FY 2018 earnings of $2.73 per share (versus $2.10 in Q2 FY 2017), beating analysts' consensus estimate of $2.68.

The company's quarterly revenues amounted to $61.137 bln (+15.6% y/y), generally in-line with analysts' consensus estimate of $60.940 bln.

The company said its iPhone shipments amounted to 52.2 mln in Q2 versus analysts' consensus estimate of 52 mln and 50.8 mln in the corresponding period of the previous year.

Apple also issued upside guidance for Q3, projecting revenues of $51.5-53.5 bln (versus analysts' consensus estimate of $51.51 bln) and gross margins of 38.0-38.5% (versus analysts' consensus estimate of 38.4% and the companies year-ago result of 38.5%).

In addition, the company decided to add $100 bln to share repurchase and raise dividend 16% to $0.73/share.

AAPL rose to $174.75 (+3.34%) in pre-market trading.

The euro area (EA19) seasonally-adjusted unemployment rate was 8.5% in March 2018, stable compared with February 2018 and down from 9.4% in March 2017. This is the lowest rate recorded in the euro area since December 2008. The EU28 unemployment rate was 7.1% in March 2018, stable compared with February 2018 and down from 7.9% in March 2017. This is the lowest rate recorded in the EU28 since September 2008.

Seasonally adjusted GDP rose by 0.4% in both the euro area (EA19) and in the EU28 during the first quarter of 2018, compared with the previous quarter, according to a preliminary flash estimate published by Eurostat, the statistical office of the European Union. In the fourth quarter of 2017, GDP had grown by 0.7% in the euro area and by 0.6% in the EU28. Compared with the same quarter of the previous year, seasonally adjusted GDP rose by 2.5% in the euro area and by 2.4% in the EU28 in the first quarter of 2018, after +2.8% and +2.7% respectively in the previous quarter.

April data indicated a moderate recovery in construction output following the weather-related disruptions seen during March. House building was the main category of activity to experience robust growth in April. However, there were signs that underlying demand across the construction sector remained subdued, with total new work rising only marginally in April. The increase in new business was the first recorded by the survey so far in 2018.

At 52.5 in April, the seasonally adjusted IHS Markit/CIPS UK Construction Purchasing Managers' Index picked up sharply from the 20-month low seen in March (47.0). The latest reading was the highest since November 2017 and signalled a moderate expansion of overall construction output.

The start of the second quarter saw a further slowing in the rate of growth in the eurozone manufacturing sector. The final IHS Markit Eurozone Manufacturing PMI fell to a 13-month low of 56.2 in April, down from 56.6 in March and slightly above the earlier flash estimate of 56.0. Although still signalling a solid rate of expansion, the upturn has lost noticeable momentum since the PMI hit a record high in December 2017.

Germany's manufacturing sector made a solid start to the second quarter, with output rising markedly and at a quicker pace than in March. However, the rate of production growth remained well below the highs seen at the turn of the year, and both new order inflows and job creation continued to wane from their recent elevated levels.

The headline IHS Markit/BME Germany Manufacturing PMI - a single-figure snapshot of the performance of the manufacturing economy - dipped to 58.1 in April, down fractionally from 58.2 in March and its lowest reading for nine months.

-

We are convinced there remains untapped potential in the economy, including participation in labor force by youth

-

What really keeps me awake at night is risk of cyber event

-

Australia's rating is underpinned by strong governance, high income levels, and a track record of macroeconomic stability

-

Monetary policy likely to remain accommodative,supportive of growth over 2 years in absence of wage growth or inflationary pressures

Although output rose at a slightly quicker rate, new order growth slowed amid a renewed fall in new export work. Consequently, purchasing activity rose only modestly, while firms noted higher inventories of both inputs and finished items.

The headline seasonally adjusted Purchasing Managers' Index registered 51.1 in April, up fractionally from 51.0 in March. Operating conditions have now strengthened in each of the past 11 months, though the pace of improvement was only marginal.

Although the rate of expansion in output regained some ground, slower increases were seen in new orders and employment. That said, the sector continued to maintain solid growth during the month.

There were also signs of softening inflationary pressures, with both input costs and output prices rising at weaker rates. The headline IHS Markit Spain Manufacturing PMI posted 54.4 in April, thereby signalling a solid improvement in the health of the sector. That said, down from 54.8 in March, the PMI signalled a weaker strengthening of business conditions, and one that was the slowest since September 2017.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2121 (1546)

$1.2090 (1158)

$1.2068 (637)

Price at time of writing this review: $1.2006

Support levels (open interest**, contracts):

$1.1932 (3115)

$1.1890 (1045)

$1.1845 (2559)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date May, 4 is 96853 contracts (according to data from May, 1) with the maximum number of contracts with strike price $1,2000 (5108);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3808 (244)

$1.3765 (922)

$1.3699 (1439)

Price at time of writing this review: $1.3611

Support levels (open interest**, contracts):

$1.3532 (685)

$1.3490 (438)

$1.3445 (211)

Comments:

- Overall open interest on the CALL options with the expiration date May, 4 is 25295 contracts, with the maximum number of contracts with strike price $1,4400 (3253);

- Overall open interest on the PUT options with the expiration date May, 4 is 27708 contracts, with the maximum number of contracts with strike price $1,3700 (2234);

- The ratio of PUT/CALL was 1.10 versus 1.13 from the previous trading day according to data from May, 1.

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

European stocks posted a modest loss on Tuesday, as most of the region's markets were closed for the May Day holiday. The Stoxx Europe 600 index SXXP, -0.08% snapped a three-day win streak and ended marginally lower, down about 0.1% at 385.03, after finishing Monday trade up 0.2%.

U.S. stocks closed mostly higher on Tuesday, as a sharp rally in technology stocks helped the S&P 500 and the Nasdaq shake off an early decline. However, the Dow fell for a third straight session as caution remained high ahead of the conclusion of a Federal Reserve policy meeting and fresh developments in global trade.

Asia-Pacific stock moves were muted in early trading Wednesday, after most overseas benchmarks saw little change the previous day. Most markets in the region were closed Tuesday for the Labor Day holiday, and Japan will be closed Thursday and Friday.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers