- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 01-08-2018

| Raw materials | Closing price | % change |

| Oil | 67.85 | -1.32% |

| Gold | 1,224.50 | -0.74% |

| Index | Change items | Closing price | % change |

| Nikkei | +192.98 | 22746.70 | +0.86% |

| TOPIX | +16.47 | 1769.76 | +0.94% |

| CSI 300 | -70.27 | 3447.39 | -2.00% |

| KOSPI | +11.81 | 2307.07 | +0.51% |

| FTSE 100 | -95.85 | 7652.91 | -1.24% |

| DAX | -68.45 | 12737.05 | -0.53% |

| CAC 40 | -12.93 | 5498.37 | -0.23% |

| DJIA | -81.37 | 25333.82 | -0.32% |

| S&P 500 | -2.93 | 2813.36 | -0.10% |

| NASDAQ | +35.50 | 7707.29 | +0.46% |

| Pare | Closed | % change |

| EUR/USD | $1,1659 | -0,23% |

| GBP/USD | $1,3123 | +0,05% |

| USD/CHF | Chf0,99189 | +0,19% |

| USD/JPY | Y111,68 | -0,13% |

| EUR/JPY | Y130,22 | -0,37% |

| GBP/JPY | Y146,582 | -0,07% |

| AUD/USD | $0,7404 | -0,29% |

| NZD/USD | $0,6792 | -0,32% |

| USD/CAD | C$1,30007 | -0,08% |

Major US stock indexes finished trading mostly in the red, losing almost all the positions earned after a strong report from Apple caused the growth of the high-tech sector. Pressure on the market raised concerns about additional US duties on Chinese goods, as well as growth in yields on US government bonds.

The focus of investors' attention was also the outcome of the Fed meeting. As expected, the Fed left the range for interest rates unchanged, sounding at the same time a positive assessment of the economy, which signaled a probable increase in rates at the next meeting. "Economic activity is growing at a strong pace," the Fed said in a statement. She also called job growth "strong" and noted "strong" growth in household investment and expenditure. In general, the Fed has used the word "strong" or its synonyms six times in its statement to describe the state of the economy and the situation in the labor market.

In addition, according to a report published by the Institute for Supply Management (ISM), activity in the US manufacturing sector deteriorated sharply in July. The PMI index for the manufacturing sector fell to 58.1 points against 60.2 points in June. Analysts had expected that the figure would drop only to 59.5 points.

However, construction costs in the US recorded the largest drop in more than a year in June, as investments in both private and public projects declined, but expenses for the previous months were revised upward. The Ministry of Trade reported that in June construction costs fell by 1.1%, which is the biggest decline since April 2017. Meanwhile, the growth rates of expenditures for May were revised to + 1.3% from + 0.4%. Expenses for April were also revised towards improvement - to + 1.7% from + 0.9%. Economists predicted that in June construction costs would grow by only 0.3%. Meanwhile, in annual terms, construction costs increased in June by 6.1%.

Most of the components of DOW finished trading in the red (19 of 30). Outsider were shares of Caterpillar Inc. (CAT, -3.73%). The leader of growth was the shares of Apple Inc. (AAPL, + 5.96%).

Most S & P sectors recorded a decline. The largest drop was shown by the sector of industrial goods (-1.2%). The consumer goods sector grew most (+ 0.6%).

At closing:

Dow 25,333.82 -81.37 -0.32%

S&P 500 2,813.36 -2.93 -0.10%

Nasdaq 100 7,707.29 +35.50 +0.46%

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.8 million barrels from the previous week. At 408.7 million barrels, U.S. crude oil inventories are about 1% below the five year average for this time of year.

Total motor gasoline inventories decreased by 2.5 million barrels last week and are about 3% above the five year average for this time of year. Finished gasoline inventories increased while blending components inventories decreased last week.

Distillate fuel inventories increased by 3.0 million barrels last week and are about 11% below the five year average for this time of year. Propane/propylene inventories increased by 1.8 million barrels last week and are about 12% below the five year average for this time of year. Total commercial petroleum inventories increased last week by 10.6 million barrels last week.

The July Manufacturing PMI registered 58.1 percent, a decrease of 2.1 percentage points from the June reading of 60.2 percent. The New Orders Index registered 60.2 percent, a decrease of 3.3 percentage points from the June reading of 63.5 percent.

"Comments from the panel reflect continued expanding business strength. Demand remains strong, with the New Orders Index at 60 percent or above for the 15th straight month, and the Customers' Inventories Index remaining low. The Backlog of Orders Index continued to expand, but at lower levels. Production and employment continues to expand in spite of labor and material shortages. Inputs - expressed as supplier deliveries, inventories and imports - had expansion increases, due primarily to negative supply chain issues, but at easing levels compared to the prior month. Lead-time extensions, steel and aluminum disruptions, supplier labor issues, and transportation difficulties continue" - Timothy R. Fiore Chair of the Institute for Supply Management.

U.S. stock-index futures were flat on Wednesday, as Apple's (AAPL) upbeat report was outweighed by increased concerns of escalation trade tensions between the U.S. and China, following news the U.S. president is considering raising its planned tariffs on $200 billion in Chinese imports to 25 percent from initially proposed 10 percent. Investors also remained cautious ahead of the announcement of the Fed's decision on monetary policy later today.

Global Stocks:

| Index/commodity | Last | Today's Change, points | Today's Change, % |

| Nikkei | 22,746.70 | +192.98 | +0.86% |

| Hang Seng | 28,340.74 | -242.27 | -0.85% |

| Shanghai | 2,824.21 | -52.19 | -1.81% |

| S&P/ASX | 6,275.70 | -4.50 | -0.07% |

| FTSE | 7,656.07 | -92.69 | -1.20% |

| CAC | 5,507.96 | -3.34 | -0.06% |

| DAX | 12,740.88 | -64.62 | -0.50% |

| Crude | $67.68 | | -1.57% |

| Gold | $1,230.10 | | -0.28% |

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 211.99 | -0.33(-0.16%) | 660 |

| ALCOA INC. | AA | 42.93 | -0.34(-0.79%) | 500 |

| Amazon.com Inc., NASDAQ | AMZN | 1,784.85 | 7.41(0.42%) | 28825 |

| AMERICAN INTERNATIONAL GROUP | AIG | 56.17 | 0.96(1.74%) | 981 |

| Apple Inc. | AAPL | 198.02 | 7.73(4.06%) | 1188450 |

| Boeing Co | BA | 354.1 | -2.20(-0.62%) | 1748 |

| Caterpillar Inc | CAT | 142.94 | -0.86(-0.60%) | 12775 |

| Chevron Corp | CVX | 125.5 | -0.77(-0.61%) | 2044 |

| Cisco Systems Inc | CSCO | 42.18 | -0.11(-0.26%) | 16226 |

| Citigroup Inc., NYSE | C | 72.28 | 0.39(0.54%) | 8656 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 16.03 | -0.47(-2.85%) | 69829 |

| General Motors Company, NYSE | GM | 38 | 0.09(0.24%) | 826 |

| Goldman Sachs | GS | 238.18 | 0.75(0.32%) | 3204 |

| Google Inc. | GOOG | 1,228.50 | 11.24(0.92%) | 17811 |

| Google Inc. | GOOG | 1,228.50 | 11.24(0.92%) | 17811 |

| Home Depot Inc | HD | 197.42 | -0.10(-0.05%) | 1506 |

| Intel Corp | INTC | 47.99 | -0.11(-0.23%) | 43528 |

| International Business Machines Co... | IBM | 144.68 | -0.25(-0.17%) | 553 |

| Merck & Co Inc | MRK | 65.36 | -0.51(-0.77%) | 618 |

| Microsoft Corp | MSFT | 105.85 | -0.23(-0.22%) | 70019 |

| Pfizer Inc | PFE | 39.7 | -0.23(-0.58%) | 7162 |

| Starbucks Corporation, NASDAQ | SBUX | 52.25 | -0.14(-0.27%) | 3228 |

| Tesla Motors, Inc., NASDAQ | TSLA | 298 | -0.14(-0.05%) | 19638 |

| The Coca-Cola Co | KO | 46.45 | -0.18(-0.39%) | 875 |

| The Coca-Cola Co | KO | 46.45 | -0.18(-0.39%) | 875 |

| Verizon Communications Inc | VZ | 51.75 | 0.11(0.21%) | 2527 |

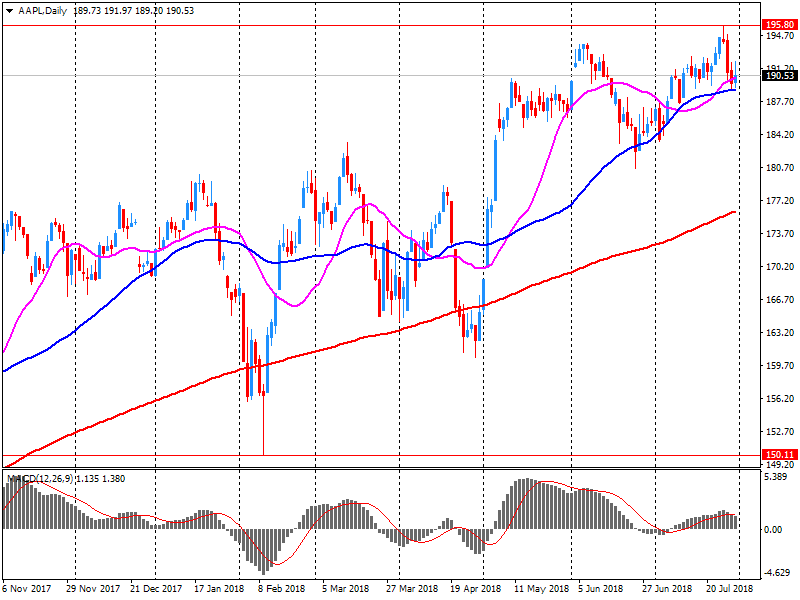

Apple (AAPL) target raised to $220 from $210 at Needham

Private sector employment increased by 219,000 jobs from June to July according to the July ADP National Employment Report.

"The labor market is on a roll with no signs of a slowdown in sight," said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "Nearly every industry posted strong gains and small business hiring picked up." Mark Zandi, chief economist of Moody's Analytics, said, "The job market is booming, impacted by the deficit-financed tax cuts and increases in government spending. Tariffs have yet to materially impact jobs, but the multinational companies shed jobs last month, signaling the threat."

Apple (AAPL) reported Q3 FY 2018 earnings of $2.34 per share (versus $1.67 in Q3 FY 2017), beating analysts' consensus estimate of $2.18.

The company's quarterly revenues amounted to $53.265 bln (+17.3% y/y), beating analysts' consensus estimate of $52.430 bln.

The company also issued upside guidance for Q4, projecting revenues of $60-62 bln versus analysts' consensus estimate of $59.4 bln.

AAPL rose to $198.44 (+4.28%) in pre-market trading.

July saw slower rates of expansion in both output and new orders, as weaker growth of new work from domestic sources offset a stronger increase in new export orders. Price pressures also remained elevated as a strong increase in average input costs led to the steepest rise in selling prices since February.

The seasonally adjusted IHS Markit/CIPS Purchasing Managers' Index fell to a three-month low of 54.0 in July, down from 54.3 in June and well below the highs achieved around the turn of the year. That said, the PMI remains comfortably above its long-run average of 51.8.

Although the final IHS Markit Eurozone Manufacturing PMI posted 55.1 in July, unchanged from the earlier flash estimate, this was only a minor recovery from June's 18-month low of 54.9 and over five points below the record high registered at the end of 2017.

Sector data signalled that business conditions improved across the consumer, intermediate and investment goods sectors, with mild growth upticks signalled in the latter two. Similar to the trend at the all-manufacturing level, rates of expansion were weaker than at the turn of the year in all three subindustries.

The headline IHS Markit/BME Germany Manufacturing PMI - a single-figure snapshot of the performance of the manufacturing economy - posted 56.9 in July, up from 55.9 in June. The start of the third quarter indicated a sharp improvement in operating conditions, with manufacturing growth regaining momentum.

Commenting on the final IHS Markit/BME Germany Manufacturing PMI survey data, Sian Jones, Economist at IHS Markit said: "The beginning of the second half of the year brought a faster rise in manufacturing growth among German manufacturers. Following a dip in overall performance in June, the upturn in output and new orders strengthened. That said, the increase in production continued to outpace that of new orders as firms expanded their efforts to clear backlogs. "Although slightly weaker than June, employment growth continued to grow sharply, with greater production requirements a key factor behind sustained job creation. Panellists also reported stronger optimism towards future output growth, the most robust since April".

Business conditions in the Spanish manufacturing sector improved at a moderated pace in July as growth continued to lose momentum from earlier in 2018. Although output increased at a slightly faster pace than in June, rates of expansion in new orders, employment and purchasing activity all slowed. Meanwhile, the rate of input cost inflation accelerated again, with higher aluminium prices widely mentioned. This fed through to a further solid increase in output prices.

The headline IHS Markit Spain Manufacturing PMI dropped to 52.9 in July from 53.4 in June. Although continuing to signal a solid strengthening of the health of the sector at the start of the third quarter of the year, the PMI pointed to the weakest improvement since August last year

EUR/USD

Resistance levels (open interest**, contracts)

$1.1788 (4487)

$1.1769 (2534)

$1.1754 (792)

Price at time of writing this review: $1.1680

Support levels (open interest**, contracts):

$1.1642 (3542)

$1.1596 (3960)

$1.1549 (2695)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date August, 13 is 90195 contracts (according to data from July, 31) with the maximum number of contracts with strike price $1,1850 (5321);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3267 (1094)

$1.3206 (661)

$1.3175 (304)

Price at time of writing this review: $1.3112

Support levels (open interest**, contracts):

$1.3074 (2512)

$1.3035 (2266)

$1.2992 (1564)

Comments:

- Overall open interest on the CALL options with the expiration date August, 13 is 24442 contracts, with the maximum number of contracts with strike price $1,3600 (3206);

- Overall open interest on the PUT options with the expiration date August, 13 is 28934 contracts, with the maximum number of contracts with strike price $1,3100 (2512);

- The ratio of PUT/CALL was 1.18 versus 1.18 from the previous trading day according to data from July, 31.

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Annual house price growth picks up to 2.5%

-

Prices rose 0.6% month-on-month

-

Any rate hike likely to have a modest impact

Commenting on the figures, Robert Gardner, Nationwide's Chief Economist, said: "There was a slight uptick in annual house price growth in July to 2.5%, from 2.0% in June. Nonetheless, annual house price growth remains within the fairly narrow range of c2-3% which has prevailed over the past 12 months, suggesting little change in the balance between demand and supply in the market. "Looking further ahead, much will depend on how broader economic conditions evolve, especially in the labour market, but also with respect to interest rates".

The headline Nikkei Japan Manufacturing Purchasing Managers' Idex declined to 52.3 in July, from 53.0 in June, thereby pointing to a softer rate of improvement in manufacturing sector business conditions.

Commenting on the Japanese Manufacturing PMI survey data, Joe Hayes, Economist at IHS Markit, which compiles the survey, said: "Latest survey data signalled a slowdown to manufacturing sector growth at the beginning of Q3. Output growth eased and there was a noticeable softening of demand, while export sales failed to record any upswing for a second month running. "There was also evidence that supply-side constraints were beginning to bite harder. Employment growth slipped and was weaker than rates seen earlier in the year, meanwhile delivery times for inputs lengthened to the greatest extent in over seven years".

"Border Security is National Security, and National Security is the long-term viability of our Country. A Government Shutdown is a very small price to pay for a safe and Prosperous America!"

-

Unemployment rate rose to 4.5 percent.

-

Underutilisation rate rose to 12.0 percent.

-

Employment rate was unchanged at 67.7 percent.

-

Filled jobs rose 0.8 percent.

-

Average ordinary time hourly earnings increased to $31.00.

-

Annual wage inflation increased 1.9 percent.

-

The unemployment rate for men rose to 4.3 percent (up 0.3 percentage points), while for women it fell to 4.7 percent (down 0.2 percentage points).

-

The underutilisation rate for men rose to 10.0 percent (up 0.6 percentage points), while for women, it fell to 14.3 percent (down 0.3 percentage points).

Operating conditions across China's manufacturing sector improved at the slowest pace for eight months in July, with output and new business both expanding at softer rates. Notably, new export orders fell at the steepest pace for 25 months. A further reduction in staffing levels meanwhile contributed to a sustained increase in backlogs of work. On the price front, the rate of input cost inflation weakened since June, but remained elevated, while output charges rose only modestly. Optimism towards the year ahead remained relatively subdued amid concerns surrounding tough market conditions, strict environmental policies and the potential impact of the US-China trade war.

The headline seasonally adjusted Purchasing Managers' Index fell from 51.0 in June to 50.8 in July. Although still above the neutral 50.0 mark, the latest figure highlighted the slowest improvement in the health of the sector since November 2017.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers