- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 24-03-2011.

The Nasdaq 100 has extended its rally to a 1.7% gain amid leadership from Research In Motion (RIMM 64.30, +2.18), which has pushed through its 50-day simple moving average to set a fresh session high ahead of its earnings report tonight. Also on the earnings calendar, Accenture (ACN 51.88, +1.21), Oracle (ORCL 32.11, +0.70), and Darden Restaurants (DRI 47.70, +0.43) are scheduled to report tonight.

Pressure against Treasuries over the past two sessions has sent the yield on the benchmark 10-year Note about 10 basis points higher, but it has yet to push past 3.40%. Still, the Note's yield stands at its highest level in more than a week.

Meanwhile, oil prices have come under increased pressure in recent trade. In turn, the energy component now trades at slightly less than $105 per barrel, which is a fresh session low, with a 0.8% loss.

EUR/USD

Offers: $1.4180, $1.4215/20, $1.4240/50, $1.4275

Bids: $1.4050/40, $1.4035, $1.4020/10

USD/JPY

Offers: Y81.10/15, Y81.30/35, Y81.75/80, Y82.00

Bids: Y80.50/55, Y80.10/15

A broad bid in the early going has helped the S&P 500 move a couple of points past the 1300 line for the first time in over a week. The benchmark index is having difficulty extending its advance, though.

Financials are a source of weakness for the second straight session. They are collectively down 0.2% and represent the only major sector that has failed to find higher ground this morning.

As a group, consumer discretionary stocks are sporting some of the strongest gains. The sector is up an enviable 0.7% as Best Buy (BBY 32.21, +0.36) bounces following a better-than-expected earnings report.

U.S. stocks were headed for another day of modest gains early Thursday, as investors mulled over the latest jobless claims data.

Weekly filings for first-time unemployment benefits were roughly in line with expectations, but stayed below 400,000 and continuing claims remained low as well.

Though concerns about global events are far from over, and more downbeat news came from Europe Thursday morning, U.S. futures held their gains.

Portugal's Prime Minister, Jose Socrates, resigned early Wednesday after parliament rejected his administration's latest proposal for austerity measures, reports said. The plan is aimed at avoiding a bailout.

Meanwhile, ratings agency Moody's downgraded its debt ratings of 30 Spanish banks. Moody's added that the outlook remained weak, and the banks "show little sign of strengthening materially in the foreseeable future."

Economy: Before the start of trade, the Commerce Department reported durable goods orders fell 0.9% in February, compared with a 3.6% rise posted in January. Economists were expecting a 1.1% rise in February.

Companies: Shares of Red Hat (RHT), the largest seller of Linux software, surged 13% in premarket trade. The company reported a 43% increase in its fourth-quarter profit late Wednesday.

Electronics retailer Best Buy (BBY) reported profit and sales that beat forecasts. Shares rose 3.9% premarket.

Walgreen Co. (WAG) said early Thursday it will buy online retailer Drugstore.com (DSCM) for $409 million.

After the bell, software giant Oracle (ORCL) and smartphone maker Research in Motion (RIMM) will report. Analysts expect RIM to have earned $1.76 a share while Oracle is expected to post a 50-cents-a-share profit.

World markets:

Oil for May delivery gained 74 cents, or 0.7%, to $106.49 a barrel.

Gold futures for April delivery rose $2.50, or 0.2%, to $1,440.50 an ounce. Gold closed at a record high in the previous session, settling at $1,438 an ounce.

The price on the benchmark 10-year U.S. Treasury fell, pushing the yield up to 3.36% from 3.26% late Wednesday.

Through resistance at Y114.25 to a high of Y114.48 as euro-dollar firms and dollar-yen heads higher on BOJ fears. Further resistance seen at Y114.60 and Y115.00.

Data released

08:28 Germany PMI (March) flash 60.9 62.0 62.7

08:28 Germany PMI services (March) flash 60.1 58.4 58.6

08:58 EU(17) PMI (March) flash 57.7 58.2 59.0

08:58 EU(17) PMI services (March) flash 56.9 56.3 56.8

09:00 Italy Consumer confidence (March) 105.2 - 106.3 (106.4)

09:30 UK Retail sales (February) -0.8% -0.5% 1.9%

09:30 UK Retail sales (February) Y/Y 1.3% 2.4% 5.3%

The euro appreciated against the dollar as speculation that the European Central Bank is poised to raise borrowing costs outweighed concern that the fiscal crisis in the region’s most indebted nations is deepening.

The euro slipped earlier today as Moody’s Investors Service downgraded 30 Spanish banks, and tumbled late yesterday after Portugal’s prime minister resigned. The ECB on March 3 said “strong vigilance” is warranted on inflation.

“The euro shrugs off these negatives because the market is focused on the ECB raising rates,” said Jeremy Hale at Citigroup. “It’s expectations about rates that are driving everything.”

The ECB will announce its next monetary policy decision on April 7. Its refinancing rate is currently at a record low of 1%.

ECB council member Erkki Liikanen today said the bank’s stance ensures that temporary inflation pressures don’t fuel broader wage and price increases.

EUR/USD continues to hold higher afger falling to session lows around $1.4050. Currently rate trades near $1.4145.

GBP/USD fell from $1.6260 tо $1.6142. Bids helped the rate to recover to $1.6180.

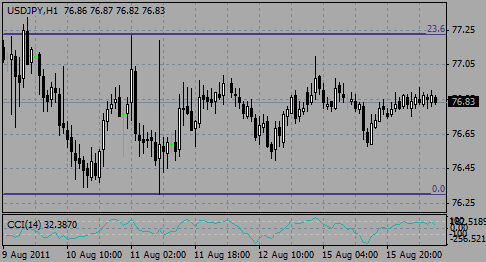

USD/JPY holds within the Y80.70/Y81.10 range.

Jobless claims is scheduled to release at 12:30 GMT.

The focus will be on Durable goods orders at 12:30 GMT. Analysts predict orders rose 3.2% in Feb after +1.0% in Jan.

EUR/JPY passed through resistance at Y114.25 to a high of Y114.48. Further resistance seen at Y114.60 and Y115.00. Cross trades Y114.40/43.

- Hard to say if we'll have food shock like 3 yrs ago

- Happy italy,spain taking measures to stabilize econs

- Monpol can't affect commodities; must consider them

- ECB balance sheet strong

- See downside risks,uncertainty on japan

- Must remember libya oil small share of global volume

- Too early to discuss ECB succession

- Hard to say if we'll have food shock like 3 yrs ago

- Happy italy,spain taking measures to stabilize econs

- Monpol can't affect commodities; must consider them

- ECB balance sheet strong

- See downside risks,uncertainty on japan

- Must remember libya oil small share of global volume

- Too early to discuss ECB succession

Euro falls versus dollar, yen after Moody's cuts ratings on Spanish banks.

Focus is still on Portugual and now there is an increased risk of S&P & Fitch downgrading Portugual's sovereign rating following the resignation of Prime Minister Jose Socrates last night after rejection of new austerity measures by opposition parties.

Meanwhile, ECB's Stark, writing in WSJ, says recent events in Japan, Mid-East need to be considered by ECB, but cannot expect a knee-jerk reaction to be easing the monetary policy to all events. Stark also noted the ECB cannot keep interest rates too low for too long. He adds observers correctly read the ECB's dropping of "rates appropriate".

Canada’s dollar fluctuated as crude oil, the nation’s biggest export, reached a two-week high.

EUR/USD printed session high on $1.414 before retreated to strong support at $1.4050. Rate's losses were capped here by bids, that helped the rate to recover to $1.4075.

GBP/USD fell from $1.6264 to the lows below the figure.

USD/JPY holds within the Y80.70/Y81.10 range.

UK' retail sales is due to come at 09:30 GMT. Madian forecast is for 1.9% rise after -0.5% month earlier.

Jubless claims is scheduled to release at 12:30 GMT.

The focus will be on Durable goods orders at 12:30 GMT. Analysts predict orders rose 3.2% in Feb after +1.0% in Jan.

Cable fell 30 pips following weak UK retail sales data. GBP/USD dropped from just above $1.6200 to $1.6170 on release of weaker than forecast UK retail sales. Second round selling now extends move to $1.6164, but again rate seen meeting willing buyers into dips. Later rate fell to the lows around $1.6140.

Data released

09:30 UK BoE meeting minutes (09-10.03)

10:00 EU(17) Industrial orders (February) 0.1% 1.2% 2.7 (2.1)%

10:00 EU(17) Industrial orders (February) Y/Y 20.9% 21.5% 19.2 (18.5)%

14:00 USA New home sales (February) 250K 290K 301 (284)K

23:50 Japan Trade balance (February) unadjusted, trln 0.654 0.897 -0.471

The euro slumped against most of its major counterparts as Portugal began debating a budget that may lead the government to fall and European leaders pushed back a decision on funding a regional bailout mechanism.

The 17-nation currency fell for a second day against the dollar before a Portuguese vote that may force the nation to an early election and bailout and reports the expansion of the European Union European Financial Stability Facility will not be decided until June.

The yen strengthened against most of its major counterparts as Luxembourg Prime Minister Jean-Claude Juncker said Europe, the U.S. and the Group of Seven are “ready” to act to curb the currency’s rise.

Demand for Japanese debt rose as radiation levels at Japan’s Fukushima Dai-Ichi nuclear power plant hampered efforts to repair reactors.

The yen rose against most major currencies even after Jean- Claude Juncker said the Japanese currency is “slowly moving in the wrong direction”. The G-7 nations intervened March 18 to bring the currency down from a postwar high.

Juncker also said March 21 his “personal guess” is that the EFSF would be decided in June and would increase guarantees. The decision won’t be made by the end of this week’s meeting of policy makers, Reuters reported citing a draft document.

“Portugal has been on the radar screen, but the statement that was most damaging is that the EFSF was put off to the end of June,” said Steven Englander at Citigroup Inc.. “Everything we heard and seen for the last three months was telling us that everything would be wrapped up this weekend and now it’s not.”

The pound fell against all its major counterparts after the Bank of England minutes showed policy makers voted 6-3 to keep rates steady on March 10.

Chancellor of the Exchequer George Osborne said the British economy will more grow more slowly this year than previously forecast.

The Office for Budget Responsibility predicts annual growth in 2011 of 1.7 percent, down from the 2.1 percent forecast in November, Osborne said.

EUR/USD initially rose to $1.4213, but failed to hold above the figure and retreated to lows around $1.4074. Rate's attempts to recover were short-lived.

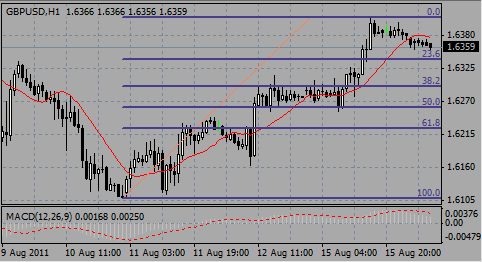

GBP/USD printed high on $1.6380, but declined after МРС's minutes release. Session lows were matched at $1.6212. Later rate recovered to $1.6270.

USD/JPY continued to hold within the narrow range, limited by Y80.70/Y81.10.

UK' retail sales is due to come at 09:30 GMT. Madian forecast is for 1.9% rise after -0.5% month earlier.

Jubless claims is scheduled to release at 12:30 GMT.

The focus will be on Durable goods orders at 12:30 GMT. Analysts predict orders rose 3.2% in Feb after +1.0% in Jan.

Majors close

Nikkei (-1.7%) 9449.47

Topix (-0.8%) 861.10

DAX +23.48 (+0.35%) 6804

CAC +21.02 (+0.54%) 3914

FTSE-100 +33.17 (+0.58%) 5796

Dow +67.39 (+0.56%) 12086.02

Nasdaq +14.43 (+0.54%) 2698.30

S&P500 +3.77 (+0.29%) 1297.54

Oil +0.54 $105.51

10-Years +0.02 3.35%

Japanese stocks fell for the first time in three days as engineers struggled to connect power to a crippled nuclear reactor and Tokyo officials advised against giving tap water to infants after finding traces of radioactive iodine.

Tokyo Electric Power Co., the owner of the damaged plant, sank 4.5%.

A series of earthquakes struck this morning near the Fukushima plant, starting with a magnitude 6.0 temblor at 7:12 a.m. local time. Quakes of magnitude 4.1, 5.8, 4.9 and 4.3 followed as of 8:03 a.m..

Toyota Motor Corp., the world’s largest carmaker, dropped 1.2% after saying it will halt domestic production through March 26.

Honda Motor Co. fell 1.8% after saying it will suspend production at three Japanese plants until at least March 27.

JTekt Corp., a car-parts supplier, slumped 6.1%.

Daihatsu Motor Co. lost 1.5% after extending a production halt until March 24.

Earthquakes early this morning also damped sentiment, and declines accelerated in the final minutes of trading following the warning on tap water.

On Wednesday, the Japanese government said the quake would cost the nation $300 billion - more than double the cost of the Kobe quake in 1995, according to published reports.

European stocks rose for the fourth time in five days as mining companies climbed with metal prices, outweighing an unexpected drop in U.S. new-home sales and speculation that Portugal’s budget vote may trigger a bailout.

Rio Tinto Group surged 2.9%, leading basic-resource producers higher.

Xstrata Plc (XTA) gained 3.5%. Copper, lead, nickel and tin climbed on the London Metal Exchange.

Eurasian Natural Resources Corp. rallied 3.5% as profit doubled.

Inditex SA (ITX) gained 6% after world’s largest clothing retailer reported earnings that topped estimates.

J Sainsbury Plc (SBRY) sank 5.4% as sales growth slowed.

Minutes of the Bank of England’s March 10 meeting published today showed policy makers saw “merit in waiting” to examine the effect of higher oil prices on inflation, boosting speculation it will leave interest rates on hold for longer. Policy makers voted 6-3 to keep interest rates at a record low.

U.S. stocks finished higher Wednesday, thanks to a late-day advance, as investors shrugged off jitters about turmoil in the Middle East and Japan's nuclear issues.

The Dow Jones industrial average (INDU) closed 67 points higher, or 0.6%, led by a 3% jump in shares of Alcoa (AA, Fortune 500). Bank of America (BAC, Fortune 500) was the worst performer on the blue-chip index. The bank said it will need to revise its dividend plan after the Fed rejected the bank's initial proposal.

Companies: Shares of General Mills (GIS, Fortune 500) dropped 1.8%. The cereal maker, which raised prices in October, said its fiscal third-quarter earnings rose 18%, though U.S. sales were slightly lower.

Adobe Systems (ADBE) was the biggest decliner on the S&P 500 and Nasdaq. Shares sank 3.7% after the software maker lowered its second-quarter earnings forecast, saying the earthquake and tsunami in Japan will curb sales.

Shares of homebuilder PulteGroup (PHM) rose 3.6% after Goldman Sachs raised its price target on the stock.

Jabil Circuit's (JBL, Fortune 500) stock jumped almost 11%, leading the gainers in the S&P 500. The electronics manufacturing company posted a profit and sales figures above expectations late Tuesday.

Economy: New home sales in February plummeted 17% from January to hit a record low. Year-over-year, sales were down 28%.

Resistance 2:Y82.00

Resistance 1:Y81.10

Current price: Y80.90

Resistance 2: Chf0.9200

Resistance 1: Chf0.9120

Current price: Chf0.9108

Current price: $1.6226

Comments: Rate holds tight a bit higher session lows. Strong support comes at $1.6190 (50% Fibo $1.5980 - $1.6400). Stronger level is around channel line from Jan 07, at $1.6040/45 today. Below losses may widen to Mar 11, 15 and 16 lows near $1.5970/80. Resistance is near $1.6320, then - at $1.6400 (Mar 22 high), also at $1.6460 (2010 highs).

- G7 Forex Intervention Not Aimed at Specific Levels

- G7 Intervention to Cope With Disorderly FX Moves

- To Continue Closely Watch Forex Markets

- G7 Forex Intervention Not Aimed at Specific Levels

- G7 Intervention to Cope With Disorderly FX Moves

- To Continue Closely Watch Forex Markets

Japan's benchmark stock indices ended Thursday's session lower. The Nikkei 225 ended the session down 14.46 points, or 0.15%, to stand at 9434.01. The broader-based TOPIX was 6.36 points lower at 854.74.

Nikkei (-1.7%) 9449.47

Topix (-0.8%) 861.10

DAX +23.48 (+0.35%) 6804

CAC +21.02 (+0.54%) 3914

FTSE-100 +33.17 (+0.58%) 5796

Dow +67.39 (+0.56%) 12086.02

Nasdaq +14.43 (+0.54%) 2698.30

S&P500 +3.77 (+0.29%) 1297.54

Oil +0.54 $105.51

10-Years +0.02 3.35%

07:45 France Business confidence (March) 106 106

07:58 France PMI (March) flash 59.5 55.7

07:58 France PMI services (March) flash 56.2 59.7

08:28 Germany PMI (March) flash 62.0 62.7

08:28 Germany PMI services (March) flash 58.4 58.6

08:58 EU(17) PMI (March) flash 58.2 59.0

08:58 EU(17) PMI services (March) flash 56.3 56.8

09:00 Italy Consumer confidence (March) - 106.4

09:30 UK Retail sales (February) -0.5% 1.9%

09:30 UK Retail sales (February) Y/Y 2.4% 5.3%

12:30 USA Jobless claims (week to 19.03) 373K 385K

12:30 USA Durable goods orders (February) 1.0% 3.2%

12:30 USA Durable goods orders excluding transportation (February) 2.0% -3.6%

12:30 USA Durable goods orders excluding defence (February) 0.8% 1.9%

20:30 USA M2 money supply (14.03), bln - +9.7

23:30 Japan Nationwide CPI (February) - -0.2%

23:30 Japan Nationwide CPI (February) Y/Y - 0.0%

23:30 Japan Nationwide CPI ex fresh food (February) Y/Y -0.3% -0.2%

23:30 Japan Tokyo-area CPI (March) - -0.1%

23:30 Japan Tokyo-area CPI (March) Y/Y - -0.1%

23:30 Japan Tokyo-area CPI ex fresh food (March) Y/Y -0.3% -0.4%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers