- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 12-07-2011.

Although the reaction wasn't immediate, stocks have been moving higher in response to verbiage in the minutes from the most recent FOMC meeting regarding the possibility of additional monetary policy stimulus. The climb has given the Dow and S&P 500 solid gains. The Nasdaq continues to lag its counter parts, but it has finally managed to poke into positive territory.

Minutes outline possible exit procedures but immediately backtrack by saying Fed is "prepared to make adjustments to its exit strategy if necessary in light of economic and financial developments" - and indeed key data has weakened since the meeting. Bernanke's testimony Wed-Thur should explain this; note that prior released central-tends already showed weaker outlook. Mins say employment situation disappointed, show Greek worries about exposure here; also a number of members had inflation worries, but most said inflation bump-ups were transitory. FOMC had 'prudent planning' session on exit, said this did not mean it will begin soon, but outlined exit. 'Some' talked about add'l accommodation; 'others' saw less slack in slow growth/high inflation; several said labor mkt needs to reallocate and this reduces potential output, arguing that withdrawing accommodation could

begin sooner than expected under stagflation. 'A few' expressed uncertainty about efficacy of mon-policy but disagreed on implications. So FOMC remained split about moving forward.

The common currency pared losses against its major counterparts after Luxembourg Finance Minister Luc Frieden said selective default on Greek debt isn’t an option “envisaged” by euro-region finance ministers and Italian government bonds reversed losses. The yen reached its strongest level against the dollar since the Group of Seven nations jointly intervened to weaken the currency.

“The story all along has been that the euro-area authorities have been doing just enough to stop the fears from being a big issue in the short term, but not enough to stop them from being a big issue in the long term,” said Paul Robinson, the global head of foreign-exchange research at Barclays Plc in London. “The perceived likelihood of something going really badly wrong in the short run has increased quite significantly.”

The euro earlier dropped to the lowest level in four months versus the yen and the dollar after a meeting of European Union finance ministers failed to defuse the region’s escalating debt crisis.

The dollar erased gains versus the pound, Canadian dollar and Swedish krona after U.S. stock markets advanced after falling as much as 0.3 percent. The Standard & Poor’s 500 Index traded 0.2 percent higher.

The U.S. currency fell for a third day versus the yen before the Federal Reserve releases minutes today from its June meeting amid signs the nation’s recovery is faltering.

Both the Dow and S&P 500 have poked back into positive territory, but the Nasdaq has been unable to make any kind of gain at all this session. Semiconductor stocks have been a heavy drag on the tech-rich Nasdaq, but large-cap tech names like Google (GOOG 534.22, +6.94) and Cisco (CSCO 15.88, +0.44) have offered some support.

A few regional lenders, like Huntington Bancshares (HBAN 6.35, +0.02), have provided a modicum of support to the Nasdaq. Overall, though, financials make up the strongest performing sector this session. That has given the sector an enviable gain of 0.7%. Banks haven't really been the drivers of that move, however. Instead, buying interest in insurance and financial services providers like Hartford Financial (HIG 25.66, +0.56) has fueled the move.

On the topside offers remain at Y111.75/80 and Y112.25/30 ahead of Y112.80/90. On the downside bids sitting at Y110.85/80 a break to open Y110.25/20.

Commodities are mostly lower this morning with a only a select few in positive territory.

The energy markets are lower, excluding natural gas. Crude oil futures were in the red all morning, but have been steadily trending higher. Crude has now moved back near the unchanged line from its session low of $93.55/barrel; now at $95.14/barrel. Natural gas futures are currently up 0.6% at $4.30/MMBtu.

Precious metals are mixed with small gains in gold and silver showing losses. Gold rose as high as $1554.40/oz. earlier this morning and is now up 0.1% at $1551.50/oz. Silver is down 0.7% at $35.44/oz.

Corn futures opened higher a few minutes ago following this morning's USDA supply/demand report. Corn futures are currently up 7 cents (or 1.1%) at $6.40/bushel.

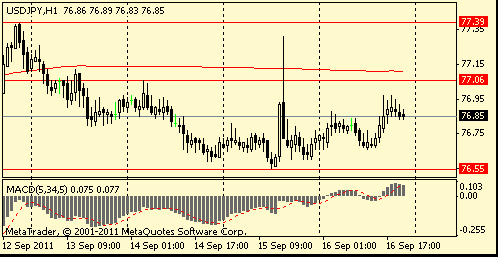

USD/JPY has settled into a broad Y79.00/Y80.00 range with rate currently holds around Y79.55. Bids towards the days lows Y79.20/10 with larger stops now sitting below Y79.00, which if triggered opens Y78.50. Offers seen at Y80.00, extending to Y80.80. Stops extending to Y81.00.

The Nasdaq has attempted to stabilize after sliding earlier amid a drop by tech stocks to a loss of 1.0%. Both tech and the Nasdaq are being weighed down by weakness in Novellus (NVLS 32.97, -2.80) shares, which have tumbled 8% even though the company posted an upside earnings surprise for its latest quarter.

- sees German HICP inflation +2.5% in 2011, +1.6% in 2012;

- German deficit of 1.9%/GDP in 2011, 1.1% in 2012;

- Germany's banking system has returned to broad stability.

EUR/USD $1.4000, $1.4100

USD:JPY Y80.00, Y80.55, Y81.00

AUD/USD $1.0600, $1.0550, $1.0410

U.S. stocks were headed for another weak day Tuesday, as fears about the eurozone debt crisis spreading to Italy rattled investors' nerves.

Economy: The U.S. trade balance figures for May came in at $50.2 billion - far larger than a revised $43.6 billion in April. The trade deficit was also wider than the $44 billion expected by economists.

World markets: European stocks fell in morning trading. Britain's FTSE 100 shed 1.6%, the DAX in Germany retreated 2.0%, and France's CAC 40 tumbled 2.4%.

Asian markets ended the session sharply lower. The Shanghai Composite dropped 1.7%, the Hang Seng in Hong Kong tumbled 3.1% and Japan's Nikkei lost 1.4%.

Companies: After the closing bell Monday, Alcoa (AA, Fortune 500) reported a larger than expected gain in second-quarter sales but investors weren't impressed.

While Alcoa beat on sales, earnings were only in line with recently lowered analyst estimates. Shares slid more than 1% in premarket trading.

Bank shares were also under pressure, with Bank of America (BAC, Fortune 500), Wells Fargo (WFC, Fortune 500) and Citigroup (C, Fortune 500) all off a little more than 1%.

Shares of tech firm Microchip (MCHP) slumped 5.7%, after the company lowered its earnings guidance.

Shares of Novellus Systems (NVLS) fell 5%, after the company delivered disappointing quarterly results and guidance.

EUR/JPY holds higher - now around Y111.65. Topside offers remain at Y112.25/30 and Y112.80/90. Support seen at Y111.30/25.

AUD/USD holds above resistance to a new session high of $1.0625. Stops through $1.0660 ahead of $1.0669 (55-daily MA) with a break here to open $1.0680/90. On the downside bids of note at $1.0575/70 and $1.0555/50.

Data released:

05:30 France CPI (June) unadjusted 0.1% 0.1% 0.1%

05:30 France CPI (June) unadjusted Y/Y 2.1% 2.1% 2.0%

05:30 France HICP (June) Y/Y 2.3% 2.2% 2.2%

06:00 Germany CPI (June) final 0.1% 0.1% 0.1%

06:00 Germany CPI (June) final Y/Y 2.3% 2.3% 2.3%

06:00 Germany HICP (June) final Y/Y 2.4% 2.4% 2.4%

08:30 UK HICP (June) -0.1% 0.2% 0.2%

08:30 UK HICP (June) Y/Y 4.2% 4.5% 4.5%

08:30 UK HICP ex EFAT (June) Y/Y 2.8% 3.4% 3.3%

08:30 UK Retail prices (June) 0.0% 0.3% 0.3%

08:30 UK Retail prices (June) Y/Y 5.0% 5.2% 5.2%

08:30 UK RPI-X (June) Y/Y 5.0% 5.3% 5.3%

08:30 UK Trade in goods (May), bln -8.5 -7.2 -7.6 (-7.4)

08:30 UK Non-EU trade (May), bln -5.1 -4.2 -4.5 (-4.3)

The euro fell after a meeting of European Union finance ministers failed to defuse the region’s escalating debt crisis.

The 17-nation currency fell to a record low versus the Swiss franc as yields on Italian and Spanish debt surged for a second day.

European finance ministers yesterday said they were considering using bond buybacks to ease Greece’s plight as bond yields surged in Italy and Spain. The announcement came after talks with bondholders on a swap of maturing Greek debt for new securities ran into opposition from the European Central Bank.

International Monetary Fund Managing Director Christine Lagarde told reporters in Washington that the fund isn’t discussing details of a second bailout with the EU, and “nothing should be taken for granted” on Greece.

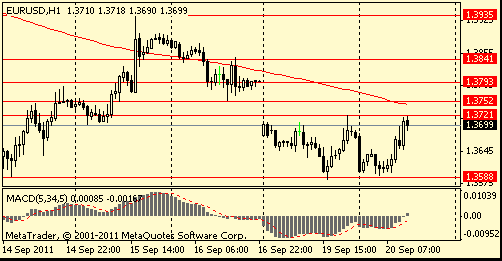

EUR/USD recovered to $1.3996 after earlier it fell to $1.3830.

GBP/USD fell to $1.5775 before rose back to $1.5852.

USD/JPY continued to recover, holding currently at Y79.72 after it earlier fell to Y79.16.

At 1230GMT, the international trade gap is expected to decrease to $42.7 billion in May. Import prices posted only a modest increase in the month, with imported petroleum prices actually down. The supply shortage of auto imports from Japan will likely appear in the data as well. Meanwhile, Boeing reported 28 deliveries to foreign buyers in May, up from 24 in April.

- not yet discussing new Greek terms, volume, conditions;

- can't take anything for granted on Greece package;

- Italy facing market-driven issues; needs better growth;

- stability fund can't react to mkts but must watch contagion risk;

- IMF "not just a cash machine;" objective is stability;

- warning of massive problems from US default.

- not yet discussing new Greek terms, volume, conditions;

- can't take anything for granted on Greece package;

- Italy facing market-driven issues; needs better growth;

- stability fund can't react to mkts but must watch contagion risk;

- IMF "not just a cash machine;" objective is stability;

- warning of massive problems from US default.

European equity markets suffered further heavy losses on Tuesday.

Italy extended its sharp losses, with the FTSE MIB index shedding 3 per cent to 17,862.74, taking its fall in the past three sessions to more than 11 per cent.

Banks were again the victims. The pace of selling steadied, however, leaving UniCredit down 1.7 per cent to €1.14, while Intesa Sanpaolo lost 2 per cent to €1.50. Insurer Generali lost 2.1 per cent to €12.77.

The biggest fallers on the pan-European FTSE Eurofirst 300, which lost 1.6 per cent to 1,079.65, included Austrian bank Raiffeisen International, down 5.3 per cent to €31.90, and Dutch insurer Aegon, which lost 3.6 per cent to €4.23. Germany’s Commerzbank fell 1.1 per cent to €2.67, having earlier struck a record low of €2.56.

Portugal’s PSI 20 index fell 3.1 per cent to 6,633.74, with bank Banif leading the losses, down 6.1 per cent to €0.56. Spain’s Ibex 35 lost 2 per cent, while the Athens General slid 2.6 per cent.

The euro recovered in early Europe after it was beaten down in Asia on Tuesday, plunging to a record low versus the Swiss franc and sinking to a four-month trough against the dollar on growing concerns that the euro zone's sovereign debt crisis was spreading.

Market participants were especially concerned about the debt of countries such as Spain and Italy, which came under strong selling pressure the day before.

"The market has become particularly concerned due to the sell-off in Italian bonds. A steep widening of the spread between Italian and German bonds is making the market worried," said Osamu Takashima, chief forex strategist at Citibank. "The market was to a certain extent expecting the problems in Greece to spread to Spain, but this drastic move in Italian bonds was very surprising."

The spread on the 10-year Italian bond yield over that of German bonds widened to above 300 basis points the previous day from about 180 bps at the start of the month.

Some traders said the euro came under pressure in Asia as IMF Managing Director Christine Lagarde failed to comment specifically on resolving Greece's problems.

Lagarde said the IMF and its European partners are not yet ready to discuss terms of a second Greek bailout, urging Athens to do more to deal with its debt crisis. Lagarde said Greece had taken important steps to cut its budget deficit but that they were not enough.

"I feel that the euro zone debt situation particularly deteriorated after Portugal was downgraded to junk status last week. The market again started to focus on the debt problem as being a problem for the whole region," said Kimihiko Tomita at State Street and Trust. "The fact that the euro broke decisively below $1.4 is significant. The most recent selling appears to be a bit too rapid, but the market could test the euro further in the short term given current sentiment," Tomita said.

European Union finance ministers meet later on Tuesday and are under the cosh to soothe market nerves ahead of Thursday's Italian bond auctions. Italy is aiming to raise 7.75 billion euros in the debt market, according to estimates from Barclays Capital.

The Bank of Japan kept monetary policy on hold.

USD/JPY continues to recover trading Y79.65 as markets rebound from session lows at Y79.15. Offers in the market at Y79.90/00 a break opens Y80.10/20.

EUR/USD $1.4000, $1.4100

USD:JPY Y80.00, Y80.55, Y81.00

GBP/USD $1.5880, $1.5900

AUD/USD $1.0600, $1.0550, $1.0410

HICP (June) -0.1%

US data starts at 1145GMT with the weekly ICSC-Goldman Store Sales data, while at 1230GMT, US Treasury Secretary Tim Geithner opens a conference on Women in Finance in Washington. Also at 1230GMT, the international trade gap is expected to decrease to $42.7 billion in May. Import prices posted only a modest increase in the month, with imported petroleum prices actually down. The supply shortage of auto imports from Japan will likely appear in the data as well. Meanwhile, Boeing reported

28 deliveries to foreign buyers in May, up from 24 in April.

US data starts at 1145GMT with the weekly ICSC-Goldman Store Sales data, while at 1230GMT, US Treasury Secretary Tim Geithner opens a conference on Women in Finance in Washington. Also at 1230GMT, the international trade gap is expected to decrease to $42.7 billion in May. Import prices posted only a modest increase in the month, with imported petroleum prices actually down. The supply shortage of auto imports from Japan will likely appear in the data as well. Meanwhile, Boeing reported

28 deliveries to foreign buyers in May, up from 24 in April.

US data starts at 1145GMT with the weekly ICSC-Goldman Store Sales data, while at 1230GMT, US Treasury Secretary Tim Geithner opens a conference on Women in Finance in Washington. Also at 1230GMT, the international trade gap is expected to decrease to $42.7 billion in May. Import prices posted only a modest increase in the month, with imported petroleum prices actually down. The supply shortage of auto imports from Japan will likely appear in the data as well. Meanwhile, Boeing reported

28 deliveries to foreign buyers in May, up from 24 in April.

- To watch European debt impact on forex rates

- Higher power costs could hurt capex, spending

- Still Think Q3 output to return to pre-quake

- Using BOJ's own seasonal adjustments in output

- FY11 GDP fcast revised down due to carryover

- Still expect global econ to lead Japan recovery

- Japan capex solid, consumer sentiment up

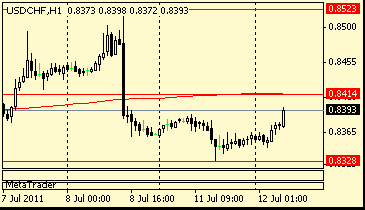

Resistance 3: Y80.50 (Jul 8 low)

Resistance 3: Chf0.8550 (Jun 15-16 high)

Resistance 3: $ 1.6080 (Jul 8 high)

Resistance 3: $ 1.4180 (38.2 % FIBO $1.4575-$ 1.3930)

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers