- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 09-12-2010.

Dow continues to trail its counterparts as it slogs along with a modest loss. 3M (MMM 84.00, -0.68) continues to weigh on the index of blue chips, but IBM (IBM 143.89, -1.09) has actually become the heaviest drag of all. In contrast, Dow component Cisco (CSCO 19.77, +0.42) has attracted strong support. That has also made it a leader on the Nasdaq, which has managed to sport a modest gain for most of the session.

The euro declined after a downgrade to Ireland’s credit rating added to concern Europe’s debt crisis may spread.

The 16-nation currency fell against 13 of its 16 most- traded counterparts as Fitch Ratings reduced Ireland’s rating by three notches and the nation’s government planned a vote on an 85 billion-euro ($114 billion) aid package. The Dollar Index rose for a fourth day after the number of workers filing first- time claims for unemployment insurance payments fell more than forecast.

Fitch cut Ireland’s credit rating to BBB+ from A+, three steps above non-investment grade, citing the mounting cost to rescue the nation’s banking system. “The downgrade reflects the additional fiscal costs of restructuring and supporting the banking system,” Fitch said in the statement. “Ireland’s sovereign credit profile is no longer consistent with a high investment grade rating.”

Applications for U.S. jobless benefits decreased to 421,000, from a revised 438,000 the prior week, Labor Department figures showed. Economists forecast claims would fall to 425,000.

“There’s a lot of nervousness around what is going on in Ireland,” said Jens Nordvig, a managing director of currency research in New York at Nomura Holdings Inc. “We’ve seen U.S. data being solid, that will be more supportive for the dollar.”

Stryker (SYK 52.89, +0.80) has put together a nice gain following this morning's announcement that the company has added $500 million to its share repurchase plan and has hiked its quarterly dividend by 20% to $0.18 per share.

In a similar vein, Western Union (WU 18.66, +0.01) announced that it has hiked its dividend by 17% to $0.07 per share. Meanwhile, Whole Foods (WFMI 48.68, -0.22) announced that it has reinstated its quarterly dividend of $0.10 per share.

The S&P 500 has made its way back to a narrow gain. Energy stocks have become a drag on trade, however; that sector is down 0.3% at the moment.

Energy's decline has come primarily from weakness in oil and gas exploration and production outfits like Range Resources (RRC 42.48, -1.38), Noble Energy (NBL 82.38, -1.39), and Devon Energy (DVN 72.00, -1.18).

A recent bounce in oil prices does not appear to have helped the energy sector. Oil prices just poked into positive territory to trade at $88.30 per barrel.

- Withdrawal of support must proceed with caution and care

- Exit must not threaten financial stability, economic recovery

- Acute concerns about addicted banks when ecb resumes exit

- Interplay between public debt problems, weak banks a risk

- Reemergence of global imbals, disorderly unwinding a risk

- If risks materialize could cause problem of systemic dimension

- See EMU debt crisis contagion risk, but low probability

- Baseline scenario sees emu financial system strengthening further

- Risk of bank funding vulnerabilities, dampened profit

- Need strong government commitment to rein in public sector imbalances

- Must improve competitiveness of and confidence in emu

- EMU banks' funding markets have improved, but still not normal

- Fiscal consolidation may weigh on bank earnings short-term

Up to EMU governments to decide on Eurobonds

ECB to continue to adjust liquidity supply to situation

Expect liquidity to drop with expire of 12-m tender

See structural shift to ECB refis from interbank deals

Up to EMU governments to decide on Eurobonds

ECB to continue to adjust liquidity supply to situation

Expect liquidity to drop with expire of 12-m tender

See structural shift to ECB refis from interbank deals

Barclays says +1.9% Oct wholesale inventories follows up-revised +2.1% for Sept and these suggest up-side risks for inventory accumulation. "The increase in October was broad based, with a 0.9% rise in durables and a 3.2% jump in non-durables. The former was despite a 0.1% decline in the autos component." Their Q4 GDP tracking estimate stands at +3.1%.

- No comment on Fitch downgrade of Ireland

- Congratulates Irish parliament for budget approval

U.S. stocks were poised to open slightly higher amid the latest report on the number of Americans filing for first-time unemployment benefits.

Economy: The number of Americans filing for their first week of unemployment benefits fell last week, pointing to slight improvement in the job market.

The number of initial claims fell to 421,000 in the week ending Dec. 4, down 17,000 from a revised 438,000 claims filed the week before, the Labor Department said Thursday.

The weekly figure beat analyst forecasts of 429,000 for the week.

After the opening bell, the Commerce Department will release a report on wholesale inventories that is expected to show inventories fell to 0.7%, from 1.5% in October.

Companies: Howard Stern announced that he has re-signed with SiriusXM (SIRI) Radio for five years, sending Sirius' stock surging 11% in premarket trade.

After the market close, Green Mountain Coffee (GMCR) is expected to report an earnings per share of 20 cents, down from the 34 cents per share it reported a year ago.

Data released

07:00 Germany CPI +0.1% +0.1% +0.1%

07:00 Germany CPI, y/y +1.5% +1.5% +1.3%

09:00 EU ECB Monthly Report

09:30 UK Trade in goods -5.00 -4.45 -4.60

12:00 UK BoE Interest Rate Decision 0.5% 0,50% 0,50%

The pound stayed lower against the dollar after the Bank of England decided to maintain its asset- purchase program and kept interest rates at a record low.

All economists predicted central bank Governor Mervyn King would keep the so-called quantitative-easing program unchanged at 200 billion pounds ($315 billion). Economists in a separate survey said the bank would hold the main interest rate at 0.5% .

The decision “ought to be relatively neutral for sterling,” Adam Cole, head of global currency strategy at RBC Capital Markets.

Sterling depreciated as a report showed house prices fell. Halifax House Prices fell 0.7% y/y after +1.2% in October and slept -0.1% m/m after +0.3%.

Australia’s currency retreated after it earlier rise after the statistics bureau said employers added 54,600 workers in November, reducing the unemployment rate to 5.2% from 5.4% in October. Economists forecast 20,000 extra jobs, according to a survey.

Meanwhile, the dollar rose against European currencies but lost ground against the yen as traders continued to mull over the effects of this week’s large sell-off in US and global government bond markets triggered by the agreement on extending Bush-era tax breaks.

EUR/USD printed session lows on $1.3190 after it failed to set above $1.3300. Currently rate consolidates within the $1.3212 range.

GBP/USD fell from $1.5840 to $1.5730, but managed to recover to $1.5756 after BOE rate decision.

USD/JPY slowly rebounded from Y83.60 to Y84.10.

US Jobless claims report is due to come at 13:30 GMT.

The U.S. dollar stayed well supported thanks to higher Treasury bond yields, while the New Zealand currency slumped after dovish comments from the country's central bank.

The 2-year U.S. note yield hit a 4-1/2 month high of 0.64%, though the 10-year yield stepped back a little to 3.27% from 3.33%.

"Now we've seen yields jump sharply and arguably they look like they may have found a level where they may have reached a high point, perhaps that'll cause the dollar rally to settle down," said Greg Gibbs, strategist at RBS. "But this time of year, you sense that people are squaring positions up. The market still has a few short dollar positions out there and this is adding to the excuse for the dollar to strengthen."

The European Commission welcomed Ireland's tough 2011 austerity budget, which received a first approval from parliament, opening the way for international loans to start flowing to Dublin.

In contrast, the New Zealand dollar dropped to a one-week low after the Reserve Bank of New Zealand said it expected interest rates to rise less over the next two years than it had previously forecast.

The RBNZ left rates unchanged at 3.0% as expected but said rates should stay low for longer.

"The kiwi sagged given the much watered down tightening bias," said Annette Beacher at TD Securities. "We can finally confirm that we are pushing out the next rate hike from March to July."

Market attention, however, is turning to China, where speculation of an interest rate hike gained momentum after Beijing brought forward the release of November data, including the closely watched inflation figures to Saturday from Monday.

Data:

00:30 Australia Employment Change (Nov) 54.6

00:30 Australia Unemployment Rate (Nov) 5.2%

The Australian dollar strengthened against all its major counterparts after a government report showed employers added more than twice as many jobs as economists forecast.

Australia’s currency gained for the first time in four days against the greenback as the extra yield the South Pacific nation’s bonds offer over Treasuries widened and traders added to bets the central bank will boost interest rates.

Australia’s currency rallied after the statistics bureau said employers added 54,600 workers in November, reducing the unemployment rate to 5.2 percent from 5.4 percent in October. Economists forecast 20,000 extra jobs, according to a survey.

Reserve Bank of Australia Governor Glenn Stevens will increase the benchmark rate by 41 basis points over the next 12 months, up from a prediction of 24 basis points at the end of last week, according to a Credit Suisse AG index.

EUR/USD: the pair shown high above a mark $1,3300.

GBP/USD: the pair bargained within the limits of $1,5790-$ 1,5840.

USD/JPY: the pair decreased below mark Y84,00.

At 0900GMT, the ECB releases the December Monthly Bulletin, although this is usually built around the opening statement of the ECB President at the recent post-meeting press conference. UK data starts at 0800GMT with the monthly Halifax House Prices data for November. UK data continues at 0930GMT with trade data and also SMMT Car Production. At 1200GMT, the Bank of England MPC Monetary Policy Announcement is due, but given the latest signs that the moderate UK economic recovery remains steadily on track going into the fourth quarter, there seems little cause for the majority of the Bank of England Monetary Policy Committee to come down off the fence at the December policy meeting.

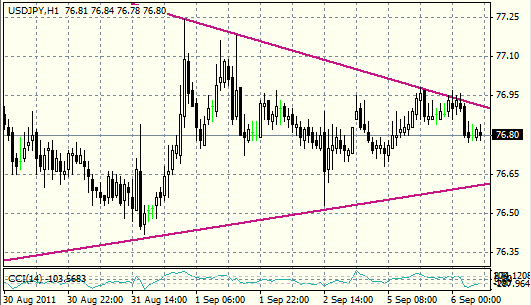

Resistance 3:Y85.90 (high of September)

Resistance 2:Y84.40 (Nov 29 high, Dec 1 and 2 high)

Resistance 1:Y84.150 (session high)

Current price: Y83.36

Support 1:Y83.60 (session low)

Support 2:Y83.30 (50,0 % FIBO Y82,20-Y84,30)

Support 3:Y82.30 (Dec 7 low, 50.0 % FIBO Y80,20-Y84,40)

Comments: the pair decreased. The nearest support - Y83,60. Below losses are possible to Y83.30. The nearest resistance - Y84,15. Above growth is possible to Y84.40.

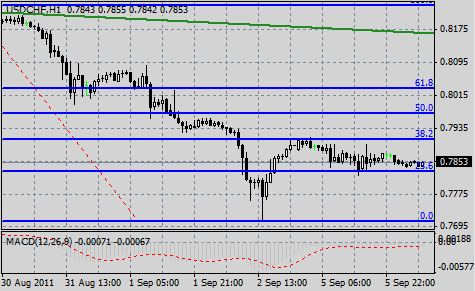

Resistance 3: Chf1.0070 (Dec 1 high)

Resistance 2: Chf0.9950 (Dec 3 high)

Resistance 1: Chf0.9915 (Dec 8 high)

Current price: Chf0.9836

Support 1:Chf0.9820 (session low)

Support 2: Chf0.9760 (Dec 7 low)

Support 3: Chf0.9720 (Dec 6 low)

Comments: the pair decreased. The nearest resistance Chf0,9915. Above is located Chf0.9915. The nearest support Chf0,9820. Below loss may extend to Chf0.9760.

Resistance 3: $ 1.3475 (50.0% FIBO $1,3790-$ 1,2970, 38.2 % FIBO $1.4280-$ 1.2970)

Resistance 2: $ 1.3430 (Dec 6 high)

Resistance 1: $ 1.3325 (session high)

Current price: $1.3310

Support 1 : $1.3240 (session low)

Support 2 : $1.3180 (Dec 8 low)

Support 3 : $1.3060 (Dec 2 low)

Comments: the pair become stronger. The nearest resistance - $1,3325. Above growth is possible to $1,3430. The nearest support - $1,3240. Below decrease is possible to $1.3180.

Resistance 3: $ 1.5985 (61,8 % FIBO $1,6300-$ 1,5490)

Resistance 2: $ 1.5890 (50,0 % FIBO $1,6300-$ 1,5490)

Resistance 1: $ 1.5830 (session high, Dec 8 high)

Current price: $1.5820 Support 1 : $1.5790 (session low)

Support 2 : $1.5720 (support line from Dec 2)

Support 3 : $1.5655 (Dec 6 low)

Comments: the pair bargains above a mark $1,5800. The nearest support - $1,5790. Below decrease is possible to $1.5720. The nearest resistance - $1,5830. Above growth is possible $1,5890.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers