- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 03-05-2011.

Recent selling pressure has paused, leaving stocks to rest at session lows. The retreat hurt energy stocks the most; the sector is now down 2.6%, which is almost double the loss of the next worst performing sector (materials, -1.4%). Energy's moves today have been tied closely to those of oil prices, which are now at $110.60 per barrel for a fresh session low and a 2.6% loss.

The stock market is without direction for the second straight session. The lackluster trade is partly a consequence of so few catalysts, given the absence of meaningful data in recent days and the shift in the earnings announcement lineup away from blue chips and industry bellwethers to names with less quality.

Even though the stock market continues to chop along, Treasuries are still having a quiet session. As such, the benchmark 10-year Note is up only a handful of ticks.

The yen and the Swiss franc rose against all of their most-traded counterparts as investors sought the currencies’ relative safety amid declines in equities and commodities.

The dollar erased gains against the euro as stocks trimmed losses after a report showed U.S. factory orders rose more than forecast. Canada’s dollar fluctuated after rising earlier as Prime Minister Stephen Harper’s Conservatives won a majority of seats in Parliament for the first time.

“It’s somewhat of a risk-off day, and the more defensive currencies are outperforming,” said Paul Mackel, a currency strategist at HSBC Holdings Plc in London. “Some people have been looking at how crowded it was getting to be in terms of short dollars, so you’re seeing some risk being taken off the table.” A short is a bet a currency will fall.

The dollar earlier strengthened from a 16-month low against the euro on speculation the European currency’s gains this year may not be sustained.

Orders placed with U.S. factories rose 3 percent in March, a fifth consecutive increase, the Commerce Department said today. The median forecast of economists projected a 2 percent increase.

The pound was the worst performer among major currencies, dropping as an index of U.K. manufacturing growth declined. Markit Economics and the Chartered Institute of Purchasing and Supply index fell to 54.6 in April from 56.7 in March.

Bank of England Governor Mervyn King said high debt levels pose “massive” economic challenges that would be exacerbated by increased long-term interest rates.

“The market continues to price out the chance of a rate hike before the end of August,” said Stephen Gallo, head of market analysis at Schneider Foreign Exchange in London. The delay in an interest rate increase will cause a “selloff in the pound.”

Bank of England policy makers are split four ways over monetary policy. The central bank probably will leave the key interest rate at a record-low 0.5 percent at the next rate meeting on May 5.

The major equity averages are working their way up from session lows, but the Nasdaq continues to wrestle with relatively stiff selling pressure. Its weakness comes largely as a result of losses among the likes of Cisco (CSCO 17.41, -0.17), Akamai Tech (AKAM 33.80, -0.43), and Broadcom (BRCM 34.88, -0.40). However, Apple (AAPL 348.87, +2.59) and Intel (INTC 23.42, +0.51) have been sources of support.

EUR/USD recovers again, holding at $1.4878. rate holds a bit lower Monday's high at $1.4902. Offers seen into that high area but stops are noted above $1.4910. Euro last at $1.4872.

Hit a fresh low on the day of $1532.90 before bouncing. Support now seen towards $1532 and $1524.50. Gold currently trades around $1538.00

EUR/USD $1.4800, $1.4630, $1.4600

USD/JPY Y82.25, Y83.00

EUR/JPY Y123.00

GBP/USD $1.6800, $1.6400

GBP/JPY Y132.00

AUD/USD $1.0750

U.S. stocks were set to open lower Tuesday, as investors shift focus back to the economy, and await auto sales and factory orders.

On Monday, U.S. stocks finished slightly lower, as investors reversed from their initial positive reaction to news that Osama bin Laden had been killed.

April was the strongest month for stocks since December.

Economy: The Commerce Department releases data on March factory orders at 14:00 GMT, with economists looking for a 2.5% rise, compared with February's 0.1% decline.

Investors will also get monthly auto sales figures from the major car makers.

Companies: Dow component Pfizer (PFE, Fortune 500) reported earnings per share that beat by a penny but revenue was just in line with forecasts. And the drugmaker reaffirmed its outlook but investors were hoping for more. Shares fell about 1% in premarket trading.

Sears Holdings (SHLD, Fortune 500) issued a disappointing outlook late Monday. Shares fell nearly 5% in premarket trading.

Other companies reporting on Tuesday include credit card processor MasterCard (MA, Fortune 500), media company CBS (CBS, Fortune 500), and food processor Archer Daniels Midland Co (ADM, Fortune 500).

EUR/GBP printed a fresh session high around stg0.8985 and currently holds a bit lower. Clean break above will target option barrier at stg0.9000 with offers ahead.

Gold heads down to the overnight lows seen in Asia with a European session low of $1536.05. A break of $1534.80 likely to extend to $1524/25 area.

Silver has broken through the Asian low of $43.55 to $43.00. Silver currently trades around $43.48 with Gold at $1539.75

AUD/USD just printed a fresh day's low of $1.0846 having filled some real money demand in the $1.0850/55 area and tripped some small stops through $1.0850. Aussie trades $1.0857/59.

Data released:

08:30 UK CIPS manufacturing index (April) 54.6 57.5 57.1

09:00 EU(17) PPI (March) 0.7% 0.4% 0.8%

09:00 EU(17) PPI (March) Y/Y 6.7% 6.4% 6.6%

10:00 UK CBI retail sales volume balance (April) 21% 18% 15%

The yen and dollar rose against most major counterparts as stocks fell and concern about reprisal attacks following the death of Osama bin Laden boosted demand for the relative safety of the Japanese and U.S. currencies.

“There seems to be worries over retaliation terrorist attacks,” said Satoshi Okagawa at Sumitomo Mitsui Banking Corp.. “There’s risk aversion, with the yen and the dollar being bought.”

The yen reached the strongest level in almost a week versus the dollar as Asia’s benchmark stock index slid to its biggest loss in three weeks.

Financial markets in Japan are shut today for a holiday.

The Australian and New Zealand dollars fell as lower commodity prices damped demand for the nations’ assets.

“With a commodity unwind, commodity currencies will come under pressure,” said Tim Kelleher, vice-president of institutional banking and markets at Commonwealth Bank of Australia.

The Aussie held its losses after the Reserve Bank of Australia left the overnight cash rate target at 4.75% at a policy meeting today.

Canada’s currency strengthened as Prime Minister Stephen Harper won a return to office with a majority government.

Harper’s party was ahead or leading in 167 of 308 districts, according to results posted on Election Canada’s website. The New Democratic Party was leading in 102 seats and will form the official opposition, followed by 34 for the Liberal Party. The separatist Bloc Quebecois led in three seats.

The pound dropped as an index of U.K. manufacturing growth fell. Markit Economics and the Chartered Institute of Purchasing and Supply index fell to 54.6 in April from 56.7 in March.

EUR/GBP failed to challenge $1.4850 to spur short-adjustment. Rate fell to the lows around $1.4752. Later rate was back to $1.4774.

GBP/USD fell after the weak data from $1.6650 to $1.6460. But currently rate tries to recover and holds around $1.6480.

USD/JPY weakened to Y80.80 after lasting consolidation within the Y80.90/81.10 range.

US data includes domestic-made light vehicle sales, which are forecast to rise to a 9.9 million annual rate in April after falling slightly in March. At 1400GMT US factory new orders are expected to rise 2.0% in March.

USD/JPY refreshed session low on Y80.68. Talk of some stops through the level, ahead of machine bids Y80.55/60. Stops now placed for a break of Y80.50 with more through Y80.40/35. Rate currently trading Y80.76/78.

- Pledges to strengthen liquidity management

- Says will increase exchange rate flexibility

- No absolute ceiling for reserve requirement ratio

- To use interest rates to manage inflation expects

- Econ growth rate, employment at reasonable levels

- Stabilizing prices the top priority

- Global inflation pressure is building

- U.S., Japan sov debt crises unlikely in short-term

- Europe banks could need more fiscal injections

- Investor demand hit if fiscal positions worsen

- Pledges to strengthen liquidity management

- Says will increase exchange rate flexibility

- No absolute ceiling for reserve requirement ratio

- To use interest rates to manage inflation expects

- Econ growth rate, employment at reasonable levels

- Stabilizing prices the top priority

- Global inflation pressure is building

- U.S., Japan sov debt crises unlikely in short-term

- Europe banks could need more fiscal injections

- Investor demand hit if fiscal positions worsen

GBP/USD remains under pressure after it fell to the lows around $1.6470. Break under opens a deeper move toward $1.6455/50 ahead of stronger support between $1.6435/30.

EUR/GBP printed session highs on stg0.8978 on French corporate demand interest before cross retreted to current stg0.8960.

USD/CAD holds close to stops in place on a break above C$0.9550, with larger stops interest noted above C$0.9625. Rate currently trades around C$0.9535 after falling to the lows around C$0.9455 earlier in the session.

FTSE-100 made a brief high at 6,103 at open, which puts in a potential double-top at 6,103/6,105. Traders look for further weakness.

The dollar hobbled near a three-year trough against a currency basket on Tuesday, undermined by loose U.S. monetary policy, but analysts said it's fall was looking overextended due to extreme short positioning.

The dollar slipped to a record low against the Swiss franc at Chf0.8619 in early trade, slipping under Friday's low of Chf0.8626.

"It's very much a case of buying the dips in euro/dollar at these levels. Rate hike expectations are anchoring the euro," said Chris Walker, currency strategist at UBS.

The single currency hit a 17-month high of $1.4903 on Monday.

Sterling fell to its lowest level since March 2010 against the euro after a survey of UK manufacturing came in below market expectations.

"Core UK data has begun to disappoint to the downside. It seems like all bets are off for a UK rate hike until year-end," said Walker at UBS.

The Canadian dollar staged a brief relief rally as Canada's ruling Conservatives won a crushing victory in the federal election. Provisional results showed the Conservatives had 166 seats in Parliament, well above the 155 they needed to transform their minority government into a majority.

The Australian dollar dipped after Australia's central bank kept interest rates unchanged at 4.75% as expected. The Reserve Bank of Australia said underlying inflation looked to have bottomed and would increase somewhat as the economy strengthened, sounding a little less hawkish than some analysts had expected.

GBP/USD under pressure ahead of CBI report at the top of the hour. Rate extends lows to reported support at $1.6480. A break below here to open a deeper move toward $1.6450 ahead of stronger area between $1.6435/30. Resistance seen back at $1.6540/50.

EUR/USD $1.4800, $1.4630, $1.4600

USD/JPY Y82.25, Y83.00

EUR/JPY Y123.00

GBP/USD $1.6800, $1.6400

GBP/JPY Y132.00

AUD/USD $1.0750

Data:

03:30 Announcement of the RBA decision on the discount rate - 4.75%

The yen rose against most of its major counterparts as Asian stocks declined amid signs global economic growth is losing momentum, boosting demand for the relative safety of Japan’s currency.

Japan’s currency advanced against 15 of its 16 major counterparts as the U.S. and Australia increased security at their embassies around the world on concern this week’s killing of Osama bin Laden will lead to revenge attacks.

The Australian and New Zealand dollars fell as lower commodity prices damped demand for the nations’ assets.

Canada’s currency strengthened as Prime Minister Stephen Harper won a return to office with a majority government.

EUR/USD: the pair shown high in the field of $1.4820 then decreased below a mark $1.4800.

GBP/USD: the pair decreased in around $1.6580.

USD/JPY: the pair receded in around Y80.80.

European data for Tuesday includes the latest German car registrations data.

In the UK, data starts at 0830GMT with PMI Manufacturing data for April. UK data also includes the latest CBI Distributive Trades data at 1000GMT.

US data includes domestic-made light vehicle sales, which are forecast to rise to a 9.9 million annual rate in April after falling slightly in March. At 1400GMT US factory new orders are expected to rise 2.0% in March.

The dollar fell for a 10th straight day, the longest slump in 17 years, after slower manufacturing growth reinforced speculation the Federal Reserve will maintain record-low rates.

Dollar index advanced earlier after the U.S. said al-Qaeda leader Osama bin Laden had been killed.

The euro gained to a 16-month high before the European Central Bank, which raised interest rates last month, meets this week. The Fed kept its rates on hold last week.

The Institute for Supply Management’s factory index was at 60.4 for April, slipping from 61.2 the previous month. Manufacturing expanded for a 21st straight month.

A widening interest-rate gap between America and the rest of the world may mean no rebound this year for the dollar.

The Fed is expected to hold its benchmark interest rate at zero to 0.25% benchmark interest rate, where it’s been since December 2008, until the first quarter of 2012, according to the weighted average forecast.

While a weaker dollar may signal waning confidence in the U.S., it also may help President Barack Obama reach his goal of doubling exports by 2015 and reducing unemployment.

The yen snapped two days of gains versus the euro after Obama said bin Laden was killed after a firefight at a house in Pakistan. Bin Laden was the architect of a radical Islamist movement that killed almost 3,000 people in the U.S. on Sept. 11, 2001, and recast global security and politics.

EUR/USD: the pair shown high in the field of $1.4820 then decreased below a mark $1.4800.

GBP/USD: the pair decreased in around $1.6580.

USD/JPY: the pair receded in around Y80.80.

European data for Tuesday includes the latest German car registrations data.

In the UK, data starts at 0830GMT with PMI Manufacturing data for April. UK data also includes the latest CBI Distributive Trades data at 1000GMT.

US data includes domestic-made light vehicle sales, which are forecast to rise to a 9.9 million annual rate in April after falling slightly in March. At 1400GMT US factory new orders are expected to rise 2.0% in March.

Japanese stocks rose for a third day after U.S. companies reported better-than-expected earnings and President Barack Obama said Osama bin Laden is dead.

Toyota Motor Corp. (7203), the world’s largest carmaker, and Sony Corp. (6758), Japan’s biggest electronics exporter, both advanced at least 1.9 percent.

Komatsu Ltd. (6301), the world’s No. 2 manufacturer of construction equipment, jumped 3 percent after rival Caterpillar Inc. (CAT) posted earnings that beat estimates.

Hitachi Construction Machinery Co. advanced 2.1 percent to 2,007 yen and Kubota Corp. (6326), a maker of farming equipment, rose 1.4 percent to 781 yen.

Oil driller Inpex Corp. (1605) and other energy-related companies fell after crude prices dropped by the most in two weeks.

Shares also rose after Japanese companies posted better earnings. Seiko Epson Corp. (6724) jumped 5.7 percent to 1,492 yen after forecasting net income will soar by 66 percent this fiscal year, buoyed by demand from China, India and other Asian countries. Ebara Corp. (6361) surged 5.9 percent to 482 yen after reporting full-year net income that more than doubled its own forecast. Profit at the pump maker rose to 28.5 billion yen ($350 million) in the 12 months ended March 31, according to a preliminary earnings statement on April 28.

Panasonic Corp. (6752), the world’s largest maker of plasma televisions, increased 2.8 percent to 1,026 yen after it announced plans to cut almost 17,000 jobs over two years as part of an overhaul to restore profitability.

European stocks advanced for an eighth day, the longest winning streak in 10 months, as U.S. President Barack Obama said al-Qaeda leader Osama bin Laden was killed in Pakistan yesterday.

Danisco A/S climbed to the highest since 1989 as the world’s largest food-ingredients maker received an increased takeover bid from DuPont Co.

Demag Cranes AG (D9C) jumped 24 percent after Terex Industrial Holding AG offered to buy the company.

TNT NV (TNT) lost 1.4 percent after the Dutch mail carrier that’s spinning off its express unit said profit fell.

Actelion Ltd. (ATLN) plunged the most in 14 months.

Grifols SA (GRF) rallied 5.3 percent to 14.08 euros, the highest price in more than two years, after the Barcelona, Spain-based maker of blood-plasma products said its purchase of Talecris Biotherapeutics Holdings Corp. won tentative U.S. antitrust approval.

Commerzbank AG (CBK) rose 3.2 percent to 4.44 euros after Germany’s second-biggest bank said profit in the first three months of the year climbed 40 percent to a quarterly record as it set aside less money to cover risky loans.

Carmakers posted the best performance among 19 industry groups in the Stoxx 600 today as Bayerische Motoren Werke AG (BMW) and Daimler AG (DAI) led the advance. The two biggest makers of luxury cars gained 1.2 percent to 64.44 euros and 0.6 percent to 52.51 euros, respectively.

Fiat SpA (F) advanced 3.9 percent to 7.49 euros as its Chrysler Group LLC unit reported its first quarterly profit since emerging from bankruptcy reorganization in 2009.

European manufacturing growth accelerated more than estimated in April, driven by higher output in Germany and France, suggesting the region’s economy is weathering surging energy costs. A gauge of manufacturing in the 17-nation euro area rose to 58 from 57.5 in March, London-based Markit Economics said. That’s above an initial estimate of 57.7 on April 19. A reading above 50 indicates growth.

U.S. stocks edged lower on Monday as investors shifted their focus back to the economy and earnings news.

Monday's losses ends what was a five-day long positive streak for the S&P 500 and Dow.

Alcoa (AA, Fortune 500), Merck (MRK, Fortune 500) and American Express (AXP, Fortune 500) led the blue chips higher Monday, but shares of Microsoft (MSFT, Fortune 500) offset the gains and weighed down the tech sector. Applied Materials (AMAT, Fortune 500) and Whole Foods (WFMI, Fortune 500) were the Nasdaq's biggest laggards.

The losses on Monday come after stocks finished their best month this year on Friday.

Corporate earnings have largely come in above expectations, but last week's weak GDP reading and higher-than-forecast jobless claims show there's still cause for concern about the U.S. economic recovery.

U.S. investors will get the April jobs report, a closely watched gauge of U.S. economic activity, this upcoming Friday.

Economy: The Institute for Supply Management said its April manufacturing index fell to a reading of 60.4%, better than the reading of 58.5% that economists had expected.

Companies: The Nasdaq-100 index will be rebalanced to reduce the weight of Apple's stock by about 40%. Apple (AAPL, Fortune 500) currently represents 20.5% of the index. After the rebalancing, Apple's weight will be reduced to 12.3%.

Shares of TiVo (TIVO) were up 3% after DISH Network Corporation (DISH, Fortune 500) and EchoStar Corporation (SATS) announced they will pay TiVo $500 million to settle an ongoing patent dispute.

Separately, DISH reported earnings per share of $1.22 for the quarter ended in March, easily topping forecasts. Also, DISH said it gained approximately 58,000 net subscribers during the quarter. Shares of DISH jumped 19%.

Resistance 3: Y82.30 (Apr 28 high)

Resistance 2: Y81.70 (May 2 high, МА (200) for Н1)

Resistance 1:Y81.30 (session high)

Current price: Y80.97

Support 1:Y80.90 (session low)

Support 2:Y80.70 (around of Mar 18-24 low)

Support 3:Y79.80 (Mar 17 high)

Comments: the pair decreased. The nearest support - Y80.90. Below losses are possible to Y80.70. The nearest resistance - Y81.30. Above growth is possible to Y81.70.

Resistance 3: Chf0.8830 (Apr 27 high)

Resistance 2: Chf0.8740 (resistance line from Apr 6)

Resistance 1: Chf0.8700 (May 2 high)

Current price: Chf0.8648

Support 1: Chf0.8630 (Apr 29 and May 2 high)

Support 2: Chf0.8600 (psychological mark)

Support 3: Chf0.8500 (psychological mark)

Comments: the pair bargains in the field of Chf0.8650. The nearest resistance - Chf0.8700. Above is located Chf0.8740. The nearest support - Chf0,8630. Below loss may extend to Chf0.8600.

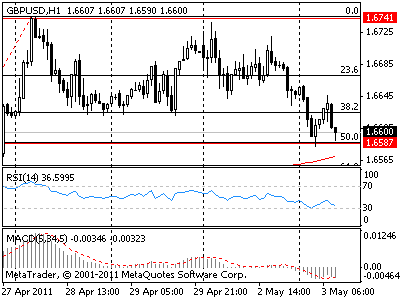

Resistance 3: $ 1.6880 (Nov'2009 high)

Resistance 2: $ 1.6740 (Apr 28-29 high)

Resistance 1: $ 1.6660 (session high)

Current price: $1.6629

Support 1 : $1.6580 (50,0 % FIBO $1,6430-$ 1,6740, session low)

Support 2 : $1.6550 (61,8 % FIBO $1,6430-$ 1,6740)

Support 3 : $1.6430 (Apr 26-27 low)

Comments: the pair decreased. The nearest support $1.6580. Below is possible testings of around $1.6550. The nearest resistance - around $1.6660. Above growth is possible to $1.6740.

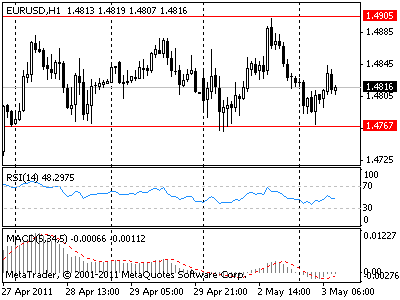

Resistance 3: $ 1.5140 (Nov-Dec'2009 high)

Resistance 2: $ 1.5000 (psychological mark)

Resistance 1: $ 1.4900 (May 2 high)

Current price: $1.4800

Support 1 : $1.4760 (Apr 28 low, May 2 low, session low)

Support 2 : $1.4630 (Apr 27 low)

Support 3 : $1.4490 (Apr 26 low)

Comments: the pair slightly decreased. The nearest support $1,4760. Below losses are possible to $1.4630. The nearest resistance - $1.4900. Above growth is possible to $1,5000.

03:30 Australia RBA meeting announcement 4.75% 4.75% 4.75%

07:00 UK Halifax house price index (April) 0.3% 0.1%

07:00 UK Halifax house price index (April) 3m Y/Y -2.9% -2.9%

08:30 UK CIPS manufacturing index (April) 57.5 57.1

09:00 EU(17) PPI (March) 0.4% 0.8%

09:00 EU(17) PPI (March) Y/Y 6.4% 6.6%

10:00 UK CBI retail sales volume balance (April) 18% 15%

12:55 USA Redbook (30.04)

14:00 USA Factory orders (March) 1.5% -0.1%

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers