- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 01-06-2011.

The major market averages trade near their worst levels of the day with the S&P 500 off 1.8%. Today's weakness in equities has led investors to the safety of Treasuries. Treasuries finished the day with strong gains, but off their best levels of the session amid poor economic data.

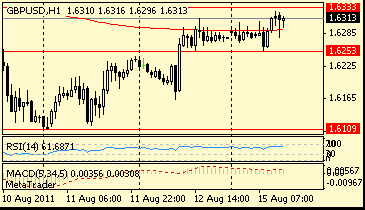

GBP/USD printed fresh lows for the day around $1.6344 after the London close after triggering demand interest around $1.6380 and then - at $1.6360/50. Currently rate holds around $1.6362.

Analysts at DB say "today's weak data point to a nonfarm payroll gain of +160k, down from our previous estimate of +225k which we cut last week from +300k. We are leaving our estimate of the unemployment rate at 8.9% (-0.1%)".

NYMEX July light sweet crude oil futures (WTI) are off $2.29 at $100.22 per barrel, after trading in a $101.54 to $103.31 range. To resume the upward trend the prices should vault its 55-day moving average (currently at $104.94). The front contract last closed above its 55-day May 4. The 100-day, at $99.37, will act as initial support.

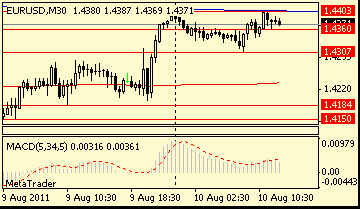

EUR/USD fell under the figure and currently holds around fresh lows near $1.4370/80 area as euro longs are closed. Pair exposed bids at $1.4380. Further bids expected $1.4360/50.

U.S. equities have slipped to their lowest levels of the day with the Dow trading down 1.5% to lead the major averages lower.

Gold miners are one of the few positives today, responding to the yellow metal's move above $1550 per ounce. Despite the underlying strength in gold some of the large cap gold miners such as Barrick Gold (ABX 47.68, -0.08) and Newmont Mining (NEM 56.11, -0.46) have recently slipped into negative territory. However, smaller miners such as Agnico-Eagle Mines (AEM 65.02, +0.32) and Kinross Gold (KGC 15.86, +0.14) continue to hold modest gains.

The dollar dropped to the lowest in three weeks as reports showed slower-than-forecast jobs growth and reduced factory output, adding to concern the U.S. economy is slowing.

The U.S. currency weakened after a private survey showed employment increased by 38,000 last month, the smallest gain since September and a measure of manufacturing output in May declined more than forecast.

U.S. employment increased last month after a revised 177,000 gain in April, according to figures from ADP Employer Services. The median estimate called for a 175,000 advance for May.

The Labor Department will release May unemployment figures June 3. Goldman Sachs Group Inc. revised its estimate today for an increase in May nonfarm payrolls to 100,000 from 150,000, while Citigroup Inc. trimmed its projection to 100,000 from 170,000.

The Institute for Supply Management’s factory index fell to 53.5 in May from 60.4 the prior month. Economists projected the gauge would drop to 57.1.

“Weak data equals a weak dollar,” said Ray Attrill, a senior currency strategist at BNP Paribas SA. “It’s not surprising to see the dollar weaken substantially on the basis of the data.”

The Swiss franc strengthened as retail sales rose in April at the fastest rate in two years, boosting speculation the Swiss National Bank may raise borrowing costs. Retail sales climbed 7.5% in the year after a 0.2% drop in March, the most since April 2009.

EUR/USD: $1.4350, $1.4500, $1.4250, $1.4225

USD/JPY: Y80.30, Y81.15, Y81.25, Y81.40, Y81.60, Y81.70, Y82.00

EUR/JPY: Y117.05, Y117.40, Y117.50, Y118.00

GBP/USD: $1.6470, $1.6490, $1.6210

AUD/USD: $1.0800, $1.0820, $1.0615, $1.0610

GBP/AUD: A$1.5230

The major market averages continue to hover near their worst levels of the day with the Dow holding losses of close to 1.2%.

Shares of Microsoft (MSFT 24.58, -0.43) and Nokia (NOK 6.68, -0.34) are in focus today after technology blog Boy Genius reported that Microsoft was set to purchase Nokia's phone business for $19 billion. A Nokia spokesman has denied the reports, calling them "100% baseless." Nonetheless both stocks are seeing heavy volume.

Analysts at CS cut non-farm payrolls data forecast, saying "We are lowering our nonfarm payroll estimate to 120K (from 185K) and our private payroll estimate to 135K (from 200K). The ADP figures were significantly different than our prior forecasts. ADP has been weaker than the official private payrolls 12 of the last 14 months, so the BLS number is likely to print above ADP."

ТD Securities calls the +38k May ADP jobs "a horror show" and says this "was the lowest since last September... exceptionally weak. At face value, it would suggest that private payrolls are likely to be around +100k, and not the +200k expected going into this number."

prices paid 76.5, new orders 51.0 vs 61.7, employment 58.2 vs 62.7, production 54.0 vs 63.8.

EUR/USD

Offers: $1.4420/25, $1.4450, $1.4480/500

Bids: $1.4380, $1.4360/50, $1.4325/20, $1.4300/290

May went out with a bang but June is headed for a sluggish start, with U.S. stock futures barely changed ahead of the opening bell.

Investors are digesting the latest reports on the state of the U.S. job market, and awaiting a couple of reports about manufacturing in the United States. Earlier, manufacturing reports from China and the U.K. signaled a slowdown in the pace of growth.

The rally in U.S. stocks regained momentum Tuesday afternoon, but the day's gains weren't enough to lift the market out of the red for the month.

The market's performance in May was the worst since August 2010. The Dow tumbled nearly 2% for the month, while the S&P 500 and the Nasdaq lost 1.3% as investors wrestled with signs of a slower economic recovery.

Economy: The first of this week's jobs-related economic reports showed that the pace of planned job cuts edged higher in May, according to a report from outplacement consulting firm Challenger, Gray & Christmas.

A separate report, also released Wednesday morning, by ADP showed private-sector payrolls added a modest 38,000 jobs in May. The number falls well below the 170,000 private sector jobs economists were expecting.

Both sets of data are typically used to forecast the government's monthly jobs data, which is due Friday.

At 14:00 GMT the Institute for Supply Management will release its May manufacturing index, and the Commerce Department will issue its April construction spending report.

The ISM Index is expected to slip to 57.6 from April's reading of 60.4, while construction spending is expected to decrease 0.5%.

Companies: Shares of Finnish mobile phone giant Nokia (NOK) fell almost 10% in premarket trade, after Nokia issued a sales warning Tuesday saying it expects device sales to come in "substantially below" its quarterly estimates. Company shares plunged 14% in the previous session.

World markets:

Oil for July delivery slipped 5 cents to $102.65 a barrel.

Gold futures for August delivery fell $3 to $1,532.90 an ounce.

The price on the benchmark 10-year U.S. Treasury was little changed, with the yield 3.06%.

- Stress tests to unveil 'pockets of vulnerability'

07:55 Germany Purchasing Manager Index Manufacturing May 62.0 58.2 57.7

08:00 Eurozone Purchasing Manager Index Manufacturing May 58.0 54.8 54.6

08:30 United Kingdom Purchasing Manager Index Manufacturing May 54.4 54.0 52.1

08:30 United Kingdom Consumer credit, bln April 0.1 0.3 0.1

The euro erased an advance versus the dollar on speculation European Union officials may seek to encourage bondholders to continue lending to Greece.

Investors may be offered preferred status, higher coupon payments or collateral as inducements to buy bonds replacing Greek debt maturing between 2012 and 2014, said two people with knowledge of discussions by policy makers, who declined to be identified because the talks are in progress.

So-called negative incentives are also under consideration, such as cutting off old Greek bonds from eligibility for use as collateral with the European Central Bank, the people said.

EUR/USD: the pair traded within the limits of $1.4383-$1.4440.

USD/JPY: traded within the limits of Y81.10/50.

US data starts at 1100GMT with the weekly MBA Mortgage Application Index, which is followed at 1130GMT by Challenger Layoffs and then at 1145GMT by the weekly ICSC-Goldman Store Sales data. Also today in the US, domestic-made light vehicle sales are expected to slow to a 9.7 million annual rate in May after the slight improvement in April. The seasonal adjustments factors for May tend to be one of the strictest, so raw sales will need to be strong to keep the seasonally adjusted selling rate steady or rising. US data continues with the 1215GMT relesae of the latest ADP National Employment Report.

USD/JPY Y80.85, Y81.50, Y81.70, Y82.00

EUR/JPY Y116.50, Y120.00

GBP/USD $1.6515

AUD/USD $1.0700, $1.0630

AUD/JPY Y85.00, Y88.30

Back below $1.4400 and extends intraday lows to $1.4383 as euro pares gains ahead of the NY open. Support seen into $1.4380 ($1.4381 76.4% $1.4360/1.4448), ahead of $1.4360/50.

The SONIA swap curve is currently implying a 25bps rate hike in February 2012 at the earliest.

USD/JPY Y81.50, Y81.70

EUR/JPY Y116.50, Y120.00

AUD/USD $1.0630

AUD/JPY Y85.00, Y88.30

Hang Seng -0.24% 23626.43

Shanghai Composite 0.0% 2743.57

Nikkei +0.27% 9,720

EUR/USD: the pair bargained within the limits of $1.4390-$ 1.4440.

UK data at 0830GMT includes Bank of England lending data as well as the UK Manufacturing PMI data, which is expected to slip to a reading of 54.1.

There is a raft of US data due at 1400GMT, including the May ISM Index, Construction Spending and the latest Help-wanted Online data. The ISM manufacturing index is expected to fall to a reading of 58.0 in May from 60.4 in April.

Construction spending is expected to rise 0.1% in April after the surprise 1.4% gain in March. Housing starts fell sharply in the month, so residential construction is expected to slow after surging in March on remodeling.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers