- Analytics

- News and Tools

- Quotes

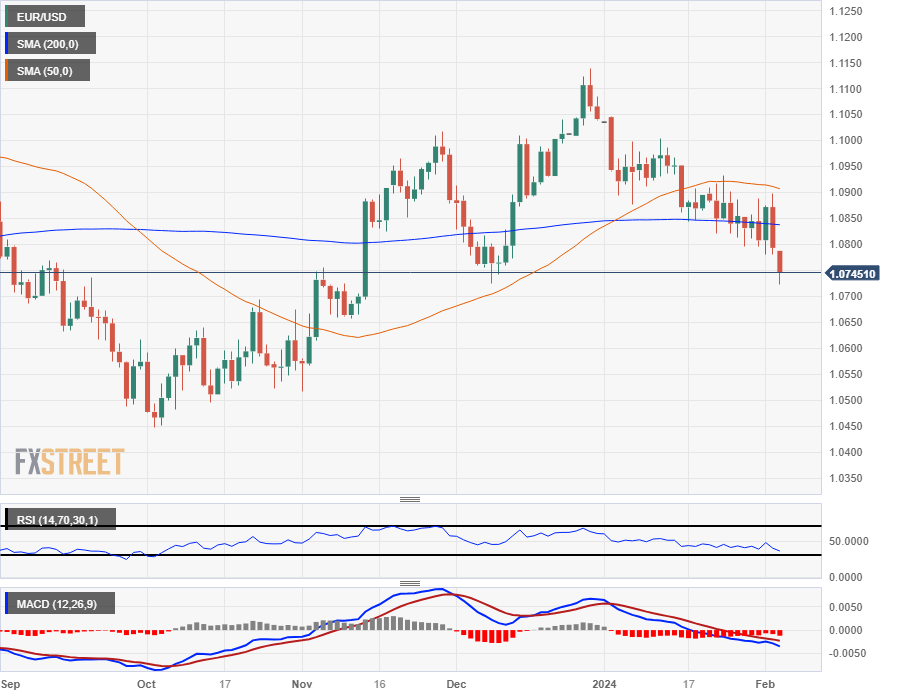

- Chart and quotes for EURUSD

CFD Trading Rate Euro vs US Dollar (EURUSD)

| Date | Rate | Change |

|---|

Related news

-

06.02.2024 13:50EUR/USD remains at risk of a drop through 1.0700 and further losses toward 1.0600 – Scotiabank

EUR/USD traded in a tight range, consolidating recent losses through the low 1.0700s. Economists at Scotiabank analyze the pair’s outlook.

Minor gains attract selling

EUR losses have stalled in the low 1.0700 area; markets appear willing to jump on minor EUR gains to add to short positions at the moment but spot losses have remained contained to the 1.0725 area again.

Retracement support (61.8% of the EUR’s Q4 rally) sits just below the market at 1.0712.

Trend dynamics are bearish on the short-term studies which suggests the EUR remains at risk of a drop through 1.0700 and further losses toward 1.0600.

Minor relief may come if spot can regain 1.0770.

-

06.02.2024 12:17EUR/USD: Three reasons why the Dollar may strengthen against the Euro throughout 2024 – Crédit Agricole

Economists at Crédit Agricole outline three key reasons for its bearish outlook on EUR/USD throughout 2024.

Monetary policy divergence

The ECB may engage in more aggressive rate cutting than the Fed in 2024, potentially positioning the euro as an appealing funding currency for investors.

Impact of QT on European markets

The ECB's accelerated quantitative tightening (QT) measures could expand peripheral yield spreads relative to Bunds, negatively affecting the Euro's appeal.

Heightened global risk aversion

Deteriorating global growth prospects and US political uncertainties could drive investors towards the USD as a safe haven, particularly in the latter half of 2024.

-

06.02.2024 10:32EUR/USD extends losses towards two-month low as ECB rate cut bets persist

- EUR/USD turns lower for the third straight day and seems vulnerable to slide further.

- Expectations that the ECB will start cutting rates in April continue to undermine the Euro.

- Hopes of higher for longer Fed rates favour the USD bulls and validate the negative bias.

The EUR/USD pair attracts fresh sellers following an intraday uptick to the 1.0765 region and drops back closer to a two-month low during the European session on Tuesday. The initial market reaction to an unexpected jump in Germany’s Factory Orders fades rather quickly in the wake of expectations that the European Central Bank (ECB) could start cutting interest rates by April amid falling inflation in the Eurozone. This acts as a headwind for the shared currency, which, along with the underlying bullish tone around the US Dollar (USD), contributes to capping the upside for the currency pair.

The USD Index (DXY), which tracks the Greenback against a basket of currencies, holds firm near its highest level since November 14 as markets seem to have fully priced out early rate cuts by the Federal Reserve (Fed). Recent US macro data suggested that the economy remains in good shape, giving the Fed the headroom to keep rates higher for longer. Apart from this, geopolitical tensions and worries about slowing economic growth in China – the world's second-largest economy – should benefit the safe-haven buck, suggesting that the path of least resistance for the EUR/USD pair is to the downside.

Daily digest market movers: ECB rate cut bets, hawkish Fed expectations weigh

- European Central Bank (ECB) policymaker Pablo Hernandez de Cos said on Tuesday that the next move will be cutting interest rates amid growing confidence that inflation is coming back to the 2% target.

- Germany’s Factory Orders rose by a sharp 8.9% in December on month as against the forecasts for no growth, albeit does little to provide any impetus to the shared currency and lend any support to the EUR/USD pair.

- The ECB's monthly Survey, released earlier today, showed that inflation expectations among Eurozone consumers for the next year fell from 3.5% in November to 3.2% in December.

- Data released by Eurostat showed that Retail Sales in the Eurozone declined by the 0.8% YoY in December as compared to a 0.4% drop in November and consensus estimates for a 0.9% fall.

- The Institute for Supply Management (ISM) reported on Monday that the US services sector growth picked up pace in January, with its Non-Manufacturing PMI rising to 53.4 from 50.5 in December.

- This, along with Friday's blockbuster NFP report and the recent hawkish comments by Federal Reserve officials, forced investors to further scale back expectations for aggressive policy easing in 2024.

- The CME Group's Fedwatch tool indicates that traders have almost entirely priced out the possibility of a March rate cut and now see just five cuts by the end of this year compared with six previously.

- Expectations that the Fed will keep interest rates higher for longer assist the US Dollar to stand tall near its highest level since November 14 and support prospects for a further downside for the EUR/USD pair.

Technical Analysis: EUR/USD bears might wait for break below 1.0700 before placing fresh bets

From a technical perspective, the recent breakdown below the 100-day Simple Moving Average (SMA) and the emergence of fresh selling on Tuesday favour bearish traders. Moreover, oscillators on the daily chart are holding deep in the negative territory and are still away from flashing oversold conditions, suggesting that the path of least resistance for the EUR/USD pair is to the downside. Some follow-through selling below the 1.0700 mark will reaffirm the bearish outlook and drag spot prices further towards the 1.0665-1.0660 intermediate support en route to the 1.0620-1.0615 region and the 1.0600 round figure.

On the flip side, the daily swing high around the 1.0760-1.0765 region seems to act as an immediate hurdle ahead of the 1.0800 mark and the 200-day SMA, currently pegged near the 1.0835-1.0840 zone. That said, a sustained strength beyond the latter might trigger a short-covering rally and allow the EUR/USD pair to reclaim the 1.0900 round figure. Some follow-through buying will negate the negative outlook and shift the near-term bias in favour of bullish traders.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the weakest against the Australian Dollar.

USD EUR GBP CAD AUD JPY NZD CHF USD 0.08% -0.08% -0.09% -0.25% 0.01% -0.05% 0.22% EUR -0.08% -0.16% -0.18% -0.33% -0.08% -0.13% 0.14% GBP 0.08% 0.16% -0.01% -0.17% 0.08% 0.03% 0.30% CAD 0.08% 0.19% 0.02% -0.15% 0.11% 0.05% 0.32% AUD 0.25% 0.34% 0.16% 0.15% 0.26% 0.20% 0.47% JPY -0.01% 0.10% -0.07% -0.09% -0.26% -0.06% 0.22% NZD 0.05% 0.12% -0.03% -0.05% -0.21% 0.05% 0.26% CHF -0.23% -0.14% -0.31% -0.32% -0.48% -0.22% -0.27% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance. -

06.02.2024 10:21EUR/USD: Failure to defend 1.0725/1.0700 could mean deeper decline towards 1.0610 – SocGen

EUR/USD has moved back to the December low at 1.0725. Economists at Société Général analyze the pair’s outlook.

Recent pivot high at 1.0900 must be overcome to confirm an extended bounce

EUR/USD has experienced a steady pullback after failing to reclaim interim resistance zone near the graphical levels of 1.1100/1.1150 representing highs of April / May 2023. It has given up both 50-DMA and 200-DMA but slope of both the Moving Averages is flattish denoting lack of clear direction.

December low of 1.0725/1.0700 is next potential support. Failure to defend could mean deeper decline towards 1.0610 and the lower limit of the range since January 2023 at 1.0484/1.0448.

Recent pivot high at 1.0900 must be overcome to confirm an extended bounce.

-

06.02.2024 07:57EUR/USD to trade out something like a 1.0700-1.0900 range this month – ING

EUR/USD broke lower again on Monday. Economists at ING analyze the pair’s outlook.

Support at the 1.0715/1.0725 area

EUR/USD now has support at the 1.0715/1.0725 area.

EUR implied volatilities are staying quite low and suggest the market is not preparing for a major break out. We agree and think this will be more of a case of EUR/USD trading out something like a 1.0700-1.0900 range this month rather than pushing down to 1.0500.

See: EUR/USD will be more comfortable in a 1.0400 to 1.1200 range than at levels closer to 1.2000 – Rabobank

-

06.02.2024 03:08EUR/USD inches higher to near 1.0750, Eurozone Retail Sales eyed

- EUR/USD faced trouble after weaker EU PPI data on Monday.

- The improved US ISM Services data supported the US Dollar.

- Fed’s Powell emphasized monitoring inflation's sustained trajectory toward the 2% core target.

EUR/USD hovers near 1.0750 during the Asian session on Tuesday after witnessing a plunge in the previous session. The EUR/USD pair tumbled on hawkish remarks from the US Federal Reserve’s (Fed) Chair Jerome Powell, coupled with the improved US ISM Services data.

The US ISM Services PMI recorded a 53.4 reading in January, exceeding the expected figure of 52.0 and the previous month's 50.5. Additionally, the ISM Services Employment Index rose to 50.5 from the previous reading of 43.8.

Federal Reserve Chairman Jerome Powell emphasized the significance of closely monitoring inflation's sustained trajectory toward the 2% core target. This stance resulted in an uptick in US Treasury yields, exerting downward pressure on the EUR/USD pair. The market response reflected increased confidence in the strength of the US Dollar amid indications of a less accommodative monetary policy stance from the Federal Reserve.

Additionally, the Euro (EUR) faced additional downward pressure following the release of weaker Europe’s Producer Price Index (PPI) data on Monday. The European Union (EU) is contending with a disinflationary trend, potentially prompting the European Central Bank (ECB) to consider easing its policy. The Organisation for Economic Co-operation and Development (OECD) foresees inflation across Europe remaining above the ECB's 2% target until sometime after 2025.

In December, the annual PPI recorded a decline of 10.6%, surpassing the anticipated decrease of 10.5% and the previous figure of 8.8%. While the monthly index showed a fall of 0.8% as expected. The previous decline was 0.3%.

Investors are attentively monitoring speeches from Federal Reserve officials for further insights into potential monetary policy adjustments. Conversely, Tuesday's release of December's Eurozone Retail Sales data is anticipated to provide additional information on the economic conditions within the Eurozone.

-

05.02.2024 19:34EUR/USD finds further room on the low side, extends recent declines

- EUR/USD slides as German Imports tumble, pan-EU PPI slips further.

- EUR/USD tested into 12-week lows in Monday’s decline.

- German Trade Balance rises on accelerating Import declines.

The EUR/USD fell another half-percent on Monday, dragging the pair into 12-week lows near 1.0723 after EU economic data failed to inspire investor confidence. The OECD sees pan-European inflation holding above the European Central Bank’s (ECB) 2% until sometime after 2025, hampering money market’s expectations for rate cuts from the ECB, further suppressing upside potential in the Euro (EUR).

This week still brings European Retail Sales for December as well as the ECB’s latest Economic Bulletin, with Friday rounding out the economic calendar with Germany’s Harmonized Index of Consumer Prices (HICP) for January.

Daily digest market movers: EUR/USD extends declines as investors look for reasons to buy

- Germany’s Trade Balance rose to €22.2 billion after German Imports tumbled to multi-year lows, declining 6.7% in December versus the forecast -1.5%, engulfing the previous month’s 1.5%.

- Germany’s HCOB Composite Purchasing Manager’s Index (PMI) also slid in January, printing at 47.0 versus the forecast steady hold at 47.1.

- Pan-European Producer Price Index (PPI) figures also declined for the year ended in December, coming in at -10.6% versus the forecast -10.5%, falling even further away from the previous period’s -8.8%.

- Tuesday brings December’s euro area Retail Sales, forecast to tick upwards slightly to -0.9% for the year ended in December versus the previous period’s -1.1%.

- MoM Retail Sales are expected to see accelerated declines of -1.0% compared to the previous month’s -0.3%.

- The ECB drops their latest Economic Bulletin on Thursday, investors will be looking for tonal shifts regarding interest rate cuts from the ECB but hopes are waning.

- Friday rounds out the European economic calendar with Germany’s HICP inflation for January, forecast to hold steady at 3.1%.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the weakest against the US Dollar.

USD EUR GBP CAD AUD JPY NZD CHF USD 0.32% 0.67% 0.45% 0.29% 0.08% 0.10% 0.34% EUR -0.32% 0.35% 0.13% -0.03% -0.24% -0.21% 0.01% GBP -0.67% -0.35% -0.22% -0.39% -0.60% -0.57% -0.34% CAD -0.45% -0.13% 0.22% -0.17% -0.38% -0.35% -0.12% AUD -0.29% 0.03% 0.39% 0.17% -0.21% -0.18% 0.04% JPY -0.09% 0.23% 0.57% 0.38% 0.21% 0.01% 0.25% NZD -0.10% 0.22% 0.57% 0.35% 0.19% -0.05% 0.23% CHF -0.34% -0.01% 0.33% 0.12% -0.05% -0.27% -0.24% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: EUR/USD looking to springboard off chart territory near 1.0720

EUR/USD shed further weight after opening the trading week near 1.0780, dipping into multi-week lows near 1.0720 as the pair accelerates into the bearish side of the 200-hour Simple Moving Average (SMA) descending through 1.0840.

Despite EUR/USD recovering late Monday, the pair remains steeply off of recent consolidation around the 200-day SMA near 1.0850, and the pair is running into old technical support from December’s swing low. EUR/USD is set for a bearish challenge of the 1.0700 handle, while the topside sees technical congestion waiting for buyers as the 200-day and 50-day SMA consolidate near 1.0850 and 1.0900, respectively.

EUR/USD hourly chart

EUR/USD daily chart

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance. -

05.02.2024 15:12EUR/USD dips amid Powell’s remarks, high US yields

- EUR/USD drops 0.40% to 1.0742, influenced by Powell's hawkish remarks and rising US Treasury yields.

- Powell emphasizes Fed's inflation target commitment, suggesting mid-year policy tweaks.

- US January labor market strength bolsters USD, contrasting with Eurozone's economic fragility.

- Euro falters as US Dollar Index climbs, with ECB policy easing expectations and focus on central bank moves.

The Euro (EUR) extended its losses against the Greenback (USD) in early trading during the New York session, down 0.40%, sponsored by high US Treasury yields and the strong US Dollar. Federal Reserve Chair Jerome Powell's Sunday interview delivered a hawkish message to the detriment of other G10 FX currencies. At the time of writing, the EUR/USD trades at 1.0742 after hitting a high of 1.0785.

EUR/USD faces downward pressure as Powell’s reiterate focus on inflation

Over the weekend, Powell commented that it was too early to ease policy while emphasizing the job is not done – driving inflation toward its 2% target. The Fed Chair added the first cut could happen in the middle of the year.

Meanwhile, data revealed last week struck a pleasant surprise for the US economy, as the Nonfarm Payrolls report for January showed the jobs market added 353K Americans to the workforce while the unemployment rate stood at 3.7%. That indicates the labor market remains strong, maintaining the soft-landing narrative in play.

US Treasury yields climbed sharply following the Fed’s Chair Powell interview, while the US Dollar Index (DXY), a gauge to track the performance of the buck against other currencies, rose 0.41%, at 104.39.

The Euro weakened as Flash PMIs in the Eurozone (EU) stood at recessionary territory despite signaling the economy slightly recovered. In addition to that, the Producer Price Index (PPI) for the block edged lower. Given the backdrop of the disinflation process in the EU, that could pave the way for the European Central Bank (ECB) to begin to ease policy.

EUR/USD Price Analysis: Technical outlook

The EUR/USD has fallen below the 100-day moving average (DMA) at 1.0783, diving to a new year-to-date (YTD) low of 1.0725, about to pierce the December 8 low of 1.0723. A breach of the latter will clear the path to 1.0700. On the flip side, buyers could recover some territory past the 1.0750, followed by the 100-DMA and the 1.0800 figure.

-

05.02.2024 14:07EUR/USD will be more comfortable in a 1.0400 to 1.1200 range than at levels closer to 1.2000 – Rabobank

EUR/USD has slowly trended lower since its late December high in the region of 1.1139. Economists at Rabobank analyze the pair’s outlook.

USD strength to moderate in the second half of the year

We maintain our one-month EUR/USD forecast of 1.0700 and our three-month target of 1.0500.

We expect USD strength to moderate in the second half of the year as the Fed’s rate cutting cycle kicks off.

Assuming that CPI inflation in the Eurozone can be kept under control, it is likely that Germany would benefit from a relatively weak EUR whilst it tackles structural reforms. For this reason, we see risk of EUR/USD being more comfortable in a 1.0400 to 1.1200 range over the next couple of years than at levels closer to 1.2000.

-

05.02.2024 13:39EUR/USD: Losses through recent support around 1.0785/1.0795 to extend – Scotiabank

EUR/USD’s break under support in the upper 1.0700s means more losses are likely, economists at Scotiabank say.

Resistance is 1.0795/1.0800

Spot losses through recent support around 1.0785/1.0795 (100-Day Moving Average and 50% retracement support from the EUR’s Q4 rally) suggest more, corrective EUR losses towards 1.0712 (61.8% Fibonacci).

Trend momentum signals are aligned bearishly for the EUR on the intraday and daily DMIs which will limit the scope for EUR gains.

Resistance is 1.0795/1.0800.

See – EUR/USD: The direction of travel lies to the 1.0700 area – ING

-

05.02.2024 11:23EUR/USD to drift higher in the second half of the year – MUFG

In January, EUR/USD weakened back after end-2023 rebound. Economists at MUFG Bank analyze the pair’s outlook.

EUR/USD correction lower followed by rebound to new highs

Over the year as a whole, the forward market indicates a remarkably synchronised easing by the Fed and the ECB, which if correct would point to limited scope for yield driven big moves in EUR/USD.

We remain neutral on EUR/USD in H1 but see a slowing US economy emerging, contrasting somewhat with a modest pick-up in Eurozone growth which will allow for EUR/USD to drift higher in H2, although the move will be curtailed by US political risks.

-

05.02.2024 09:53EUR/USD languishes near YTD low as traders continue to trim Fed rate cut bets

- EUR/USD drops to a fresh YTD low and is pressured by a combination of factors.

- The USD builds on the post-NFP rise and touches its highest level since December.

- Bets for an April rate cut by the ECB continue to undermine the shared currency.

The EUR/USD pair trades with a negative bias for the second successive day on Monday and languishes near the YTD trough, around the 1.0770 region during the early European session. Investors further scaled back their expectations for a more aggressive policy easing by the Federal Reserve (Fed) in the wake of Friday's blockbuster US jobs data, which continues to push the US Treasury Bond yields higher. This, along with the risk of a further escalation of geopolitical tensions in the Middle East and China's economic woes, underpins the Greenback's relative safe-haven status and exerts pressure on the currency pair.

In contrast, falling inflation in Germany and France – the Eurozone's two largest economies – has raised hopes that the European Central Bank (ECB) could start cutting its benchmark deposit rate from the current record-high level of 4% by April. This is seen as another factor that contributes to the offered tone surrounding the EUR/USD pair and supports prospects for an extension of the post-NFP rejection slide from the vicinity of the 1.0900 mark. Traders now look to the US ISM Services PMI and Fedspeak for fresh impetus later today.

Daily Digest Market Movers: EUR/USD seems vulnerable near YTD low amid bullish US Dollar

- The upbeat US jobs report points to a still-resilient US labor market and gives the Federal Reserve headroom to keep rates higher for longer, underpinning the US Dollar and exerting pressure on the EUR/USD pair.

- Furthermore, Fed Chair Jerome Powell, speaking in an interview with the US TV show 60 Minutes over the weekend, reiterated that the March meeting is likely too soon to have the confidence to start cutting interest rates.

- The probability of the first interest rate cut by the Fed in May stands at about 70%, down from 90% before the key employment data, and the probability of 150-bps of cumulative rate cuts in 2024 plummets to just around 20%.

- The yield on the benchmark 10-year US government bond extends the post-NFP rise beyond the 4.0% threshold on Monday and favours the USD bulls amid a slight deterioration in the global risk sentiment.

- Israel's Prime Minister Benjamin Netanyahu said that the country will not end the war before it completes all of its goals, while media reports suggest that Hamas is set to reject the Gaza ceasefire deal proposed in Paris.

- The US Central Command said its forces conducted a strike in self-defence against a Houthi land-attack cruise missile and struck four anti-ship cruise missiles prepared to launch against ships in the Red Sea.

- A private survey showed that business activity in China's services sector remained in expansionary territory for 13 straight months, though grew less than expected in January and added to slowdown concerns.

- Eurozone CPI moves slowed from the 2.9% YoY rate to 2.8% in January, moving closer to the 2% target and making it more likely that the European Central Bank will start cutting interest rates by April.

- ECB's Governing Council member Boris Vujcic said that the central bank needs to ensure there aren’t any second-round effects on inflation from wages before cutting rates, though fails to inspire the Euro bulls.

- The US ISM Services PMI is due for release later today and is expected to improve from 50.6 to 52.0 in January, which, along with Fedspeaks, will influence the buck and provide some impetus to the currency pair.

Technical Analysis: EUR/USD struggles near 100-day SMA, seems poised to depreciate further

From a technical perspective, acceptance below the 100-day Simple Moving Average (SMA) will be seen as a fresh trigger for bearish traders. Given that oscillators on the daily chart are holding deep in the negative territory and are still away from being in the oversold zone, the EUR/USD pair might then slide to the December 2023 swing low, around the 1.0725-1.0720 region. This is closely followed by the 1.0700 mark, below which the downward trajectory could accelerate further towards the 1.0665-1.0660 intermediate support en route to the 1.0620-1.0615 region and the 1.0600 round figure.

On the flip side, any attempted recovery back above the 1.0800 mark is likely to attract fresh sellers and remain capped near the 200-day SMA, currently pegged near the 1.0835-1.0840 zone. A sustained strength beyond, however, might trigger a short-covering rally and allow the EUR/USD pair to reclaim the 1.0900 round figure. The latter should act as a key pivotal point, which if cleared decisively will negate the negative outlook and shift the near-term bias in favour of bullish traders.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the weakest against the New Zealand Dollar.

USD EUR GBP CAD AUD JPY NZD CHF USD 0.14% 0.07% 0.10% 0.02% -0.05% -0.08% 0.21% EUR -0.16% -0.09% -0.05% -0.14% -0.21% -0.24% 0.05% GBP -0.07% 0.08% 0.03% -0.05% -0.12% -0.15% 0.14% CAD -0.10% 0.03% -0.03% -0.08% -0.16% -0.18% 0.10% AUD -0.03% 0.14% 0.06% 0.09% -0.07% -0.09% 0.19% JPY 0.04% 0.20% 0.11% 0.17% 0.07% -0.04% 0.26% NZD 0.10% 0.23% 0.18% 0.18% 0.09% 0.00% 0.27% CHF -0.21% -0.05% -0.14% -0.11% -0.18% -0.26% -0.29% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance. -

05.02.2024 07:57EUR/USD: The direction of travel lies to the 1.0700 area – ING

The strong US jobs data swung EUR/USD back under 1.0800 on Friday. Economists at ING analyze the pair’s outlook.

The market still prices a 55% chance of an ECB rate cut in April

It is tempting to say the direction of travel lies to the 1.0700 area, and if so, it will probably be a function of the US side of the equation. From the Eurozone side, the calendar is relatively light.

Given the market still prices a 55% chance of an ECB rate cut in April, there is always a risk of a EUR-positive back-up in short-term rates if that cut is removed. It is not clear this will be the week in which the April rate cut is removed.

-

05.02.2024 06:14EUR/USD Price Analysis: Holds below 1.0800 ahead of German, Eurozone Services PMI data

- EUR/USD attracts some sellers around 1.0780 on the firmer USD.

- The pair keeps the bearish outlook unchanged below the key EMA; RSI indicator remains below the 50 midlines.

- The immediate resistance level will emerge at 1.0840; the initial support level for EUR/USD is located at 1.0752.

The EUR/USD pair remains on the defensive during the early European session on Monday. The hawkish remarks from Federal Reserve (Fed) Chairman Jerome Powell provide some support to the US Dollar (USD) and exert some selling pressure on the EUR/USD pair. Investors await the Services PMI data from Germany and the Eurozone for fresh catalysts. At press time, the major pair is trading at 1.0780, losing 0.11% on the day.

Fed Chairman Jerome Powell said on Sunday that a rate cut in March is too early, and he doesn’t believe the central bank will have the confidence by then that inflation will return to a 2% target sustainably. The US Central Bank emphasized that it wants more confidence before taking the very important step of beginning rate cuts.

Technically, the bearish outlook of EUR/USD remains intact as the major pair is below the key 100-period Exponential Moving Averages (EMA) with a downward slope on the four-hour chart. The tower momentum is supported by the Relative Strength Index (RSI), which stands below the 50 midlines, suggesting that the path of least resistance level is to the downside.

On the bright side, the immediate resistance level for the major pair will emerge near the 50-period EMA at 1.0840. The next upside barrier is seen near the 100-period EMA at 1.0865. A decisive break above the latter will pave the way to the key hurdle at 1.0900, representing the confluence of the upper boundary of the Bollinger Band and a psychological mark. The additional upside filter to watch is a high of January 15 at 1.0967, and finally at the 1.1000 psychological round figure.

On the flip side, the first support level for EUR/USD is located near the lower limit of the Bollinger Band at 1.0752. A breach of this level will expose a low of December 8 at 1.0723, en route to a low of November 9 at 1.0660.

-

05.02.2024 02:00EUR/USD weakens to 1.0780 ahead of German Trade Balance, Eurozone PMI data

- EUR/USD trades on a weaker note near 1.0772 amid the stronger USD.

- Fed’s Powell said a rate cut in March is too soon, as he doesn’t believe that inflation is heading back to 2% sustainably.

- US January Nonfarm Payrolls were at 353K, beating market expectatins of 180K; the Unemployment was flat; wages spiked.

The EUR/USD pair faces some selling pressure above the mid-1.0700s during the early Asian trading hours on Monday. The US Dollar Index (DXY) edges higher as the Federal Reserve (Fed) Chair Jerome Powell pushed back on the timing of rate cuts. The major pair currently trades around 1.0772, down 0.19% on the day.

Late Sunday, Fed Chairman Jerome Powell said a rate cut in March is too soon as he doesn’t believe the FOMC will have the confidence by then that inflation is heading back to 2% sustainably. Powell added that policymakers see it appropriate to cut rates this year, but it is prudent to be open to the possibility of rates falling from spring onwards. The US central bank will discuss at the March meeting about the timing of easing the pace of quantitative tightening (QT).

According to the US Bureau of Labor Statistics on Friday, the Nonfarm Payrolls (NFP) rose by 353K in January, above expectations for a 185K increase in the previous reading. Meanwhile, the Unemployment Rate was unchanged at 3.7%. Finally, wage growth is firming, with Average Hourly Earnings climbing 4.5% YoY in January from the previous reading of 4.4% in December.

On the other hand, European Central Bank (ECB) Governing Council member Boris Vujcic said on Sunday that the central bank needs to ensure there aren’t any second-round effects on inflation from wages before cutting interest rates.

Investors will keep an eye on the German Trade Balance and the January HCOB Composite PMI from Germany, the Eurozone and Spain. On the US docket, the ISM Services PMI will be due. -

02.02.2024 17:49EUR/USD sheds 1.0900 once again as US NFP sends Greenback higher

- EUR/USD loses key technical handle after US Jobs Report thumps forecasts.

- US NFP hits highest level in a year, March rate cut hopes all but buried.

- US Average Hourly Earnings also gained ground in January.

EUR/USD continues to churn on Friday, keeping a near-term choppy technical pattern intact as the Euro (EUR) cycles against the US Dollar (USD).

US Nonfarm Payrolls wildly outperformed market expectations, hitting a one-year high and bringing sharp upside revisions to previous datapoints. Investors hoping for faster, sooner rate cuts from the US Federal Reserve (Fed) have seen rate cut hopes dwindle as the US domestic economy continues to surprise with its sturdiness.

Daily digest market movers: EUR/USD back into familiar lows as cyclical pattern drags the pair down.

- EUR/USD climbed into 1.0900 early Friday before getting dragged back down post-NFP.

- US Nonfarm Payrolls climbed to 353K in January, vaulting well over the forecast 180K.

- December’s NFP figure also saw a sharp upside revision to 333K from 216K.

- YoY US Average Hourly Earnings also gained in January, coming in at 4.5% versus the forecast 4.1% and the previous period’s 4.4% (revised upwards from 4.1%).

- MoM US Average Hourly Earnings climbed 0.6% in January versus the forecast 0.3%, 0.4% last.

- US Unemployment Rate held steady at 3.7% in January; markets expected a tick upwards to 3.8%.

- Michigan Consumer Sentiment Index gained to 79.0, above the forecast 78.9 and climbing further above the previous month’s 78.8.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the strongest against the Japanese Yen.

USD EUR GBP CAD AUD JPY NZD CHF USD 0.82% 0.97% 0.62% 1.02% 1.35% 1.30% 1.16% EUR -0.82% 0.17% -0.21% 0.19% 0.52% 0.50% 0.32% GBP -0.96% -0.15% -0.32% 0.06% 0.38% 0.33% 0.20% CAD -0.64% 0.18% 0.34% 0.39% 0.72% 0.67% 0.51% AUD -1.01% -0.19% -0.02% -0.36% 0.32% 0.31% 0.12% JPY -1.37% -0.51% -0.34% -0.74% -0.33% 0.01% -0.20% NZD -1.32% -0.50% -0.33% -0.71% -0.31% 0.00% -0.15% CHF -1.16% -0.32% -0.15% -0.52% -0.12% 0.20% 0.18% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: EUR/USD steeply off recent highs as whipsaw pattern remains

EUR/USD came within touching distance of 1.0900 early Friday, but the pair got dragged back into familiar lows below 1.0800 near 1. 0780.

Friday’s bearish action sees the EUR/USD tumble out of a familiar consolidation zone between the 200-day and 50-day Simple Moving Averages (SMA), between 1.0900 and 1.0850.

The EUR/USD continues to drift into the low side in choppy trading, and the pair is down over 3% from December’s swing high into 1.1140.

EUR/USD hourly chart

EUR/USD daily chart

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance. -

02.02.2024 14:33EUR/USD dips toward 1.0800 on hot US Nonfarm Payrolls, strong US Dollar

- EUR/USD falls to 1.0791, reacting to US adding 353,000 jobs in January, surpassing expectations.

- Steady US unemployment at 3.7% and faster wage growth signal tight labor market, raising inflation concerns.

- Jump in US Treasury yields and US Dollar Index rally post-job report underscore strong US economic outlook.

The Euro extends its losses versus the US Dollar following a hot US employment report, that witnessed the economy created more than 300,000 jobs in January. Therefore, the EUR/USD trades at around 1.0800, hitting a daily low of 1.0791.

US Nonfarm Payrolls in January crushed forecasts despite the upward revision of December

The US Bureau of Labor Statistics revealed that Nonfarm Payroll employment rose by 353,000 in January, crushing the previous month's reading of 216,000, which was revised upward to 333,000. Digging into the data, the Unemployment Rate was unchanged at 3.7% but below estimates, while Average Hourly Earnings ticked up to 0.6% MoM from 0.4% the previous month. On a yearly basis, earnings by the hour rose 4.5% from 4.4%, with monthly and yearly figures exceeding forecasts.

US equities tumbled on the report, while the US 10-year Treasury note yield rose by more than ten basis points, up above the 4% threshold. Consequently, the Greenback (USD) stages a comeback after the US Dollar Index (DXY) braced to 103.00, its weekly low, before surging to a daily high of 103.86.

Ahead in the calendar, the US docket will feature the release of the University of Michigan Consumer Sentiment alongside Factory Orders.

Recently, Joachim Nagel, the Bundesbank President and member of the governing Council of the European Central Bank (ECB), stated in an interview that it was too early to cut rates after the US Nonfarm Payrolls data was released.

EUR/USD Price Analysis: Technical outlook

From a technical perspective, the EUR/USD breaching of the 200-day moving average (DMA) could open the door for further downside. once sellers crack the 1.0800 figure, further weakness is seen at the 100-DMA at 1.0782, followed by the December 8 daily low, an intermediate support at 1.0724, before slumping to 1.0700. On the flip side, the 200-DMA would be the first barrier for buyers at 1.0832,before aiming toward 1.0900.

-

02.02.2024 12:30EUR/USD: Potentially bullish price action on the weekly chart will support the idea of a rebound – Scotiabank

EUR/USD is little changed on the day after modest, earlier gains stalled just below 1.0900. Economists at Scotiabank analyze the pair’s outlook.

EUR rally capped below 1.0900 for now

A solid rebound from Thursday’s intraday low (coinciding with a test of the 100-DMA and the 50% Fib retracement of the EUR’s Q4 rally) may well equate to the market setting the low for the EUR’s January decline.

Potentially bullish price action on the weekly chart (‘hammer’ pattern) will support the idea of a EUR rebound if confirmed today.

Support is 1.0865/1.0875. Resistance is 1.0950/1.0975.

-

02.02.2024 10:24EUR/USD: Unlikely to see an immediate return to the area above 1.0900 – Commerzbank

EUR/USD is not so far away from 1.0900, the level it was trading around before the last dovish ECB meeting. Ulrich Leuchtmann, Head of FX and Commodity Research at Commerzbank, analyzes the pair’s outlook.

An inflation risk premium on the Euro is appropriate

The point is that the ECB may not have the room to cut rates too quickly and that an initial cut in March or April may not actually happen. However, one negative factor for the EUR remains, and that is the impression that a large faction within the ECB Governing Council is really dragging its feet and will later take the first opportunity to push for rate cuts. Perhaps too soon, depending on the situation.

I therefore continue to believe that an inflation risk premium on the Euro is appropriate. I would therefore be critical of an immediate return of EUR/USD to the area above 1.0900.

-

02.02.2024 09:24EUR/USD extends gains towards 1.0900 as traders brace for NFP

- EUR/USD extends gains as US Dollar weakens after mixed US data.

- The Euro could face challenges as markets speculate over an ECB interest rate cut in June.

- The expected decline in US Nonfarm Payrolls could further weaken the US Dollar.

The EUR/USD pair extends its gains for the second consecutive day, edging higher to near 1.0880 during the European session on Friday. EUR/USD gained upward support following mixed economic data from the United States (US). Further, the subdued US Treasury yields contribute to adding pressure on the US Dollar (USD). US Treasury yields experienced downward pressure following reports from regional bank New York Community Bancorp, which indicated increased stress in its commercial real estate portfolio.

The Euro faced a decline following the release of softer German consumer inflation data on Wednesday, as market sentiment leaned towards the possibility of a speculative interest rate cut by the European Central Bank (ECB) in June. However, the European currency initiated a recovery after the release of mixed Eurozone inflation data on Thursday.

The US Dollar Index (DXY), which measures the performance of the US Dollar (USD) against a basket of six major currencies, struggles to retrace its recent losses. The DXY trades around 103.00, with the 2-year and 10-year US Treasury yields hovering around 4.23% and 3.88%, respectively, at the time of writing.

US Initial Jobless Claims rose to 224K for the week ending on January 26, exceeding both the previous increase of 215K and the expected figure of 212K. However, ISM Manufacturing PMI improved to 49.1 from the prior reading of 47.1, surpassing the anticipated figure of 47.0 in January. On Friday, key labor data is set to be released, including US Average Hourly Earnings and Nonfarm Payrolls (NFP).

Daily digest market movers: EUR/USD extends gains after mixed US economic data

- Eurozone preliminary Core Harmonized Index of Consumer Prices (YoY) increased by 3.3% in January, higher than the expected 3.2% growth but lower than the 3.4% prior.

- The annual Consumer Price Index came in at 2.8%, as expected, against the previous reading of 2.9%. The month-over-month report showed a decline of 0.4%, swinging from the 0.2% rise in December.

- German Consumer Price Index (CPI) for January showed a year-on-year increase of 2.9%, lower than the expected 3.3% and down from December's reading of 3.7%.

- Germany’s consumer inflation met expectations, rising to 0.2% MoM from the previous reading of 0.1%. The Harmonized Index of Consumer Prices YoY increased 3.1%, lower than the previous figure of 3.8%.

- The preliminary US Nonfarm Productivity increased by 3.2% in Q4, higher than the expected 2.5%, but down from the previous reading of 4.9%.

- US Challenger Job Cuts rose to 82,307 in January from the previous 34,817 in December.

- US Unit Labor Costs reported a 0.5% rise against the 1.7% expected in the fourth quarter, swinging from the previous 1.1% decline.

Technical Analysis: EUR/USD moves higher towards psychological barrier at 1.0900

EUR/USD advances to near 1.0880 on Friday, close to the immediate resistance around the psychological level at 1.0900. A breakthrough above the latter could exert upward pressure on the pair to surpass the 38.2% Fibonacci retracement level at 1.0915 to navigate the next barrier around the major level at 1.0950.

On the downside, the major level at 1.0850 appears as the key support, which is aligned with the 21-day Exponential Moving Average (EMA) at 1.0846. A break below this region could push the EUR/USD pair to approach the psychological support at 1.0800, followed by the weekly low at 1.0779.

EUR/USD: Four-Hour Chart

-638424624928399111.png)

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the strongest against the Japanese Yen.

USD EUR GBP CAD AUD JPY NZD CHF USD -0.14% -0.06% -0.06% -0.30% 0.23% -0.02% -0.14% EUR 0.16% 0.10% 0.10% -0.14% 0.39% 0.14% 0.02% GBP 0.10% -0.06% 0.05% -0.22% 0.32% 0.04% -0.07% CAD 0.06% -0.07% 0.00% -0.24% 0.28% 0.04% -0.09% AUD 0.31% 0.17% 0.24% 0.26% 0.53% 0.28% 0.16% JPY -0.23% -0.40% -0.32% -0.26% -0.50% -0.27% -0.38% NZD 0.06% -0.07% 0.00% 0.01% -0.24% 0.29% -0.08% CHF 0.16% 0.04% 0.08% 0.12% -0.16% 0.40% 0.12% The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers